One thing we always demand in a stock is a megatrend-powered dividend that grows. And there aren’t many megatrends bigger than the soaring need for (and tight supply of) food.

I’ll share three tickers from three different parts of the food business—a fertilizer maker, a crop trader and a seller of packaged foods here in the US—in a second.

These “megatrend” plays have grown their payouts fast, driving quick pops in their share prices. (Pick No. 3 could easily 3X its payout tomorrow without breaking a sweat!) The best part is that these payouts have staying power through inflation, recession, geopolitical mayhem, you name it.

Dodging the “Dollar Bulldozer” Is Key to “Mega-Dividends” in Food Stocks

The numbers around our future food supply are sobering: according to the UN Food and Agricultural Organization, global food demand will soar 70% by 2050.

Meantime, we’re facing a trifecta of factors cutting food supplies. They include droughts, wars (including Russia’s despicable invasion of Ukraine) and the strong US dollar—or as I call it, the “dollar bulldozer,” which cuts the value of sales US companies make abroad.

These conditions are worrying, to be sure, but they also create opportunities for companies that process crops, help farmers boost their yields, and sell food through stores here in the US, where the economy is holding up and the “dollar bulldozer” isn’t a worry.

Megatrend Food Stock No. 1: A Global Crop Processor With an Accelerating Payout

Archer Daniels Midland (ADM) operates 400 crop-procurement facilities and 270 processing plants across the globe, turning crops into supplements and ingredients for food makers. ADM also produces animal feed and runs a commodity-trading business.

ADM is flashing not one but three signals we Hidden Yielders look for in a dividend play:

- A dividend whose growth is accelerating

- Smartly timed share buybacks

- Relative strength against the rest of the market.

Let’s take those first two points at once, because they’re tied together.

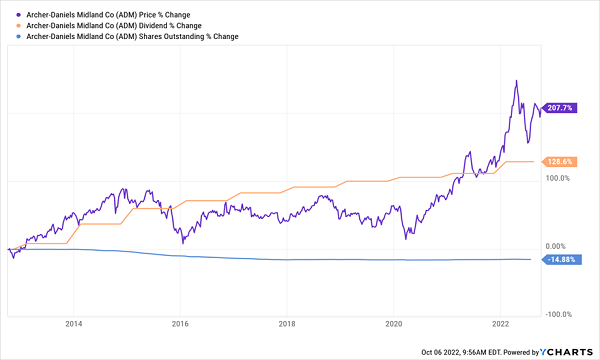

If you’ve been reading my columns on Contrarian Outlook for a while, you know about the “Dividend Magnet.” It’s the tendency for a company’s share price to track its dividend growth. You can see this in action with ADM’s payout (in orange below), which has more than doubled in the last decade, pacing its share price (in purple) higher.

ADM’s Dividend Drives Its Stock (With a Buyback Assist)

That rapid dividend growth, which I see accelerating as future food demand rises, is more than enough to offset ADM’s ho-hum 1.9% current yield.

The company’s buybacks (in blue), meanwhile, reduce the company’s share count, which increases its earnings per share, which, in turn, helps lift the share price.

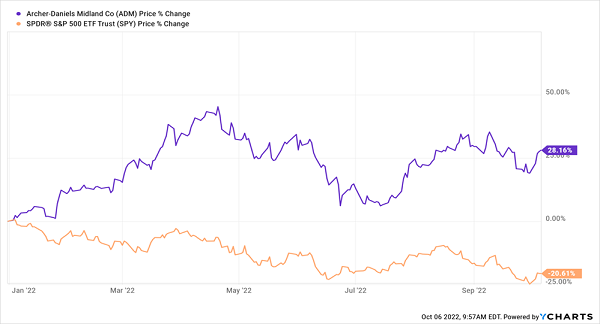

Which brings us to our third indicator that ADM is ripe for buying: it’s showing “relative strength” against the rest of the market. That simply means the stock has momentum, and stocks that are on the rise tend to keep rising. ADM has done that in spades this year, soaring while the S&P 500 tanked.

ADM’s Relative Strength, Low Volatility on Display in ’22

Put it all together and you’ve got a stock primed to deliver rising income, strong price gains and “megatrend” growth through the rest of the decade.

Megatrend Food Stock No. 2: A Smart Buy for Inflation, a Recession or Both

Conagra (CAG), yields 4% today and owns household-name food brands like Slim Jim, Duncan Hines, PAM and Hunt’s, is a good way to profit whether inflation keeps roaring or a recession hits, because both outcomes keep people out of restaurants and eating at home.

The Chicago-based company has this advantage because its products are affordable staples, not the fancy fare consumers often cut first when tough times hit. That gives CAG pricing power it can use to offset rising ingredient and shipping costs.

You can see that in CAG’s revenue, which jumped 9% in the third quarter, even as inflation took off. That bodes well for another big hike in the dividend, which has already soared 55% since late 2019:

CAG’s Dividend Springs to Life.

Add in CAG’s safe payout ratio—dividends account for just 24% of earnings and 52% of free cash flow—and you’ve got a recipe for more big hikes in the future.

That, in turn, should fuel CAG’s “Dividend Magnet.” As you can see in the chart above, the payout paced the stock higher until late last year, when a gap opened up. That gap is our upside—and it makes now a great time to buy.

“Megatrend” Food Stock No. 3: A Fertilizer Play That Could 3X Its Payout Tomorrow

Canada’s Nutrien (NTR) is the world’s largest producer of potash and the third-largest producer of nitrogen fertilizer. It balances its exposure to sometimes-volatile fertilizer markets with its network of 2,000 retail stores, which sell directly to farmers.

(Don’t let its foreign domicile worry you—Nutrien reports results in US dollars, not Canadian “loonies,” which have also been plowed under by the dollar bulldozer.)

Farmers are racing to increase production as prices for corn, soybeans and wheat stay high—a situation that won’t likely ease anytime soon. Wheat supplies, for example, remain tight due to limited exports from Ukraine (the world’s No. 8 producer) and Russia (No. 3).

Higher fertilizer demand showed up in spades in the company’s latest earnings report: in the third quarter, sales spiked 49%, earnings jumped 224% and free cash flow soared 142%.

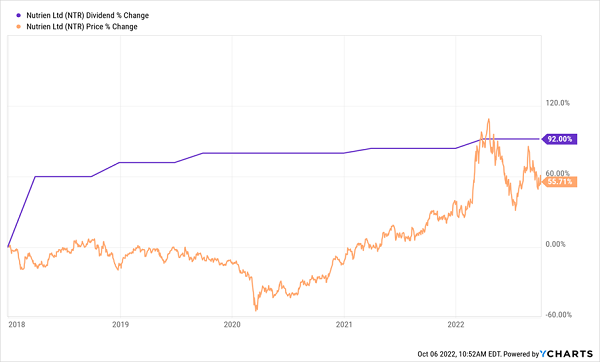

Those results haven’t flowed through to dividends—yet. The stock yields 2.3% today, but I expect that to rise quickly for folks who buy now, as Nutrien’s last 12 months of payouts accounting for just 38% of earnings and a mere 15% of free cash flow. That low cash flow payout ratio means Nutrien could triple its payout tomorrow and still be below my 50% “safety limit.”

Meantime, the stock’s “Dividend Magnet” continues to pull its share price higher. I expect the gap to close again—especially with Nutrien likely to surprise investors with a substantial dividend hike, more buybacks or both:

Nutrien’s Dividend-Share Price Gap Shows Our Upside

Speaking of buybacks, management has reduced Nutrien’s share count by an incredible 60% in the last five years. With the stock trading at an absurdly low 5-times (!) forward earnings, we can expect the company to keep buying its own stock with both hands. That’s a bullish sign for us.

My “Perfect Income Portfolio” Is Purpose-Built to 4X Your Retirement Income

I’ve built a complete portfolio of stocks and funds that delivers what every retiree (or wannabe-retiree!) needs: safe, stable and high dividends that hold up through any crisis.

Sure, the “perfect” in the name may sound confident—arrogant, even. But investors across America are using it to collect 7%, 9% and even 10% income today, which is far more than the paltry 1.6% the average S&P 500 stock pays.

Here are the four things this unique portfolio does:

- Pays you consistently, reliably and predictably (of course!)

- Contains undervalued, overlooked investments, which research shows have a far better chance of soaring than the overvalued, popular names most folks buy.

- Takes just a few minutes every month to “manage.”

- Does NOT involve day trading, buying on margin or any other risky strategy.

- Does NOT involve gambling on penny stocks, bitcoin or buying puts and calls.

I want to take you on a personal guided tour of this one-of-a-kind income portfolio now. Click here and I’ll show you the inner workings of this portfolio, which I’ve built to hand you the steady 7%+ dividends you need, whether you’re in retirement or reinvesting your dividends.