Thank you to our 1,581 Contrarian Income Report subscribers who attended our webcast last week! My publisher described it as a “firehose of information”—hopefully, that was a good thing!

We have you, our thoughtful reader and income investor, to thank for the inspiration behind the firehose. We fielded 45 questions before the event and another 127 on the call, for a total of 172. Amazing.

As promised, I have read each and every question (as has our excellent customer service team). In the weeks ahead, we’ll discuss as many as I can find white space for. Let’s start with six today.

Q: I just subscribed to your Contrarian Income Report. Your most recent issue preaches patience. So, am I supposed to do nothing?

When investing, there is a time to be greedy and a time to be cautious. Right now, it’s best to play it a bit safe.

Our Best Buy list for the month of December was a bit thinner than usual (only five, versus our usual seven). The lack of more ideas on this list reflects my current caution.

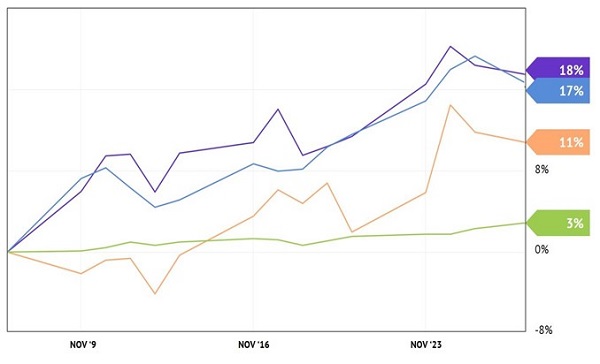

Just one month ago, there were more nervous nelly investors out there. That was the time to be aggressive. And congrats to our readers who did, because our top four best buys from November’s CIR averaged 12% returns in one month!

November’s Top 4 “Best Buys” Averaged 12% Returns—In 1 Month!

However, if your focus is long-term, you have two choices on what to buy for December:

- Nothing at all (and wait for my January instructions).

- Or, simply maintain your usual investment allocation.

You are probably doing number two right now, setting aside a set amount of cash every month. This type of dollar-cost averaging is always a fine plan. By investing regularly, you’ll naturally bank more shares when prices are low, and less when they are high.

Q: What convertible bond funds do you like?

Right now I wouldn’t put any new money into convertible bond funds. It’s best to wait for a pullback, because these funds do trade up and down with the broader stock market. And with sentiment quite cheery, we do need some type of correction to blow off this bullish steam.

If you’re a Dividend Swing Trader subscriber, you’re sitting on gains of 18% and 21% from our two convertible positions in just a few months! Continue to hold these funds and wait for my cue to book profits, which could be coming as soon as tomorrow.

For those not familiar with convertibles in general, these income vehicles pay regular interest. In this way, they act like bonds. You buy them and “lock in” regular coupon payments.

But convertibles are also like stock options in that they can be “converted” from a bond to a share of stock by the holder. So, you can think of them as bonds with some stock-like upside.

The SPDR Barclays Capital Convertible Bond ETF (CWB) is the most popular mainstream (read: widely marketed) vehicle to purchase convertibles. It pays just 0.8% today. As you know, when we buy ETFs, we lock in:

- No discount to NAV (net asset value), and

- A low yield.

(Snooze.) While CWB should do well-enough as long as the current money printer-driven rally continues, a better bet is a closed-end fund (CEF) like the Calamos Convertible and High Income Fund (CHY).

CHY has been a great fund. Over the last decade, it’s returned a stellar 9.9% per year on its NAV.

DST subscribers are up 18% on CHY in four months. Continue to hold, and I’ll let you know when it’s time to book profits (and potentially buy back later).

Q: Any thoughts on emerging markets? Is it worth investing?

As I write, the US “M2” money supply is up an amazing (and scary) 24% year-over-year. When the Fed swung into action in March, the dollar began to break down right away. Seven months later, the greenback continues to sink and, by historical standards, we are probably closer to the start of the dollar’s bear move than the end. And these tend to be multi-year trends.

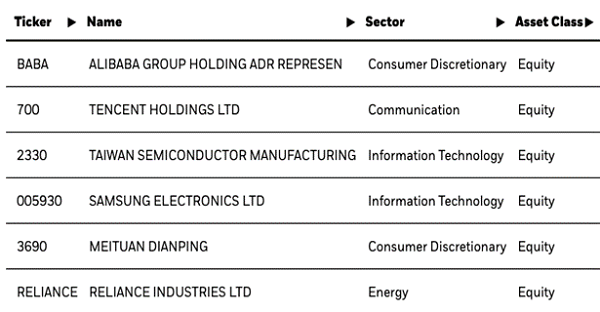

The iShares MSCI Emerging Markets ETF (EEM) usually gets a boost from the weak dollar. It’s a nice way to diversify our holdings and take advantage of strength in emerging market stocks without getting too deep “in the weeds” trying to figure out how to buy this alphabet soup of holdings:

EEM Holdings: Easier to Buy the ETF

EEM actually owns 1,236 positions. It’s a one-click way to play these two trends.

With a 2.5% yield, EEM won’t qualify for our CIR portfolio. But DST’ers are up a quick 10% on our EEM trade (purchased on October 15). As with the convertibles, this position is a Hold for now.

EEM isn’t really a “buy and hold forever” position, but it is a fine ETF to trade, if you’re able to time your entries and exits. We plan to sell it high soon and buy it back for less down the road.

Q: Any infrastructure plays for 2021?

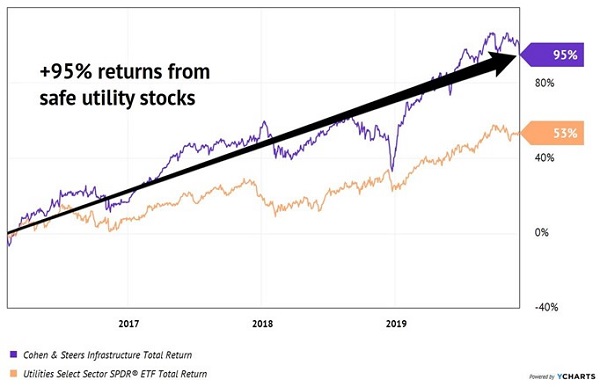

Our Cohen & Steers Infrastructure Fund (UTF) is a great high-paying way to play infrastructure. UTF invests in “cash cow” infrastructure companies that own and operate utilities, airports, toll roads, railroads, and other physical framework.

Longtime CIR subscribers will remember the name fondly. The first time we bought and held this excellent fund, we enjoyed 95% total returns,and many of the gains were delivered to us in the form of UTF’s neat monthly payout!

We often discuss how well-run CEFs often beat the pants off of pedestrian ETFs, and that’s exactly what UTF did to household utility ETF XLU:

Our Utility CEF Crushed its ETF “Competitor”

Since we re-added UTF to our CIR portfolio, its price has rallied and the fund now trades at a premium to NAV. This is a great long-term holding, but there’s no reason for us to chase it. Let’s sit back, be patient and wait for a pullback to purchase more shares.

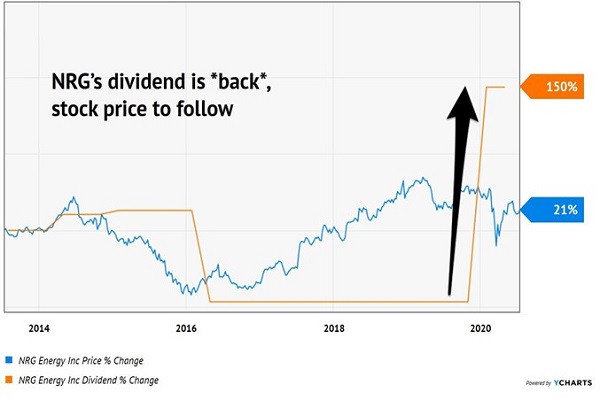

Q: What do you think about NRG?

When stocks-in-general are hot, safe dividends often become uncool. As a result, a stock like NRG Energy (NRG) dropped into the bargain bin.

The firm paid its $0.30 per share quarterly dividend, which marks an impressive 10-fold increase over its dividend in the second quarter of 2019!

An Underappreciated Turnaround Story

You may have winced at my initial mention of NRG and maybe weren’t sure why. The company slashed its dividend in 2016 as part of a corporate restructuring. The old NRG was heavily dependent on prices for coal and natural gas, and its cash flows were crushed when those commodities crashed in 2015 and 2016.

Give management credit for a successful turnaround. They found hundreds of millions of dollars in cost savings and removed billions in debt from their balance sheet. Their previous dividend cut was a “necessary evil” to achieve these goals. Debt is now down to a manageable 2.5 to 2.75X EBITDA, and the dividend is back.

In addition to the pay raise, the firm plans to buy back $380 million in shares and achieve an investment grade credit rating (which will further lower its cost of debt). Shares now pay $1.20 per year, and management is projecting 7% to 9% annual dividend growth in the years ahead.

As the broader markets continue to return to reality, and day-to-day case count and lockdown drama continues, a stock like NRG is going to be increasingly appealing because its drama is already in the rearview mirror.

NRG yields 3.6% today and it’s on track to be one of the few companies raising its dividend in January 2021. There’s plenty to like about NRG and several reasons for its stock price to appreciate as more income investors understand its successful turnaround effort. This is why it’s a current holding in our Dividend Swing Trader portfolio.

Q: What are your favorite recession-proof dividend plays for 2021?

There’s an untapped portion of the market that most income investors don’t know about. It has the ability to return 15% per year, every year, regardless of whether it’s a bull or bear market.

Their secret lies in these “three pillars” of dividend success:

- Consistent dividend hikes,

- A “lagging” stock price, and

- Share repurchases.

Together, these three pillars let us identify stocks that are undervalued, overlooked, recession-proof and primed for 15% growth year after year. Click here and I’ll share my seven favorite dividend growth ideas for 2021.