Generally speaking, we like monthly dividends better than quarterly payouts. I mean, why wait 90 days to get paid when “every 30” is possible?

Here’s another great thing about monthly divvies—they often have big fat annual yields attached to them.

For example, today we are going to discuss a batch yielding between 8% and 19.8%. On a modest $500,000 in savings, these monthly machines will dish between $40,000 and $99,000 per year!

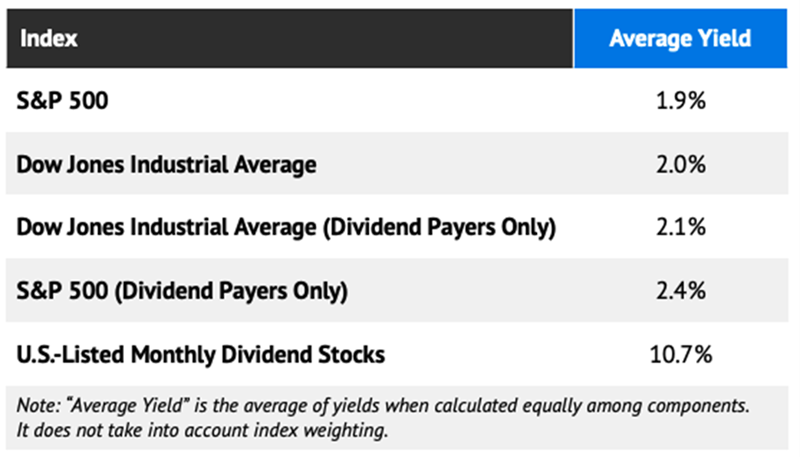

If we randomly select a few monthly dividend payers, chances are we’ll earn (way!) more. Here’s the difference between the stock market’s monthly dividend stocks and the major indices:

Dividend heroes or yield traps? Let’s look at this four pack in more detail.

Sabine Royalty Trust (SBR)

Distribution Yield: 8.0%

We’ll begin with a rarity among rarities—Sabine Royalty Trust (SBR).

Royalty Trusts are among the most passive income vehicles on the market. They exist to own shares in income generated from natural resources (crude oil, natural gas, minerals, etc.), which they turn around and pay back to unitholders, less costs, in the form of distributions. Sabine Royalty Trust, for instance, receives Sabine Corporation’s landowner royalties, overriding royalty interests, minerals, production payments, and more from proved but undeveloped oil-and-gas properties in six states, predominantly in the Permian Basin.

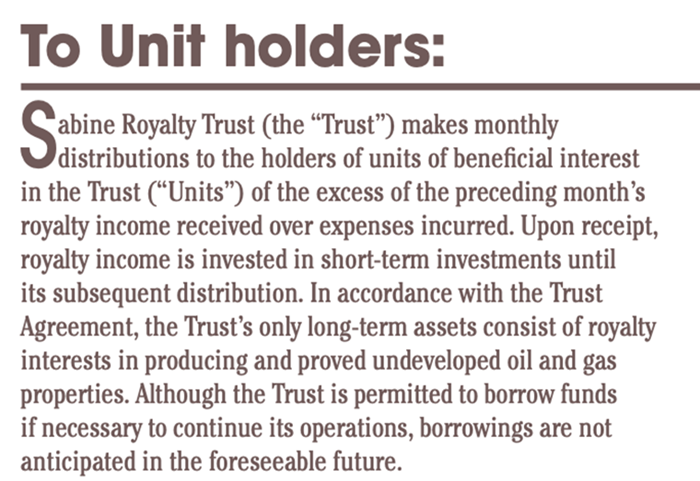

How central are distributions to royalty trusts’ existence? Here’s the first paragraph from the first page of SBR’s most recent earnings report:

Source: Sabine Royalty Trust Q2 2025 Earnings Presentation

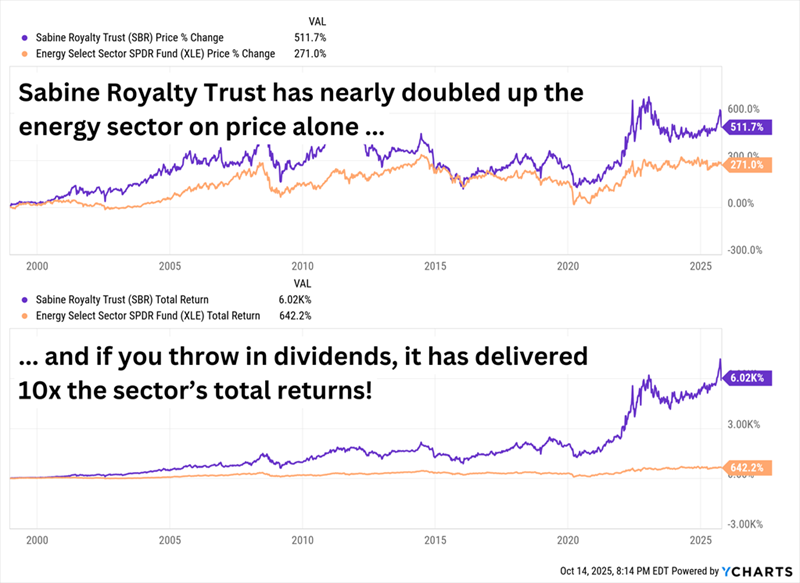

Who can argue with a business that has no debt, pays a generous monthly distribution that by nature has to be covered, and has run laps around the broader energy sector?

Why Drill for Oil When Collecting Royalties Is So Much More Lucrative?

Well, there are a few oddities we must address.

Sabine Royalty Trust won’t be with us forever, for one. While it technically has no termination date, the company was established to fizzle away one day. Its asset base was established in 1983, and those assets are fixed—SBR can’t acquire new ones, so when their current assets are depleted, they’re gone. The trust itself would likely terminate shortly before that. SBR will terminate if there are two successive fiscal years in which Sabine’s gross revenues from royalty properties are less than $2 million per year, or if unitholders vote for a closure.

Because SBR only collects royalties, it’s extremely sensitive to commodity prices, so it can be far more volatile than the energy sector. The distribution isn’t predictable, either—over the past five years, distributions have ranged between 2.7 cents per share and $1.14 per share. Those distributions aren’t tax-efficient, either; they’re considered ordinary income, so we’re taxed at our marginal rates.

Capital Southwest Corp. (CSWC)

Dividend Yield: 12.7%

Capital Southwest Corp. (CSWC) is a business development company that provides capital to lower middle market firms with EBITDA (earnings before interest, taxes, depreciation and amortization) of between $3 million and $25 million. Its current portfolio stands at 122 firms—roughly 90% of its deals are first-lien loans, 9% are equity, and the rest are a sprinkling of second-lien and subordinated debt.

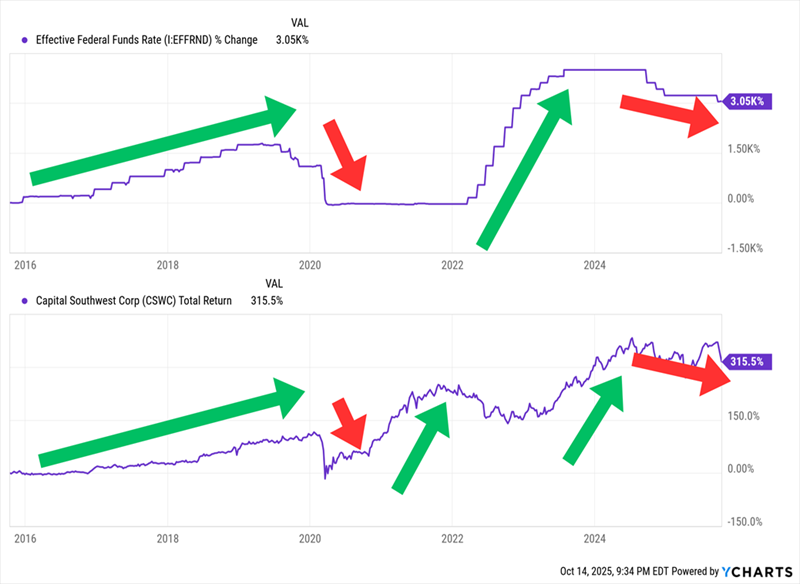

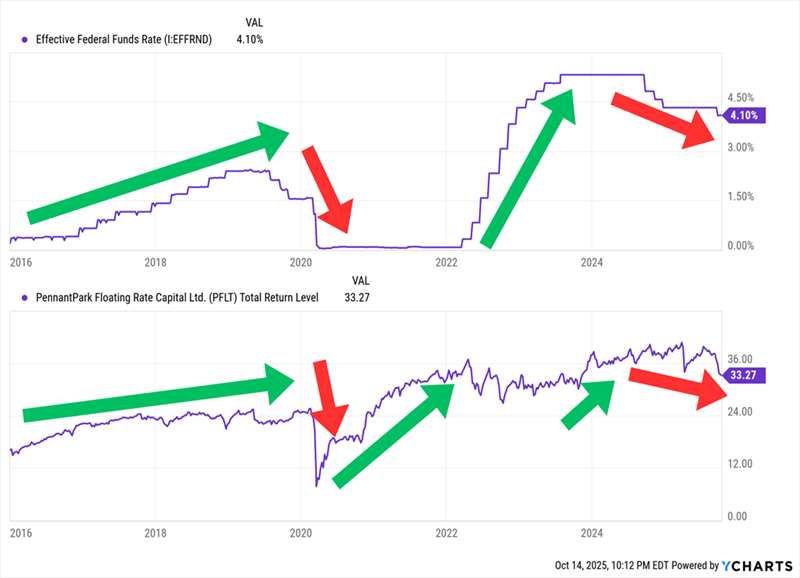

The blessing and (more so at the moment) curse of many BDCs is that they deal in a high percentage of floating-rate debt, which is outstanding when rates are rising, less so when they’re declining. And the stock market being what it is, sometimes the connection isn’t perfect—BDCs can just as easily trade on expectations for policy as it can the policy itself:

Still, It’s Clear the Fed Has a Lot of Say in BDC Performance

However, in CSWC’s case, some Fed pain now might be a blessing in disguise.

The BDC industry is a difficult one that, as a whole, tends to lag the market. But a few individuals stand out, and CSWC is one of them, clobbering its peers and outperforming the S&P 500 over the long term. It’s internally managed (so external managers aren’t bleeding fees from it), it has moderate leverage, the dividend is well-covered and, as of summer 2025, those dividends are paid on a monthly basis. Most of its high dividend is attributable to its regular dividend, but CSWC kicks in supplementals that account for another percentage point or so of yield.

So why would lower rates be a blessing for a company that wants higher rates? They won’t be—at least not for Capital Southwest. But they could provide a little relief for prospective buyers who don’t want to pay the current 21% premium to net asset value (NAV) for shares.

PennantPark Floating Rate Capital (PFLT)

Dividend Yield: 14.0%

Another BDC, PennantPark Floating Rate Capital (PFLT), which targets midsized companies that generate $10 million to $50 million in annual EBITDA.

PFLT effectively invests us in more than 190 portfolio companies spread across over 110 PE sponsors. It’s also a “value-added” BDC that lends its expertise in specific industries, hence its portfolio focus on five categories: health care, software and technology, consumer, business services and government services.

And the name pretty much says it all. PennantPark Floating Rate does about 90% of its funding through first-lien debt, almost all of which is floating-rate in nature. (The remaining 10% is made up of equity co-investments and joint venture equity.)

Like with CSWC, it’s clear that rates are the straw that stirs PFLT’s performance.

Though PFLT Hasn’t Been Nearly as Strong a Performer as CSWC

I’ve previously looked at PFLT and noted that its dividend coverage was getting tight. It’s getting tighter, too, with the dividend outstripping NII across a few quarters over the past year-plus. A dividend reduction is at least in the realm of possibility, though management believes that joint venture growth (including a new JV, PennantPark Senior Secured Loan Fund II) and additional leverage can help it meet its NII needs. Wall Street may be a little skeptical; PFLT trades at a 20% discount to NAV.

Orchid Island Capital (ORC)

Dividend Yield: 19.8%

REITs are well-known for their above-average dividends, but if we want to test the upper limits, we want to look at mortgage REITs.

Most REITs are equity REITs, which own (and sometimes operate) physical real estate. But mortgage REITs purchase stacks of paper with a business model that goes something like this:

- Borrow money at short-term rates.

- Buy bundles of mortgages (securitized mortgages)

- Collect the income these mortgages produce at (hopefully higher) long-term interest rates.

And whereas you can commonly find nice yields in the mid-single-digits among equity REITs, it’s extremely common to find double-digit yields in the mREIT space.

Orchid Island Capital (ORC) is one such mREIT dealing in agency residential mortgage-backed securities (read: Fannie Mae, Freddie Mac, etc.), including fixed-rate pass-through securities, interest-only securities and inverse interest-only securities. It’s externally managed and advised by Bimini Advisors. And its yield is in the stratosphere, currently just shy of 20%.

We discussed another mREIT with a rising dividend a couple weeks ago, and I mentioned that “Generally speaking, the Federal Reserve’s easing should be a boon for mREITs, including the potential for improving originations in the residential space.”

In fact, you can see ORC’s improving health over the past two years or so as the rate environment has improved.

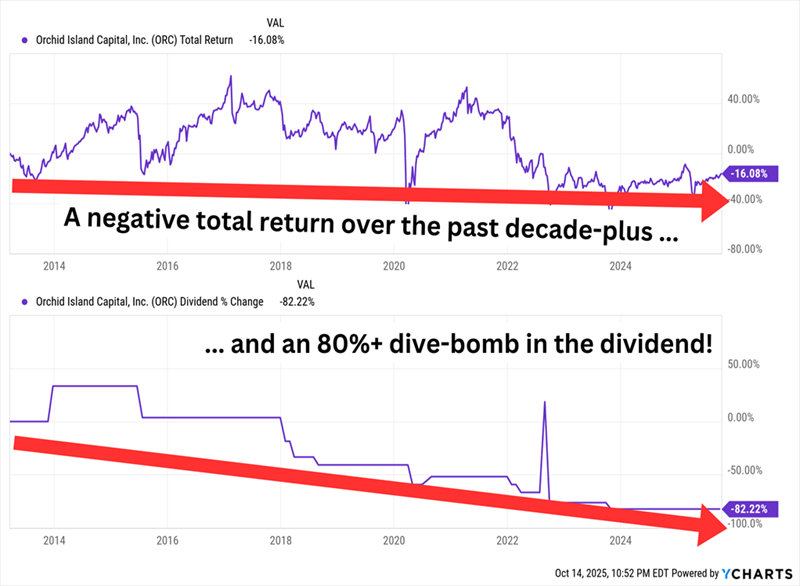

Unfortunately, You Can See Something Else, Too

Orchid Island’s long-term total return since its 2013 initial public offering is bad enough. But the massive dividend papers over a trainwreck of a price performance, with shares off 90% since that IPO. The declines have been so precipitous that just a few years ago, ORC had to initiate a 1-for-5 reverse stock split; without it, shares today would trade for less than $2.

And as the chart above shows, ORC has no compunction about reducing its dividend at the drop of a hat.

Monthly Dividends of 9%+ We Can Actually Count On!

I prefer to collect monthly dividends without the anxiety of wondering when the next axe will fall.

If you’re a long-term investor who wants those frequent payouts at an elite level, but from more dependable payers, you can’t do much better than the low-drama, high-yield payers in my “9%+ Monthly Payer Portfolio.”

Don’t let the name deceive you. The “9%+ Monthly Payer Portfolio” isn’t just about earning high levels of yield—it’s about earning high levels of yields by leveraging steady-Eddie holdings that won’t leave you reaching for the Pepto every time the economy hiccups or Jerome Powell sneezes.

You also won’t need to stress about the size of your nest egg. Unlike many retirement plans that require you to bleed out your savings as you age, the income this portfolio can generate is so rich, it can sustain a retirement on dividends alone.

Here’s the math: A mere $500,000 nest egg—less than half of what most financial gurus insist you need to retire—put to work in this powerful portfolio could generate a $48,000 annual income stream.

That’s $4,000 every month in regular income checks!

Even better? While the current bull run has many stocks priced for perfection, many of these monthly dividend stocks still remain in our “buy zone” … but they might not be for much longer. So click here to learn everything you need about these generous monthly dividend payers right now!