First-level investors think the key to retiring on dividends alone is to find the largest yields they can and ride them into the sunset.

But while it’s important to lock down fat yields—like the five-pack of 5.5%-10.4% yielders I’ll share with you today—that’s only part of the puzzle. We need two more things from our long-term income holdings:

- Dividend safety. A 10.4% payout is only helpful if it’s actually going to get paid for quarters and years to come. No dividend cuts, please.

- Principal safety. We’re also not looking to lose 10.4% per year in price. Or anything in price, for that matter. We want our principal to stay steady or better.

One of the best ways to find safe dividends that will protect our principal is in “low-beta” stocks. We could call them “low-heartburn” just as well. These are equities that move less than the broader market.

Perfect for us payout-focused investors.

Here’s a quick example of beta. Let’s say a stock has a beta of 0.5. It moves half as fast as the market.

If the S&P drops 10%, we would expect our 0.5 beta stock to be down only 5%. Less bad, in other words.

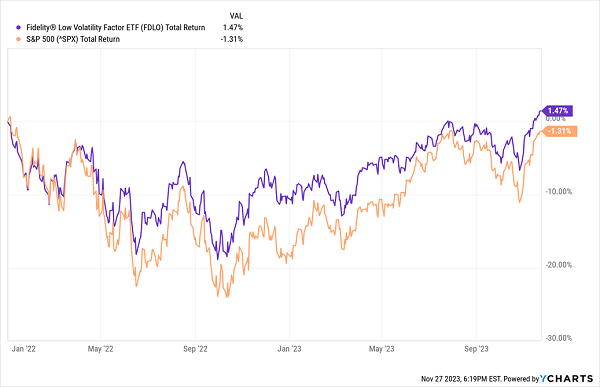

A low volatility (beta) strategy has performed well since the bear market started in 2022. A popular “low vol” ETF beat the market with—wouldn’t you know it—less heartburn.

Low Vol ETF Beats Broader Market

But as you know, we can do better than a lazy ETF! Today we’ll discuss five low-beta dividend stocks that pay between 5.5% and 10.4% to see if they meet our safe dividend and principal intact standards.

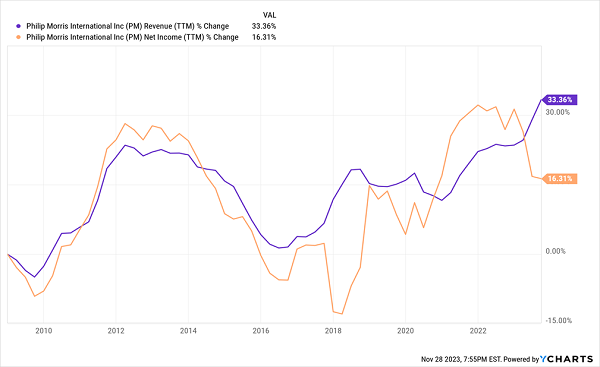

Tobacco companies like Philip Morris International (PM, 5.5% yield), somehow, keep churning cash flow. Governments hate ‘em, but smokers gotta have ‘em. And ol’ Flip Mo actually grows faster than our average tobacco peddler.

Shares have been left behind over the past year or so as the market has found its groove. But PM has performed exceptionally during downturns as a store of safety. And that’s in part because Philip Morris keeps finding ways to bring in more money.

Believe It or Not, Philip Morris is Still Growing

While cigarette sales are struggling, PM is finding ways to offset that weakness—specifically in heated and oral tobacco products, which it has bolstered by raising its stake in (and eventually outright acquiring) Swedish Match. Also, its positioning in foreign markets makes Philip Morris more attractive than its U.S.-locked peers. So while other cigarette makers might be treading water or worse, PM is expected to grow its top and bottom lines this year and next.

Philip Morris’s shares boast one- and five-year betas of 0.68 and 0.8, respectively. Dividend stability is every bit as nice—the company has increased its dividend every year since splitting from Altria (MO) in 2008, by more than 7% annually.

LTC Properties (LTC, 7.0% yield) is a national real estate investment trust (REIT) that’s roughly 50/50 split between senior housing and skilled nursing properties. This type of real estate was long considered can’t-miss—that is, of course, until COVID wreaked havoc on the sector. The upside? Most operators (including LTC) likely have the worst of it in the rear-view, with occupancy and rent coverage generally on the upswing.

LTC’s one- and five-year betas are both just under 1, so you’re not getting noticeably calmer performance than the rest of the market. But that could very well mellow out as the industry’s conditions continue to improve. The dividend needs to get in gear, though—LTC’s 7% yield is nice, and a monthly payout schedule is even nicer, but the payout has been idling for years at 19 cents, losing a lot of ground to inflation.

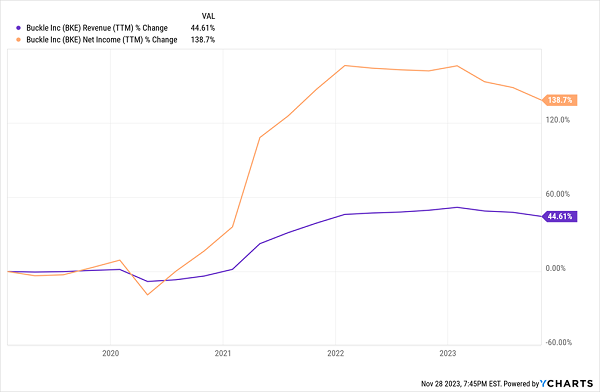

Fashion retailer Buckle (BKE, 10.4% yield) is a strange name to see here, on two counts.

For one, it’s generally surprising to see a retailer with consistently low beta—fashion is fickle, and as a result, fashion stocks tend to be mercurial as well.

But Buckle’s five-year beta is a hair under 1.0, and it’s been downright sleepy over the past year with a beta of 0.59. This is a case where beta doesn’t tell the whole story, though. After a few years of boom times, Wall Street sees Buckle’s earnings dropping 17% and revenues falling 6% this year; its results through three quarters are right in line with those projections. No wonder BKE shares are off double digits in 2023 while the S&P 500 has returned nearly 20%.

Buckle’s Financial Results Were Flattening; Now They’re Falling

If there’s any silver lining, it’s that Buckle’s results are largely expected to stabilize next year.

The other oddity is Buckle’s double-digit yield, which is extremely unusual for any stock, but especially one in retail. But BKE’s payout is more than meets the eye, for better or worse. Buckle is a special dividend payer—one that prefers to augment its regular dividend with special distributions as profits allow. Of the Buckle’s 10.4% yield, only 3.6% of that comes from its quarterly dole. So while Buckle does provide income potential, it’s perhaps not the best source of stable income potential. Let’s move on.

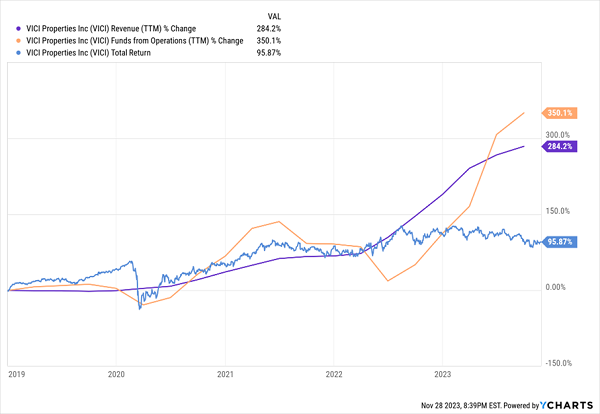

VICI Properties (VICI, 5.7% yield) is another eyebrow-raiser, as it’s involved in one of the market’s more cyclical businesses: casinos and hospitality.

VICI Properties’ portfolio includes 54 gaming facilities—including Caesars Palace Las Vegas, MGM Grand, and the Venetian Resort Las Vegas—as well as 38 non-gaming experiential properties. All told, its real estate includes 60,000-plus rooms and 500-plus restaurants, bars, clubs, and sportsbooks. So VICI Properties’ properties are a little more than just a place to sit down and play slots.

All of the above is discretionary nonetheless, but, then, VICI’s business isn’t collecting chips—it’s merely collecting the rent. And that’s really it, in fact. VICI is a triple-net lease property, so its tenants are responsible for taxes, insurance and maintenance.

From that perspective, business is good. In fact, so good that, despite a lukewarm forward-looking price-to-adjusted funds from operations (AFFO) of 14 or so, it’s possible the market is sleeping on this REIT.

VICI’s Operations Have Exploded, But Shares Haven’t—Yet

VICI just barely qualifies as low-vol—its one- and five-year betas are both just under 1. Still, that’s about as cool and collected as you’ll get from the gaming business, and it offers a 6% yield to boot—on a dividend that has been rising since its 2018 IPO.

One REIT that screams stability is Getty Realty (GTY, 6.2% yield), which is one of the most boring landlords in America.

And boring, as I like to say, is beautiful.

Getty Boasts a History of Stable Growth

Getty Realty owns nearly 1,100 single-tenant retail properties in 40 states and the District of Columbia. Sure, the mention of brick-and-mortar retail doesn’t exactly inspire confidence, but Getty’s tenants will. More than two-thirds of the portfolio involves convenience store companies like 7-Eleven and gas stations from the likes of BP (BP). Its other tenants include car washes, repair shops, auto service stations, and more.

Much of the above is either recession-proof or at least recession-resistant. That said, Getty isn’t exactly invincible—higher interest rates have weighed on GTY, much like other REITs. And there’s an open question about whether a gradual shift to electric vehicles will weigh on its gas-station properties, though the convenience-store aspect of these locations should make them plenty resilient.

Getty will never be a font of explosive growth. But it’s a smooth operator—one- and five-year betas are 0.67 and 0.91, respectively—and it boasts a well-above-average yield that keeps getting bigger as time marches on.

Give Me 4 Minutes, I’ll 5X Your Retirement Income

Getty is a perfect illustration of how we want to build a high-yield retirement portfolio. We want holdings that will let us sleep through existential crises—bear markets, economic slumps, yet another Jerome Powell press conference.

And those are exactly the kind of investments I stash away in my “Perfect Income” portfolio.

My “Perfect Income” portfolio attacks retirement investing from a different angle. Rather than trying to time the market and chase trends, we target high-yield holdings (roughly 5x the S&P!) that walk their own path, no matter what the Fed, Congress or the rest of the world throws their way.

So, what makes these dividends “perfect”? Well, they have to have a few things in common:

- They DO pay consistently, predictably and reliably.

- They DO survive—and even thrive—in market crashes.

- They DO deliver double-digit returns, with safe, secure investments.

- They DO require minimal management time—just a few minutes every month!

- They DON’T involve day trading, buying on margin or any other risky strategy.

- They DON’T involve gambling on penny stocks, Bitcoin or buying puts and calls.

Let me show you the stocks and funds you need to stabilize your retirement. But more importantly, let me teach you more about this incredible strategy itself and make you a better investor in the process!

Take control of your financial legacy today. Click here for my newly updated briefing on the Perfect Income Portfolio!