We contrarians stayed calm through the market’s fourth quarter hissy fit. We not only held onto our shares through November and December but we also added dividend payers opportunistically to our portfolios.

Now, it’s time for us to be a bit more conservative. Most US stocks have rallied so much that they are now “overbought.” This means they’ve gone up pretty far pretty fast and are due for a breather (or, perhaps, another correction).

Of course certain elite dividend growers are still good long-term buys at current prices (aren’t they always). And a select five-pack of these picks also represents solid short-term purchases as well.

Why should you care about the short run? Well, maybe you shouldn’t! Getting the near term right isn’t a requirement for a successful retirement, after all.

However, if you are speculating on short term moves – such as selling put options, or writing covered calls, or simply trading in days, weeks and months – then you should pay attention to timing.

I do this for my Options Income Alert subscribers. We pick out dividend growers that fulfill the following criteria:

- We have identified a “dividend magnet” ready to pull the current share price higher.

- We’d like to own the stock at a discount to its current price.

- And my research and indicators favor these stocks in particular in the weeks and months ahead.

Let’s start with the first concept because it’s the most important. Dividends are magnets that pull their share prices along with them. If you’re looking for the stock market’s tail that wags the dog, pay attention to the payouts attached to a given share price.

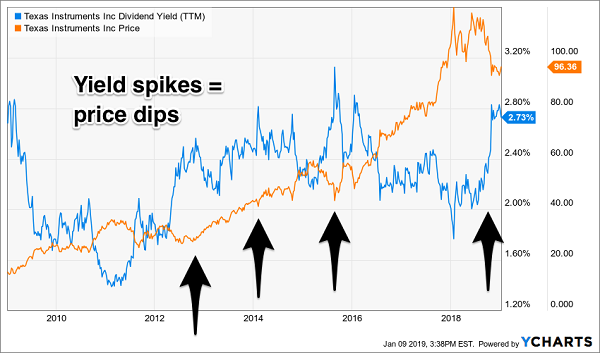

Regardless of what the stock market does during any given trading session (or month, or whatever), we can stack the income odds in our favor by only selling puts on dividend growers we’d be thrilled to buy at a discount anyway. For example, let’s consider Texas Instruments (TXN), which has increased its payout (orange line below) by an amazing 600% over the last decade. Its stock price (blue line) was pulled higher by its payout:

TXN’s Dividend Magnet

The best time to buy a stock like TXN is nearly anytime. But we can “cherry pick” our entries (and put option sales) by focusing on times when TXN’s yield is higher than usual. These spikes in yield tend to be temporary and they often point out good dips to buy:

Buy the Dip (or High Relative Yield)

Thanks to the firm’s recent 24% dividend hike, the stock will pay 2.9% over the next 12 months (more than its 2.6% trailing yield).

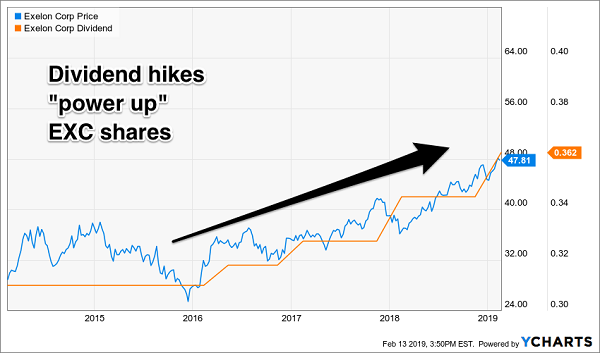

Moving on, in an overbought environment like this one, it helps to look for the laggards. Let’s consider regional monopoly Exelon (EXC), which took a beating eleven years ago when natural gas prices collapsed.

Since then this rare “growth utility” has steadily gotten things together under CEO Chris Crane’s leadership. (And a competent manager is often all you need when you have a regional monopoly. Crane is excellent.) After years of paying a steady but static dividend, EXC recently raised its payout for the fourth year in a row. Wall Street is beginning to appreciate this unfolding “dividend growth” story:

EXC’s Dividend Growth Drives Share Price Growth

Shares pay 3% today, and investors will likely settle for less (meaning they’ll pay a higher price) as EXC establishes itself as a growth utility.

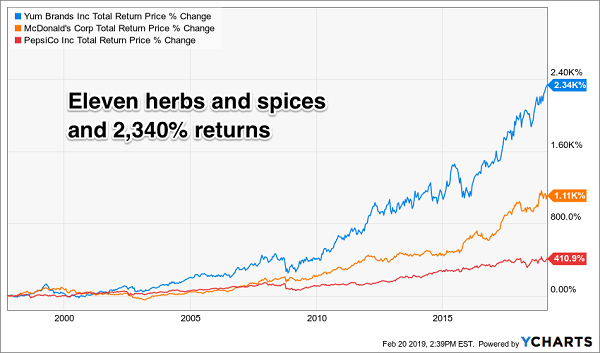

Next let’s order up a quick growing fast food company that its parent probably wished it still owned. Twenty-one years ago, PepsiCo (PEP) spun off its restaurant business into a separate company. A $10,000 investment in Yum Brands (YUM) at that time would be worth more than $230,000 today.

Yum has run circles around its old parent and “gold arches” industry standard McDonald’s (MCD) too:

Mouth Watering Returns for Yum

Yum’s secret? It’s bet heavily on international growth and expansion for the past two decades. Its KFC brand was the first Western fast food company to open a restaurant in China. Today, Yum’s overseas KFCs, Taco Bells, Pizza Huts and WingStreets account for about half of the firm’s total profits.

The firm has hiked its dividend payout by 40% over the past two years. As long as it keeps deploying Colonel Sanders internationally, shareholders should continue to enjoy higher dividends and higher share prices.

Next up we have a company growing its free cash flow (FCF) by 117% over five years and its dividend by 167%. Wouldn’t that thrill any investor? Not so for hedge fund mega-shareholder D.E. Shaw & Co., which believed that Lowe’s (LOW) could do better.

Two years ago, the firm posted cameras in Lowe’s parking lots, compared them with images from top rival Home Depot (HD) and took Lowe’s management team to task for underperforming the competition!

Not Busy Enough

Then-CEO Robert Niblock made the self-preserving comment that he valued the “constructive discussions.” As you’d expect, these productive talks eventually ended with Robert looking for a new employer!

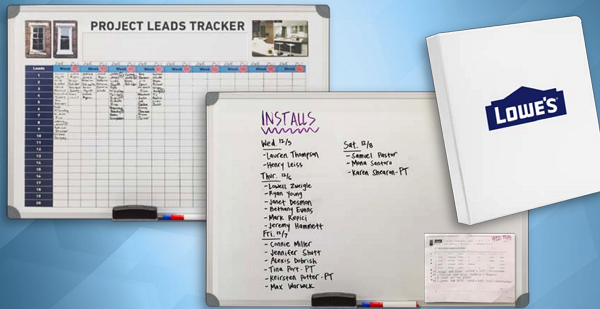

Last July the new-look board of directors installed Marvin Ellison, a respected Home Depot veteran, as new boss. And Ellison was, well, less than impressed with what he saw. He popped by a store and asked a group of associates how they’d manage a particular kitchen project for their customer.

They took him to the back of the store to show him their project management system – a dry erase board.

“Well, the customer doesn’t have a dry erase board,” replied Marvin. “So how do they keep track of the project?”

They replied: “Well, Marvin, we give them a binder.” How very…last century!

Marvin Was Not Impressed by This Technology

Turnaround investing opportunities can be quite lucrative. When a stock’s news improves from “bad” to merely “mediocre” (by moving from, say, dry erase boards to computers), share prices often skyrocket. (“First-level” investors don’t realize that stocks trade off of current perceptions and hopes about the company. When these change – for better or for worse – the share price often moves in the same direction.)

Let’s close with a quiz of your magnet knowledge. By now you know that dividend hikes are the driving force behind higher stock prices. They are also quite predictable. So, why not “front run” the good news and buy shares ahead of a hike?

For example, Dollar General (DG) is due for a dividend raise early this spring. Since the discount retailer began paying a dividend in 2015, it’s hiked its payout this time of year like clockwork:

Spring Has Sprung When Dollar General Hikes

Dollar General qualifies as “Amazon-proof” thanks to its low price tag items (which don’t make sense to ship). Thanks to its unique market positioning, the stock quickly shook off the stock market’s “December disaster” and is again approaching all-time highs.

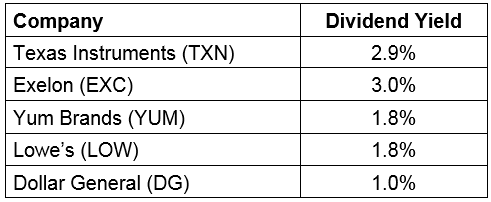

The only problem with buying these stocks on your own? These yields:

At 2.1% this five-pack will only get you $21,000 in annual income on a $1 million portfolio. If you’re simply buying and hoping, you’re sure banking on a big spring of price appreciation!

Fortunately we can take chance out of the equation by using one of my favorite income strategies. Let me explain…

Just Released: How to “Force” a 7.5% Dividend From TXN, EXC & More

I’ve found 4 mysterious “Dividend Conversion Machines” that let you rewind the clock: buy stocks like TXN, EXC and more, but instead of grabbing today’s 4.4% dividend, you’ll get the same incredible 7.5% CASH payout folks who bought in 2009 bagged instead!

But there’s a vital difference: you won’t have to take a stomach-churning plunge to get it, like you would have back then.

Sure, handy slogans like “Buy when there’s blood in the streets” are easy to say. But actually overcoming fear and hitting the buy button at a time like that is almost impossible for most people.

But with these 4 amazing “Dividend Conversion Machines,” you’ll grab the same massive dividend yields (7.5% to 8% or more) that the best blue chips never quite pay right now—TODAY.

And these life-changing payouts are safe, backed by these very same household-name stocks.

Massive Upside and 7.5% to 8%+ Dividends—in 1 Buy

What’s more, you can grab these lofty payouts whenever you’re ready: all at once, on an automatic yearly or monthly schedule … or simply whenever you have new money to invest.

It’s all up to you!

Best of all, each of these 4 incredible investments are about to explode and give us massive price upside, too.

How massive?

I’m talking 20%+ yearly price gains, on top of dividends of 8%, 10% and up.

Just days ago, I released the whole incredible story on these 4 Dividend Conversion Machines to the public for the first time, including their names, ticker symbols, exactly how they work and how you can buy (hint: you can grab these 4 incredible Dividend Conversion Machine straight from your brokerage account.)