It’s the No. 1 retirement question: how much income do you need to quit the 9 to 5?

Today I’m going to help you find your number.

The best place to start is by asking yourself how your post-retirement lifestyle goal stacks up that of the average working American. Do you want to live lavishly or closer to the middle class?

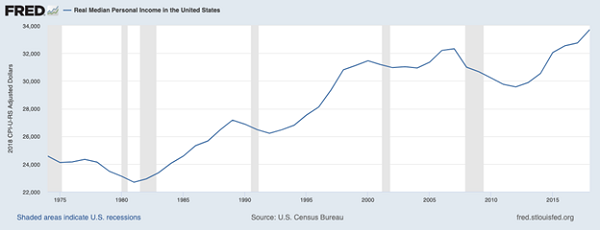

Once you’ve answered that question, the next step is to look to this number: $33,706.

Average American Incomes

According to the Federal Reserve, that’s the average income an American worker earns, and it gives us a handy jumping-off point. This figure has been rising lately, but has stayed stable over the long haul. In the last 20 years, real personal incomes have risen just 7.1%.

So let’s say you want to pull in an income stream in retirement that’s equivalent to that of the average American worker. You’ll need to withdraw $33,706 from your investments, rising on a 2% basis every year to cover inflation.

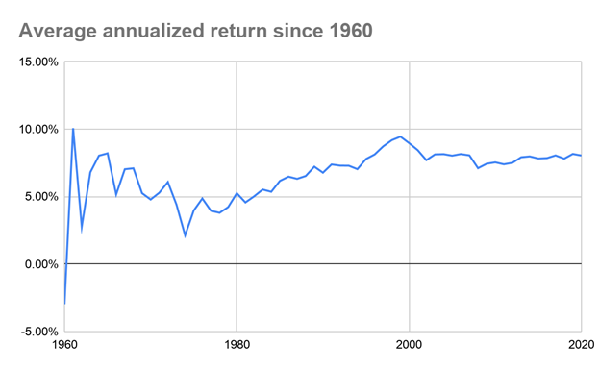

Now let’s look at what kind of return we can expect on our nest egg. We’ll be conservative and look back over 50 years of stock-market performance. In that span, returns have been 8.1% annualized, on average, and that average has held relatively steady for about 30 years:

Source: CEF Insider

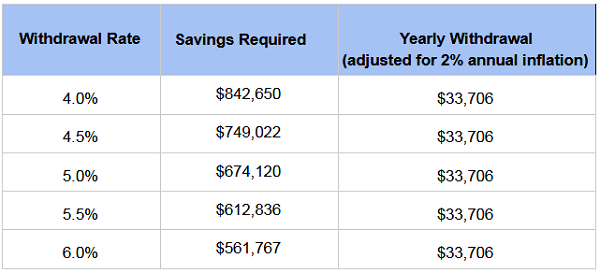

So we can expect stocks to give us, over the long term, an 8% return. Taking out 2% to keep up with inflation, we’ll need anywhere from a 4% to 6% yearly return on our portfolio to have a stable income stream in retirement that gets us a middle-class lifestyle without running out of money.

Here’s what that looks like, assuming your yearly rate of return exceeds your withdrawal rate:

With our very conservative inflation adjustments and reasonable expectations for market returns, we could get the average American into retirement with just $561,767, much less than the $842,650 required by conventional wisdom.

Getting the Income

Now that we’ve set up savings goals, let’s tackle one final problem: the rate of withdrawal.

This is where the “4% rule,” a strategy touted by Wall Street, which says you can safely withdraw 4% of your portfolio every year without running out of money, runs into trouble. If you buy the Vanguard S&P 500 ETF (VOO) or some similar index fund that pays 2% or less in dividends, you’ll need to sell shares to make up your withdrawal rate, even if you’re at the most modest 4% withdrawal assumption.

The critical factor here? Timing.

Sell at the wrong time, say at the trough of a recession, and you’re forced to do so at rock-bottom prices, so you’ll need to sell more shares to get the cash you need, slashing your future income stream as you do.

Timing Is Everything

Of course, timing the market is extremely difficult. Even professionals get it wrong a lot of the time.

7.1% Dividends, 0% Withdrawals: the Key to a Low-Stress Retirement

Luckily, there’s a simple approach we can use to eliminate the risk of selling at the wrong time and ruining our retirement, while keeping our nest egg intact (and growing). It’s a unique group of funds called closed-end funds (CEFs).

Many of these funds are managed by the titans of the hedge-fund world, like DoubleLine, as well as the investment-banking and asset-management world, like BlackRock and Morgan Stanley.

Take, for example, the Nuveen Tax-Advantaged Dividend Growth Fund (JTD), which, as you’d expect from the name, minimizes your tax burden by selling strategically to limit capital-gains taxes, while also focusing on stocks with high cash flow that shell out big dividends, such as JPMorgan & Chase (JPM), Microsoft (MSFT) and UnitedHealth Group (UNH). JTD has been crushing it for a long time:

Imagine Holding This Fund in Your Retirement Portfolio

What’s really important is the income: JTD’s 7.1% yield is more than enough to cover even a 6% withdrawal rate, meaning you may be able to retire on dividends alone, without having to sell a single share. Instead, you can leave it to the professionals at Nuveen to do the buying and selling for you while they keep that juicy 7.1% income stream flowing.

This Massive 8% Payout Could Give You $44,941 Every Year, Forever

What if I told you that a 7.1% dividend was on the lower end for closed-end funds? And that I’ve uncovered 5 CEFs yielding 8%, on average, that are perfect for your retirement portfolio now?

In other words, if you took the $561,767 from the example above, you’d generate $44,941 in yearly dividend cash with this 5-fund “mini-portfolio.” For many folks, that’s more than enough to retire on dividends alone and forget about the impossible task of trying to time the market.

Then there’s the upside.

With CEFs, the key number to look at is the discount to NAV. We don’t have to get into the weeds, but suffice it to say, this number is the difference between the fund’s market price and the value of its portfolio.

I’m sure you see where I’m going here.

To reap big gains from CEFs, we simply need to wait until the fund’s discount gets unusually wide, then strike—and ride the price back up as the discount window “slams shut.”

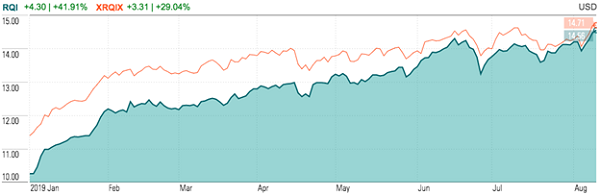

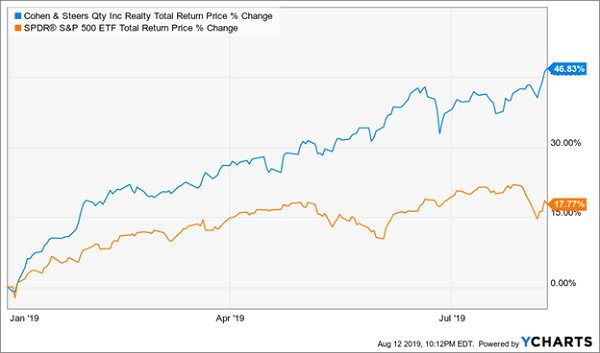

It’s a pattern I’ve seen time and time again, like with the little-followed Cohen & Steers Quality Income Realty Fund (RQI), owner of high-quality real estate investment trusts (REITs) and payer of a monthly 6.8% dividend today.

Back on December 27, 2018, it was trading at a ridiculous 13% discount to NAV. So buying then meant you got every dollar of the fund’s assets for just $0.87!

Absurd discounts like this don’t exist anywhere else in the investing world. But they happen all the time with CEFs. Over the following 8 months, RQI’s discount slowly bubbled away, closing from 13% to just over 1%:

RQI’s Shrinking Discount …

And driving a swift 47% gain!

… Powers a Fast Double-Digit Return

As I said, I’ve seen this dead-simple (and totally predictable) pattern happen over and over again, and my I’ve got these 5 fund picks pegged as the next big gainers, with a forecast 20%+ in price gains over the next 12 months, to go along with their fat 8% dividends!

I’ve got everything you need to get in on the action now. Click here to get full details on these 5 funds: names, tickers, buy-under prices, complete dividend histories and all the facts you need before you buy. Don’t miss out!