Worried about the next round of tariffs? Tech disruption from DeepSeek? The geopolitical landscape?

All of the above?

Fret not my contrarian friend—here are seven wonderfully-sleepy dividend stocks. They yield between 5% and 14.1% and we are discussing them today because all seven boast low betas.

This means these shares move less than the overall market. An admirable quality when it comes to a dividend stock because we’re not here for the price drama, we’re here for the payout.

Beta represents an investment’s volatility against a benchmark. Stock beta is typically benchmarked against the S&P 500, aka “the market.” Beta is based around the number 1, so a stock with a beta equal to 1 moves with the market. If the S&P 500 is down 1%, we would expect this stock to be down one percent.

A beta above 1 is more volatile than the market. Think Bitcoin.

Our focus today is stocks with betas below one. If the S&P is down 1%, we expect these positions to be down 0.5% or 0.25% or so.

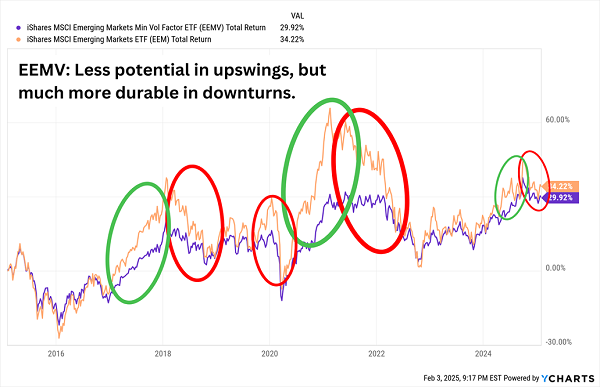

Betas are based on historical price movements and are not future guarantees. But directionally they can be helpful to know. We can reasonably expect low-beta stocks to deliver smaller swings in price action. We can easily see this dynamic at work when comparing a traditional emerging-market fund (very volatile) versus a minimum-volatility EM fund:

Lower Volatility Means a Much Smoother Ride

That said, beta is not the end of our research. We also consider the fundamentals driving the profits (and payouts) of tomorrow. Let’s get into these seven low betas, starting with our “lowest” yield of 5% and working our way all the way up to 14.1%. Let’s start with aisle five.

Consumer Staples

Baking specialist Flowers Foods (FLO, 5.0% yield), the company behind bread brands such as Nature’s Own, Dave’s Killer Bread, Wonder and Sunbeam, as well as snack brands including Tastykake and Mrs. Freshley’s.

FLO’s business is predictable. Revenues have been in a larger uptrend for years; same goes for profits, though legal settlements tied to employee classifications took a big chunk out of the bottom line in 2023. And that consistency has led to a longer-term (five-year) beta of just 0.37, or roughly only a third as volatile as the market, while its one-year beta of negative 0.11 reflects a truly slow-moving stock that hasn’t been aligned with the market. Given the year the broader market has had, that’s not great.

Flowers Marches to the Beat of Its Own Drum. But It’s a Lousy Beat.

We could excuse some of underperformance as investors keeping their assets away from stodgy defensive plays and chasing the market’s growth—FLO and the S&P 500 have been running almost inverse to each other for a couple of years now. But Flowers also has a problem with mismanaging expectations, and has produced mostly in-line or disappointing earnings reports during its current downtrend.

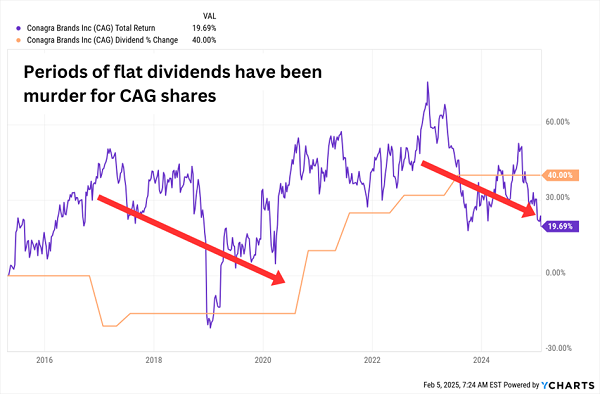

ConAgra (CAG, 5.6% yield) has a similar volatility profile, with a low five-year beta of 0.27 and a slightly negative one-year beta. It’s befitting a staples stock—one with a wider business than Flowers, dealing with four different divisions: Grocery & Snacks, Refrigerated & Frozen, International, and Foodservice. As a result, it offers a more diverse product lineup that includes Birds Eye frozen vegetables, Marie Callender’s and Healthy Choice frozen meals, Duncan Hines baking mixes, Slim Jim meat sticks, Reddi-wip whipped cream and Angie’s Boomchickapop popcorn, among others.

The financial picture is much less promising here. Profits have dropped in each of the past three years, and 2024’s net income was only a bit more than a quarter of what it was in 2021. Worse, the top and bottom lines are pacing for another retreat in the current fiscal year. While the majority of its brands continue to hold or gain market share, expectations for increased inflation are holding back ConAgra, which guided down in December.

CAG shares have long exemplified the “Dividend Magnet,” for better or worse.

Unfortunately, after a few years of annual dividend raises, ConAgra has once again gone more than a year without hiking the payout—and it shows.

The Dividend Magnet Is on Low-Power Mode

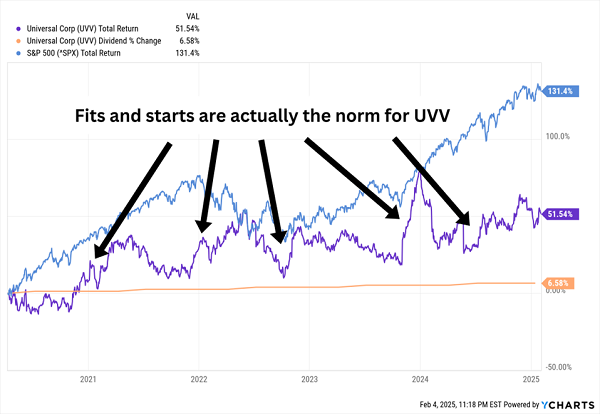

Universal Corp. (UVV) has always stood out to me because it’s a useful oddball in a niche dividend space. Specifically, it’s a “picks and shovels” play in tobacco. Traditional tobacco stocks are names like Philip Morris (PM) and Altria (MO) that produce cigarettes and other tobacco products. However, Universal Corp. doesn’t produce finished products—it merely supplies the tobacco.

Actually, it does much more—in addition to procuring and processing flue-cured, burley, dark air-cured, and oriental leaf tobacco, it also has an ingredients division (Universal Ingredients) and a “value-added agricultural business” (Universal Enterprises) that includes nicotine production, a lifecycle data solution and even a compost facility.

There’s a decided lack of volatility in corporate financials and the dividend, which are growing, albeit slowly. But one- and five-year betas of 0.14 and 0.78 actually reflect shares that refuse to mirror the S&P 500 more than they reflect serene stock movement.

Peaks and Valleys Are More Common Than You’d Expect

Unfortunately, for the moment, UVV is hands-off. The company hasn’t released a quarterly earnings report since August—in November, it received a notice from the New York Stock Exchange that it was not in compliance for failing to report its quarter numbers and has six months to file its 10-Q. This largely stems from an internal investigation over allegations of embezzlement at a Mozambique subsidiary. Universal doesn’t believe it will have a material negative impact for the fiscal year, but even if we were considering getting our feet wet, the most prudent move would be to wait until the company is back in compliance.

A Staples-Esque Consumer Play

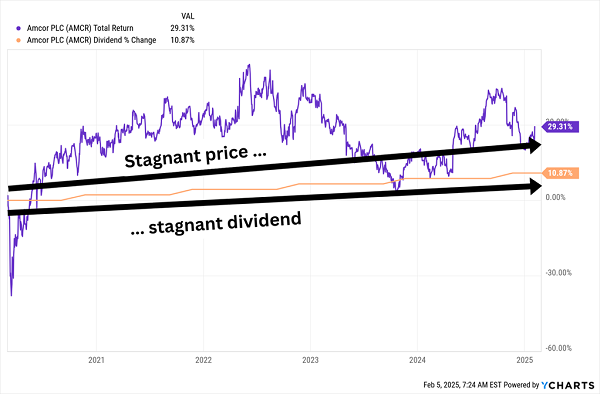

Amcor (AMCR) is a cyclical play that often feels like it’s defensive. This Switzerland-headquartered firm makes a variety of packaging—everything from shrink bags for food to blister packaging for pharmaceutical pills to sachets for cosmetic samples—for consumer and healthcare companies. So, yes, consumer demand still plays a big role in Amcor’s fortunes, but not as acutely as consumer cyclical companies that specialize in, say, just making snacks, or just making drinks.

Indeed, Amcor’s business line has enough financial stability that it boasts more than 40 years of consecutive dividend increases, putting it among the ranks of the Dividend Aristocrats—a title it picked up from the 2019 acquisition of Bemis.

The problem? Amcor has been largely treading water for years. So yes, volatility has been low—its one- and five-year betas sit at 0.27 and 0.85, respectively—but so have its prospects. Indeed, it was largely looking toward aggressive cost cuts to improve its bottom line.

Little Dividend Growth, Little Growth Growth

But Amcor might very well have found a potential catalyst through another acquisition. It’s currently in the process of trying to merge with U.S. packaging manufacturer Berry Global (BERY), which Amcor hopes will drive volume growth through greater scale in existing categories, as well as entering new categories and geographies—not to mention the potential for synergies.

Healthcare

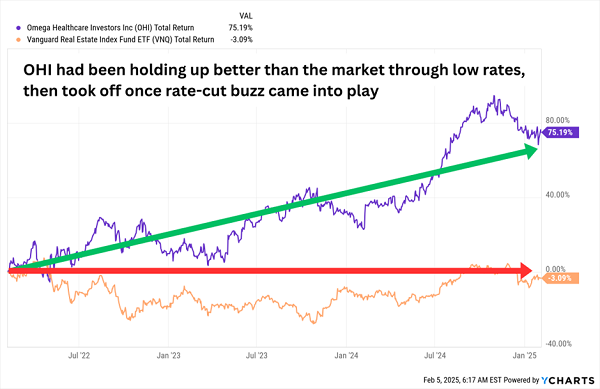

One of the highest-yielding low-beta stocks out there is Omega Healthcare Investors (OHI, 7.1% yield), which sits at the intersection of healthcare and real estate. Specifically, it provides financing and capital solutions to skilled nursing facility and assisted living facility partners, with a portfolio of 962 properties in 42 states and the U.K. that are leased out to 81 different operators.

Omega has turned around its fortunes over the past couple of years—a combination of an improved operational story and a much friendlier interest-rate environment.

OHI Stands Out in a Struggling Real Estate Sector

Its longer-term five-year beta isn’t all that low, at 0.97—roughly in line with the market. Its one-year beta is extremely low, at 0.20. Because while OHI has been jumpier than the real estate sector over the past year (as shown in the chart above), shares have been smooth compared to the rest of the market.

In theory, its positioning in long-term care at a time when demographics are increasingly in its favor, as well as OHI’s triple-net lease structures, should put the wind at Omega’s back. However, I mentioned a few months ago that OHI looked frothy, and since then, the stock has pulled back sharply amid a broader pullback in real estate. The valuation has improved, with shares now trading hands at 13-times next year’s FFO estimates. Reasonable though not quite a bargain.

“Flexible” Dividend Payers

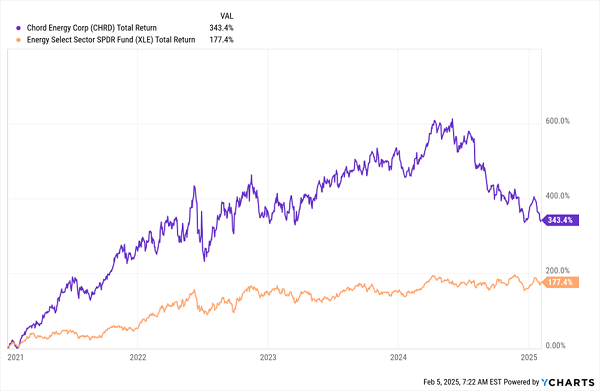

It’s not often that we see traditional energy operators throwing off very high yield and low beta. But independent oil-and-gas producer Chord Energy (CHRD, 9.1% yield), which operates in the Big Sky’s Williston Basin, is an exception, with a 9%-plus yield, as well as one- and five-year average betas of 0.74 and 0.84, respectively—though the former is a little misleading.

Chord’s Past Year: A Case of Low Beta, But Not Exactly Low Volatility

The bad news first: Chord has been downright rotten over the past year, with weak oil prices hacking share prices down by a little less than 40% since they peaked in June 2024. But CHRD had some froth to work off following a 615% total return since the start of 2021 that more than tripled the energy sector in that time. Even including the past few months’ losses, it’s still up by roughly double.

Still, Chord boasts a pristine balance sheet and generates strong free cash flow even amid lean oil prices. Moreover, it has one of the industry’s best free-cash-flow (FCF) payout programs, bolstered by its merger with Canadian E&P Enerplus. For at least the past few quarters, it has set return of capital (RoC) at 75% of FCF. That goes toward paying a base dividend of $1.25 per share (~4.5% yield); any additional free cash flow past that funds a variable dividend and/or share buybacks.

CHRD is tactical about these expenditures. For instance, in the second quarter, RoC was set at $197 million, and Chord bought back roughly $62 million in shares while paying out a $1.27/share variable dividend. But in Q3, during which shares really started to tumble, RoC was set at $234 million, which included $146 million in buybacks (and the authorization of a new $750 million repurchase program) but a smaller 19-cent variable distribution.

The downside? Yields can really fluctuate from year to year. But it’s hard to argue Chord doesn’t have shareholders’ best interests at heart.

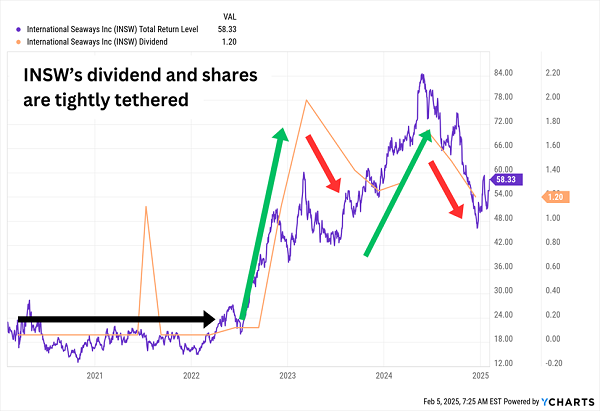

Low-beta dividends don’t get much bigger than International Seaways (INSW, 14.1% yield), which owns and operates a fleet of 83 ocean vessels that transport crude oil and petroleum products. Currently, its fleet includes 38 Medium Range (MR) tankers, 14 Long Range 1s (LR1s), 13 Suezmaxes, 13 Very Large Crude Carriers (VLCCs), and five Long Range 2s (LR2s).

International Seaways, like CHRD and OHI, is another example of how low beta can sometimes be deceiving. In INSW’s case, its five- and one-year betas are exceedingly low, at -0.11 and 0.14, respectively, but like many of its tanker brethren, this stock can really move.

More importantly, this stock is about as tethered to its dividend as it gets.

The Dividend Magnet’s Force Is Strong in This One

Of course, that’s because International Seaways’ dividend is even more variable than Chord. INSW features a 12-cent quarterly distribution representing just 1.2% worth of yield—thus, the vast majority of this double-digit dividend is heavily reliant on business conditions, which naturally also dictate the ups and downs of the stock itself.

It’s not ideal for retirement planners, but low beta and all, swing traders might be attracted to this mix of high potential upside and yield. Specifically, INSW boasts solid fundamentals, low capex and a low cash-flow breakeven, and if shipping rates rebound in 2025 as expected, that could be a potent combo.

This 11% Payer Is Another Top Buy as Volatility Ticks Up

If we’re trying to find both stability and double-digit yields for the longer term, we can do much better than INSW.

I’m talking about a massive 11%, in a fund diversified across numerous holdings, that pays us each and every month.

At an 11% yield, this expertly run closed-end fund (CEF) pays us …

- $11,000 in dividends on every $100K invested.

- $22,000 on every $200K.

- $500K? A sweet $55,000 in yearly dividends.

And with those payouts rolling in every month, the next one is always just a few short days or weeks away.

Which is why I’m urging all investors to buy this stout 11% payer now. It’s a rare bargain in a universe of overpriced US stocks and funds, and I don’t want you to miss your opportunity here.