“Regular” REITs typically buy physical properties, find someone to manage them, and lease them out. They collect rent checks and avoid paying taxes on most of these profits if they distribute 90% of their profits as payouts. This is the reason REIT stocks typically boast big yields.

Mortgage REITs (mREITs), on the other hand, don’t own buildings. They own paper. Specifically, they buy mortgage loans and collect the interest. How do they make money? By borrowing “short” (assuming short-term rates are lower) and lending “long” (if long-term rates are, as they tend to be, higher).

This business model prints money when long-term rates are steady or, better yet, declining. When long-term rates drop, these existing mortgages become more valuable (because new loans pay less).

Of course, the traditional mREIT’s gravy train derails when rates rise and these mortgage portfolios decline in value. Historically, rising rate environments have been very bad for mREITs and resulted in deadly dividend cuts.

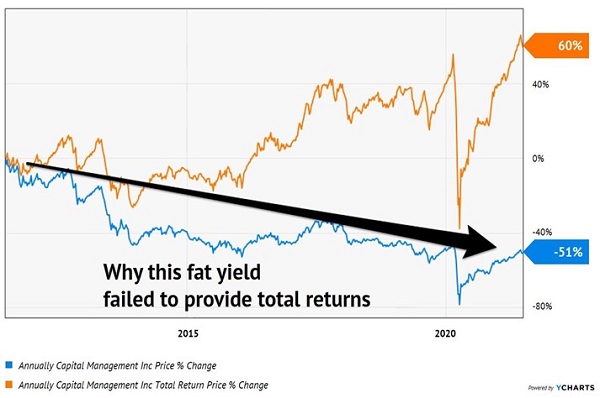

For example, Annaly Capital (NLY) investors took it on the chin during the rate hike cycle from June 2004 to June 2006, when Alan Greenspan boosted rates from 1% to 5.25%. Everyone knew higher rates would be problematic, but NLY investors didn’t run for the exits until after it chopped its payout in mid-2005.

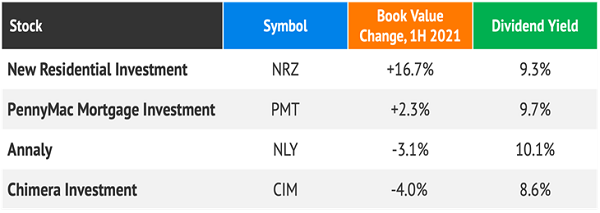

Of late, NLY has made efforts to hedge its portfolio from rising rates. The firm always pays a huge dividend—the shares yield 10.1% as I write—but stock price declines weigh on total returns. So, over the past decade, the stock is up only 60% and due only to the dividends. Not awful, but these returns don’t even add up to that stated payout:

Overpromising Payouts

But savvy mREITs are positioning their portfolios for higher rates. New Residential Investment (NRZ), for example, is now the largest non-bank owner of MSRs in the world.

Mortgage service rights (MSRs) are contracts that give the holder the right to collect payments from a borrower. These aren’t the loans themselves; they are the rights to service these loans—a subtle but important difference.

Fixed-rate loans—like mortgages—become less valuable as rates rise. MSRs, on the other hand, rise in value along with rates (and they generate more cash flow and profits).

My wife and I just refinanced our home, and we now have a new mortgage servicing company, Truist Bank. Truist is collecting about 0.25% of our payments for the remaining 15 years of our mortgage. With our account already on autopay, this is truly easy money for Truist.

The bullish promise for MSRs is reflected in the book value of NRZ. Its book soared 16.7% in the first half of 2021 thanks to the move in mortgage rates:

NRZ’s MSRs Soar in Value

If you believe that rates have more upside than downside from here, then the first half of 2021 was a fine dress rehearsal. NRZ, as you’d expect, performed perfectly:

Let’s face it, our intrepid Federal Reserve has printed a LOT of money. These unprecedented actions are setting up the biggest retirement disaster in the history of this country.

Traditional inflation plays like gold and silver are not the answer. Crypto is a casino. No, we retirees need income-producers like NRZ, stocks that pay a big dividend today and will soar tomorrow when the CPI numbers start coming in hot, hot, hot.

If you like a 9.3% dividend with serious price upside, then you’ll love my Inflation Retirement Storm portfolio. Click here and we’ll discuss more, including names, tickers and buy prices.