Your 2% bonds are going to make you broke. You need to buy these safe, higher paying dividends instead.

We’ll get to these “real yields” (up to 9.3%!) in a moment. First, let’s recap. Treasury yields just took their biggest bath in weeks, sending the 10-year T-note to 2%. Less than a year ago, the 10-year was flirting with (a not exactly nosebleed) 3%.

And now that Fed chair Jay Powell has fallen in love with the doves (whether by choice or by force), he’s going to keep rates low for a long time. Which means bonds will have no place in a retirement portfolio geared towards income.

It wasn’t always this way. Decades ago, bonds rightfully earned their reputation as a source of not just safe, but substantial income that could actually support a high-quality retirement.

But Times, They’ve Been A-Changin’

But for nearly a decade, investors subject to traditional wisdom have been put in peril. They’ve been told that bonds are safe, that they’re “wealth preservers.” However, they now yield so little that their income is almost completely gobbled up by inflation, and their paltry coupons don’t even support basic necessities.

Put another way: If you rely on plain-Jane bonds in retirement, you’ll be underwater paying for even the most bare-bones lifestyle.

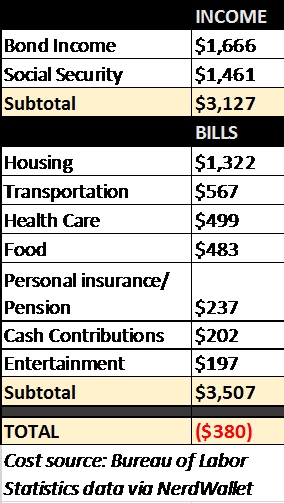

The table below shows the monthly income from a $1 million nest egg 100% invested in Treasuries, as well as the average Social Security paycheck, stacked up against a list of basic retirement costs compiled by NerdWallet.

Bond investors come up $380 shy each and every month under this low-frills budget. And even if they didn’t spend a penny in “entertainment,” they’d still be broke.

This “new normal” requires a different set of income strategies. You need better yields and substantial payout growth to make sure you’re ahead of the inflation curve.

Of course, you’re not going to get those from Uncle Sam at 2%. You will, however, find them in this five-pack of bigger paying bonds.

BlackRock Core Bond Trust (BHK)

Type: Multi-Sector

Distribution Yield: 5.6%

The BlackRock Core Bond Trust (BHK) closed-end fund (CEF) lives up to its name, providing a core collection of primarily investment-grade bonds. Investment-grade corporates make up about a third of the portfolio, with double-digit holdings in U.S. government bonds, junk debt and agency mortgages. It also holds developed- and emerging-market debt, securitized products, bank loans and more.

About three-quarters of the portfolio is rated BBB or above, so quality is no issue. And you even have roughly 15% exposure to international debt, which gives you a splash of geographic diversity.

A core ETF such as the iShares Core Aggregate Bond ETF (AGG) will offer typically a little better overall credit quality, but less than half the yield. That’s the power of closed-end funds, which can use leverage and wily active management to juice returns and distributions.

A 7% discount to the fund’s net asset value (NAV) would seem to cinch the deal. After all, who wouldn’t want broad bond-market exposure with 2x the yield for 93 cents on the dollar?

The problem is that there are better options. BHK has delivered 7.1% in annual total returns since inception, versus a 7.6% category average. Plus it has underperformed in most other time periods, too.

Luckily, BlackRock has more to offer, as I’ll show you in a minute.

Calamos Convertible & High Income Fund (CHY)

Type: Multi-Sector

Distribution Yield: 9.3%

Calamos offers another type of somewhat-blended fixed income, though it’s far from the “core” allocation you’d get via BHK.

The Calamos Convertible & High Income Fund (CHY) invests in a portfolio of convertible securities and other high-yield fixed income instruments. Convertible securities are the lion’s share at 57%, followed by corporate bonds at 32%.

Convertible bonds get very little press. They’re like traditional bonds in that they make regular, fixed coupon payments. But as the name implies, they can be converted–into common stock. So, you can enjoy the income of bonds with the potential upside of equities.

While convertibles’ yields are typically less than regular bonds, CHY’s other holdings, as well as a hefty amount of leverage, help fuel a massive distribution of more than 9% despite a slight reduction in the payout late last year. Its 7.7% annualized total return since inception is in line with the category average.

A 3% discount to NAV is a bargain considering CHY has traded at a premium on average over the past year.

Convertibles Are Cruising in 2019

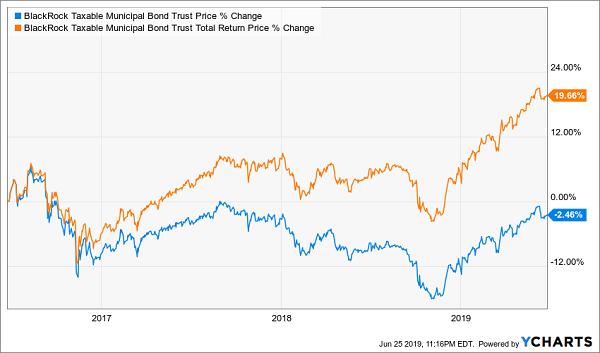

BlackRock Taxable Municipal Bond Trust (BBN)

Type: Taxable Municipal

Distribution Yield: 6.1%

It’s hard to read “taxable municipal bond” without doing a double-take. Isn’t the whole appeal of a municipal bond the fact that you get to pull a fast one on the IRS?

Sure, tax-free munis can offer smaller yields thanks to that tax benefit. But what happens when you collect that income in a tax-advantaged account like an IRA?

That’s right: You lose municipal bonds’ primary perk.

Enter the BlackRock Taxable Municipal Bond Trust (BBN), which invests at least 80% of its assets in taxable munis, including Build America Bonds. The fund can, if necessary, invest in other assets, from Treasuries to even tax-exempt bonds, but it mostly stays faithful to its charge.

There’s plenty to like here. BBN is able to juice a 6.1% yield its taxable municipal bonds, which it has converted into a 9.4% average annual total return since inception. That’s better than the category mark by 50 basis points. And you can purchase that outperformance at a tidy little discount of about 4% to NAV right now.

That makes BBN an unorthodox but nonetheless attractive buy.

High Taxable Muni Yields Get BBN Over the Hump

Cohen & Steers Limited Duration Preferred & Income (LDP)

Type: Preferred

Distribution Yield: 7.6%

I love preferred stocks. These under-covered, under-loved “hybrid” securities fall well off the radar of many investors. But for those in the know, they’re a dependable source of high yield.

Cohen & Steers skims a lesser-traveled area of the preferred world with its Limited Duration Preferred & Income (LDP) closed-end fund, which, as the name suggests, invests in low-duration preferreds. Just like many investors will duck into low-duration bonds to fight off interest-rate risk, they can tap into this fund when they’re worried about rising rates.

Given the Fed’s current disposition, that’s a big strike against it for now. So is a mere 2% discount that sits below its 52-week average discount of about 5%. (In other words, we’re likely to see this fund trading at a bigger bargain down the road.)

But I always make sure to have a plan for every market condition, and that includes an eventual return to rising rates, whenever that might be. Under that condition, LDP and its collection of about 150 holdings–including preferreds from JPMorgan Chase (JPM) and Bank of America (BAC)–will be the right way to play this asset class.

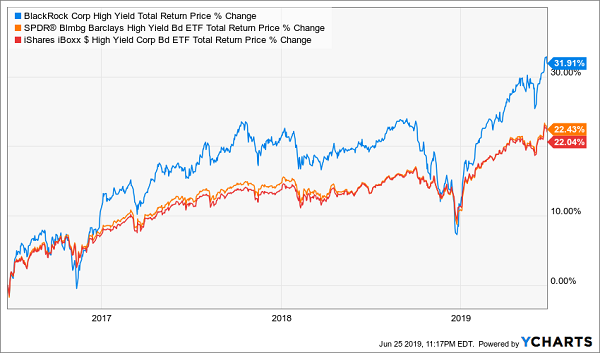

BlackRock Corporate High Yield Fund (HYT)

Type: High Yield

Distribution Yield: 8.1%

Junk debt has looked less like a fixed-income product and more like a hard-charging blue chip in 2019. That has led to stellar returns for the likes of the BlackRock Corporate High Yield Fund (HYT).

BlackRock’s HYT: Don’t Throw This Junk Away!

HYT’s more than 1,100 holdings aren’t exclusively junk debt, of course. While 83% of the fund is dedicated to junk, another 11% of assets are piled into term loans, with a peppering of collateralized loan obligations, preferred stocks and other assets.

This closed-end fund takes chances, too. Only a little more than a third of the fund is in the highest credit-quality level of junk (BB); much more is in B (45%), and another 14% is dedicated to CCC-rated bonds. That’s much farther down the ladder than what you get in typical junk index funds such as iShares iBoxx $ High Yield Corporate Bond ETF (HYG) and SPDR Bloomberg Barclays High Yield Bond ETF (JNK). BlackRock’s managers double down on those risks, too, with a healthy 28% leverage ratio.

The chutzpah is worth it. BlackRock Corporate High Yield has stomped its category return, 8.3%-6.7%, since inception. And anyone who steps into the fund today can buy HYT’s high-performing assets at a 9% discount.

How Retirees Can Collect $3,125 Per Month in Dividends Alone

These CEFs all have one important trait in common: They distribute cash to shareholders not every quarter, but every month.

That’s a boon to retirees who will have to pay all their monthly bills with retirement income.

But how much will you need every month to get by?

The experts at Merrill Lynch say you need a $738,400 nest egg to retire. The talking heads on CNBC and Fox Business will tell you the magic number is $1 million or $1.5 million. Suze Orman collectively dropped our jaws when she said “You need at least $5 million, or $6 million. Really, you might need $10 million.”

$10 million?

They’re right—if you invest in low-yield bonds or the types of so-so-yielding blue-chip stocks that the financial media deems as “safe.” But there’s nothing safe about collecting so little income in retirement that you have to start taking large chunks out of your nest egg, which in turn saps your income potential even more.

But if you stockpile the picks in my “8% Monthly Payer Portfolio” —including my two favorite preferred stock plays, which each deliver uber-safe yields of more than 7%—you can bank on a comfortable retirement with a mere $500,000 nest egg.

In fact, you’d be collecting a fat $3,125 in pure income each and every month!

This easy, buy-and-hold dividend strategy can net you not just an average 7.5% annual yield, but also 10%-plus average price upside. That takes care of a critical retirement component that too many professionals overlook: The need to expand your nest egg in retirement because people are simply living much longer than old financial models are equipped to deal with.

You don’t need to learn some strange options tactics or complex trading routine. You can live off a $500,000 portfolio indefinitely by following just two simple steps:

- Sell off your “buy and hope” portfolio: The financial media has pushed so-called “safe plays” like Coca-Cola (KO) and Procter & Gamble (PG) on to investors for years. But these companies don’t deliver the kind of yield you need to maintain your current quality of life in retirement.

- Buy my 8 favorite monthly dividend payers.

That’s it!

This portfolio includes some truly amazing dividend stocks, including …

- An 8.6% payer that’s set to rake in huge profits from an artificially depressed sector.

- The brainchild of one of the top fund managers on the planet that’s giving out generous 9.1% yields.

- And a rock-steady 7.2% dividend trading at a massive discount to NAV.

Get these and the other monthly dividend picks, including two rock-solid preferred-stock plays, that will unlock $3,125 in monthly income right now–for free! Click here to receive each and every pick in my 8% Monthly Payer Portfolio—complete with tickers, buy prices and full analyses—at absolutely NO COST to you.