Interest rates are trending lower, which means real estate investment trusts (REITs) are rallying. These “bond proxies” tend to move alongside bonds and opposite rates.

If you believe the economy is likely to continue slowing, then select REITs are intriguing income plays here. Especially those yielding between 7.2% and 13.2%, which we’ll discuss shortly.

As I’ve been saying for a few weeks, the real story is in longer rates, namely the 10-year Treasury. I spelled this out in a recent article.

To recap, Treasury Secretary Scott Bessent has been upfront that he and President Trump are focused on the 10-year Treasury rate (the “long” end of the yield curve), and not the Fed benchmark (the “short” end).

That’s generally a boon for bonds and bond proxies (like preferred stocks, as well as certain equity sectors such as utilities). Naturally, lower 10-year yields will make REITs’ generous yields even more attractive, too, but in general, REITs have thrived much more often than not during periods of falling Treasury rates.

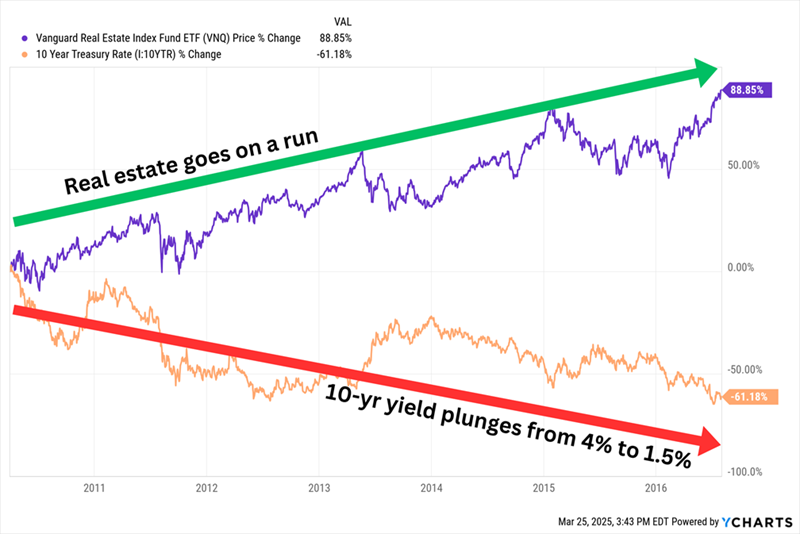

For example, let’s consider the 2010 to 2016 period in which the 10-year Treasury eased lower and lower:

REITs Rallied From 2010 to 2016

Of course we’re not looking to buy a pedestrian ETF. We are here for the dividends, the bigger the better! Our mandate is income so let’s review five REITs paying up to 13.2%.

Rayonier (RYN)

Dividend Yield: 10.6%

This first name rarely shows up on lists of high-yield REITs, and for good reason! Its yield is artificially inflated right now.

Florida-based Rayonier (RYN) is a specialty REIT that boasts a little more than 2.5 million acres of timber-growing land across the U.S. South, U.S. Pacific Northwest and New Zealand. That land is used in forestry products such as paper, sure, but also a lot more: hunting, recreation, beekeeping, mineral exploration, and in some cases, even community development.

Some of those acres are going away. The company in March announced it would sell its entire 77% interest in a New Zealand joint venture for $710 million. That JV accounts for 70% of its total NZ acreage and all of its productive acreage.

This is just the latest sale in a massive “right-sizing” at Rayonier, started in 2023, meant to streamline operations and financial reporting, improve resource allocation and, in the case of the NZ disposition, reduce exposure to log export markets and focus on its lucrative U.S. acreage. Rayonier originally targeted $1 billion in asset sales, but once the NZ transaction closes, its total dispositions will be closer to $1.5 billion.

Why am I focusing on all this M&A? Well, for one, RYN is making itself more attractive operationally while also raising funds to reduce its leverage.

But it also speaks to Rayonier’s payout potential.

Rayonier pays a merely so-so regular dividend that yields 4%. But in January 2025, the company paid out a massive special dividend of $1.80 per share (+6.6% in additional yield)—after making $495 million in dispositions during the fourth quarter. That follows a smaller 20-cent special dividend in January 2024 in the wake of a smaller timberland sale.

In other words, it’s possible that another big windfall might be on the way for shareholders after its $710 million New Zealand asset dump.

Longer-term, a healthier operational base and a healthier balance sheet could free Rayonier up to improve its regular distribution. The chart shows that the regular dividend is declining by 5% for the March payment, but it’s not really a cut—RYN paid out 25% of its special dividend in cash, and 75% in new shares, so the lower payment is just an adjustment to account for 7 million-plus new shares issued.

Could We See 3 Special Dividends in 2 Years?

Armada Hoffler Properties (AHH)

Dividend Yield: 7.2%

Armada Hoffler Properties (AHH) is a diversified REIT with 71 buildings. It gets the majority of its annualized base rent (ABR) from mixed-use office buildings (57%), with another quarter coming from mixed-use multifamily and the rest from mixed-use retail.

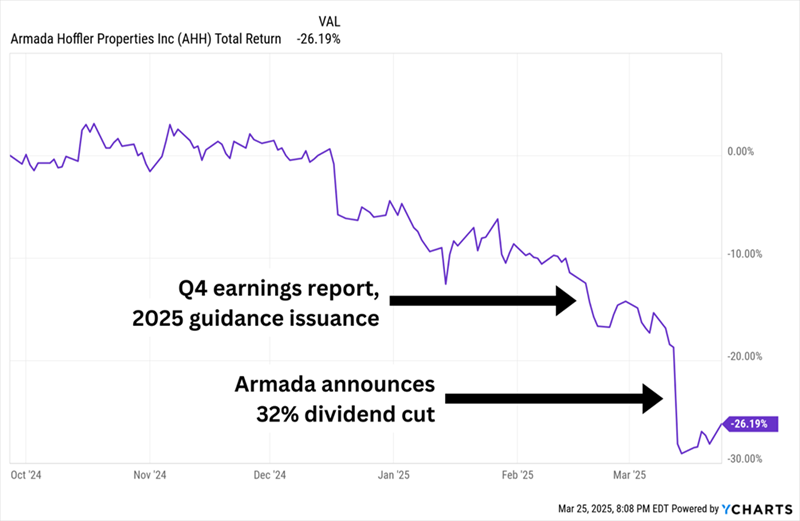

The last time I looked at Armada, in September 2024, it was yielding just a hair under 7%. Since then, the yield has ticked up to 7.2%. Unfortunately this is a case of a double dividend raise the “wrong way”—via a falling share price that sniffed out a payout cut!

Falling Price Sniffs Out Lower Payout

Armada looked like one of many real estate COVID bounceback stories. Occupancy was in the mid-90s. Same-store cash net operating income (NOI) was improving. It had recouped its dividend to near pre-COVID levels. Dividend coverage from adjusted funds from operations (AFFO) was a little tight but not sending out warning flares yet.

Still, I said AHH wasn’t yet an ideal situation.

In February, Armada delivered lousy guidance for 2025, expecting normalized FFO to decline anywhere between 15% and 22%. And in March, the company hacked its quarterly dividend by 32%, to 14 cents per share.

Armada had been working to improve its balance sheet, including reducing its exposure to variable-rate debt, and its guidance implied double-digit savings on general and administrative expenses. But tight coverage clearly was going to become undercoverage, so Armada pulled the trigger, with management noting the dividend would now be fully covered by “property income without any consideration of fee income.”

It’s possible AHH represents a healthier 7% yield today than it was last year, and because shares have fallen off a cliff, they trade at a cheaper 10 times starkly reduced AFFO estimates. But it’s a nonstarter without seeing more operational improvement first.

Brandywine Realty Trust (BDN)

Dividend Yield: 13.2%

Brandywine Realty Trust (BDN) is another hybrid REIT with a heavy office bent, but large (and increasing) focus on residential and life sciences buildings. It’s also very acutely focused, with its 64 properties located in either greater Philadelphia or Austin, Texas.

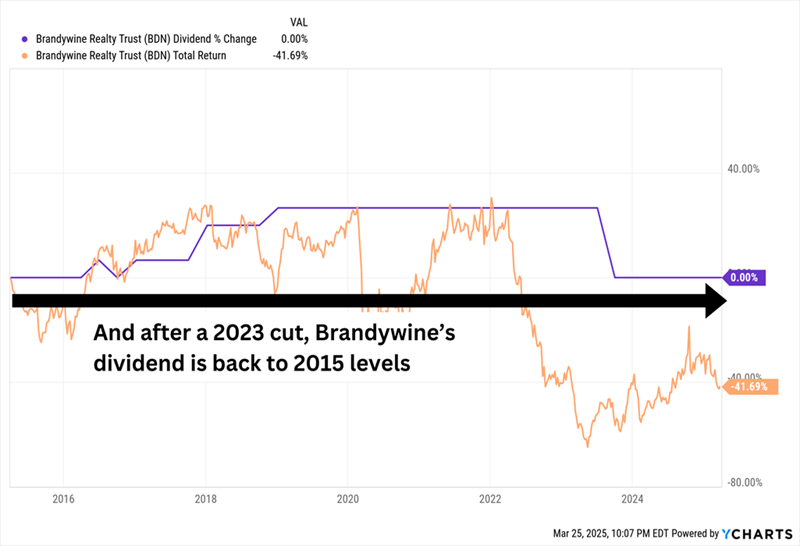

I looked at Brandywine just a few months ago, when it was trading at just 6 times FFO estimates. It’s trading at 7x now—but not because shares have improved. The company delivered a shoddy fourth-quarter report and disappointing guidance for 2025, and that has sent the stock back to the mat in 2025.

Brandywine’s wholly owned portfolio is performing decently. The problem is with its joint ventures. BDN is experiencing a heavy drag from its development projects. Some of its construction has been funded by expensive capital, and its arrangements with partners require Brandywine to recognize full interest and other costs until the projects become profitable. Estimates for JV FFO are tumbling as a result, and investors are responding by unloading shares.

Despite a massive 13% yield, we don’t want what they’re selling.

BDN’s Dividend Hasn’t Gone Anywhere. Its Stock Price Is Jealous.

Easterly Government Properties (DEA)

Dividend Yield: 10.1%

Federal government housing, anyone?

Didn’t think so.

Easterly Government Properties (DEA) is an office REIT on the exact wrong side of DOGE. This REIT owns 100 properties that it leases out to U.S. government agencies such as Veterans Affairs, the FBI, and the Drug Enforcement Administration, among others. And its buildings go beyond offices, spanning outpatient facilities, warehouses, courthouses, labs, even built-to-purpose properties.

DOGE, however—which wants to boot federal employees by the tens of thousands and reduce real estate footprint—is problematic for DEA. Alas, there are a couple of hopeful points for longs.

For one, Easterly has offices in more than two dozen states, but it doesn’t own any property in Washington, D.C., where Elon Musk appears to be concentrating his focus for now.

But more importantly (and more of a complication): Much as it might want to, DOGE can’t just rip up real estate contracts. Instead, many real estate contracts the government does want to get rid of will likely just have to run their course—and in some cases, they might have a change of heart by then.

“Every year we give ideas to the U.S. government on how to improve a facility,” CEO Darrell Crate told Institutional Investor. “With DOGE, people all of a sudden are receptive to ideas.”

While Easterly might defy the odds and not die by DOGE’s sword, this is a company that already had a longstanding problem consistently growing FFO. Hard pass on this double-digit divvie.

Gladstone Commercial (GOOD)

Dividend Yield: 8.1%

Gladstone Commercial (GOOD) isn’t a spectacular prospect right this second. Acquisitions are few and far between, and growth has flatlined, with few immediate catalysts on deck.

But it might just be building itself into a potential long-term winner.

If “Gladstone” sounds familiar, that’s because GOOD is part of the Gladstone family of REITs and business development companies (BDCs), which also includes Gladstone Land (LAND) and Gladstone Investment (GAIN) and Gladstone Capital (GLAD).

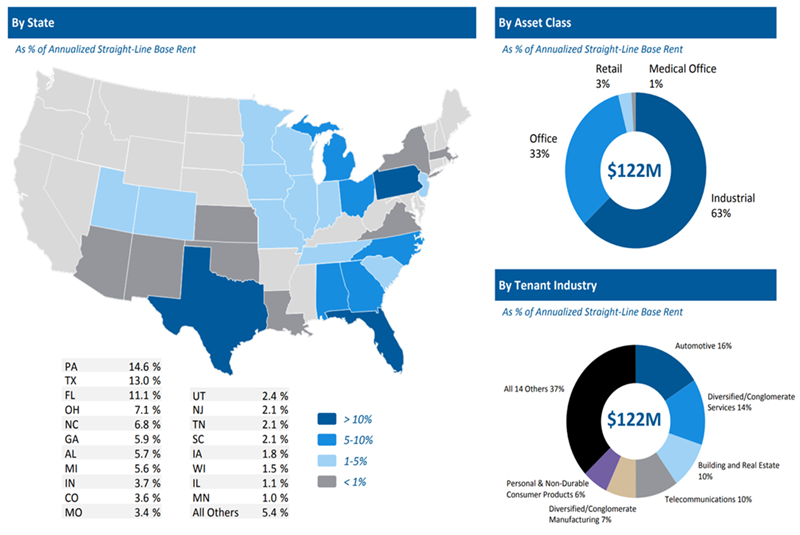

Gladstone Commercial owns 135 single-tenant and anchored multi-tenant net-leased properties, leased out to 106 tenants across 27 states.

The biggest strike against Gladstone has long been its office properties. Weakness in offices forced GOOD to reduce its payout by 20% in 2023, and even today, office occupancy of 94.3% pales compared to its industrial occupancy of 99.4%.

Fortunately, Gladstone has been reducing that office exposure, which is now down to 33% of annualized straight-line base rent. Most of the rest is industrial, though it does own a little bit of retail and medical office real estate. I’d like to see it pare down even more of its office portfolio, but GOOD is being constrained by a weak market for sellers.

An Increasingly Diversified Portfolio: That’s GOOD!

In the meantime, Gladstone has been reducing leverage and producing results that have largely been in line with expectations.

How to Collect a $48,000 “Portfolio Paycheck” When You Retire

We could wait around and collect an 8% monthly dividend. But a dip in shares would be nice: GOOD shares have actually outpaced the real estate sector over the past year, and they now trade for a fair 13 times AFFO estimates.

But if you’re ready to put your money to work right away, you can still collect 8%-plus monthly dividends, from names with even stronger growth profiles than Gladstone.

I’ve loaded up on dynamite high-yield dividends in my “8%+ Monthly Payer Portfolio”—a “who’s who” of companies and funds that check off the “3 H’s”:

- High yields

- High quality

- High durability

A lot of dividend portfolios try to offer up names that you know, and that you’re comfortable with. But Wall Street’s over-trodden blue chips tend to deliver relatively modest yields at high valuations … not to mention, they always pay quarterly.

My 8%+ Monthly Payer Portfolio is filled with names that many investors have (wrongly) slept on—despite kicking out 8%+ dividends that roll our way each and every month.

That dividend schedule means when you’re done collecting a regular workplace paycheck, you can quickly transition to collecting a regular “portfolio paycheck” of roughly $48,000 annually on just $600,000 invested—and that paycheck will still sync up with your monthly bills!

Don’t miss out on these terrific income plays while you can still get in at a bargain. Click here for all the details, and to download a FREE Special Report revealing the names and tickers of my favorite monthly payers.