This crisis has caused a lot of folks to develop a crippling fear when it comes to REITs: they see the beating mall owners like Simon Property Group (SPG) have taken and swear REITs off for good.

To be sure, SPG took it on the chin in March, and has not gotten up:

Simon’s Business Model: Broken for Good

But way too many people think REITs are about shopping malls, and that’s about it. It’s too bad, because this first-level thinking causes them to miss out on a lot of upside—and dividend growth, too.

Beyond the Mall

Members of my Hidden Yields service know better: we wanted nothing to do with mall landlords before this crisis, because Amazon.com (AMZN) was already relegating them to the history books. COVID-19 simply sped up the trip!

That makes SPG a classic value trap—it’s cheap for a reason: its business model is straight out of 1996.

Dumpster fires like this have unfairly cast a shadow over the hundreds of other REITs out there, like American Tower (AMT), which rents 139,000 cell towers to wireless providers around the globe, including Verizon (VZ), AT&T (T), T-Mobile US (TMUS) and Sprint (S).

American Tower is the exact opposite of Simon. It’s riding locked-in megatrends like the COVID-driven surge in technology use and the launch of hyper-fast 5G networks.

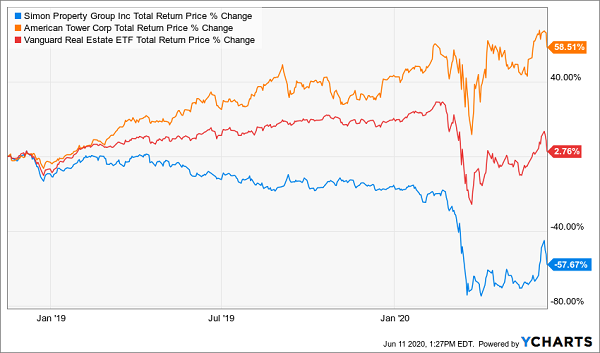

Compare the two REITs and you get a good illustration of the bipolar nature of REIT-land these days: AMT delivered a 59% return for my Hidden Yields since my November 2018 recommendation—21 times what you’d have gotten from the REIT benchmark Vanguard Real Estate ETF (VNQ).

SPG? It went the other way, losing 58% of its shareholders’ money!

The Bipolar REIT World in 1 Chart

AMT isn’t the only REIT you should consider as you build your shopping list. Let’s walk through some other REIT sectors—and individual tickers—to see which are ripe for buying (and selling) now.

Self-Storage REITs: Avoid This “No-Man’s Land”

Another corner of the REIT space that’s hit the mat hard is self-storage: all the major players—Public Storage (PSA), ExtraSpace Storage (EXR) and CubeSmart (CUBE)—lag the S&P 500 year to date.

Self-Storage Stocks Fall Behind

There were already worries about overbuilding in this sector prior to COVID-19. That’s a constant problem in a business where the barriers to entry are absurdly low: once you’ve built the building, you really just need to hand out keys and keep the dust off the shelves!

Now, with the recession, the time for extra “stuff” has passed. In the REIT landscape, self-storage REITs fall somewhere between malls and cell towers, and this is no time to be in no-man’s land.

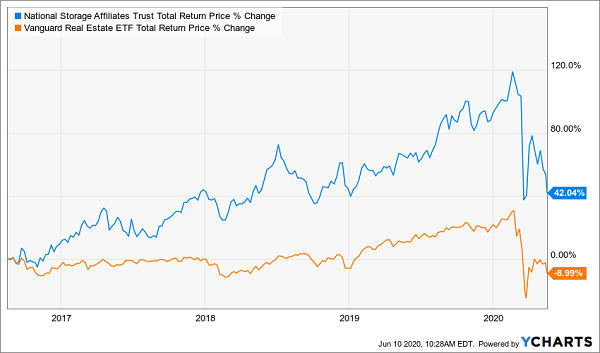

This is why we sold National Storage Affiliates (NSA) in the May Hidden Yields—but not before riding it to a 42% total return since my recommendation in August 2016 (with half of that gain in dividends), easily besting VNQ.

NSA Buy Pays Off

Now let’s move on to two other sectors (and two specific REITs) that are nicely dialed into the new world we find ourselves in.

Data Center REITs: Prime Pandemic Plays

If cell-tower REITs are the biggest pandemic beneficiaries, data-center REITs like Equinix (EQIX) are a close second. The company houses the servers companies need to keep running; it’s a pioneer in the space, founded in 1998.

Name a trend and Equnix is in the thick of it. Work from home? Check. Surging e-commerce? Check. More meetings held through Zoom (ZM)? Check. Internet of things? Check. Cloud computing? Check.

Equinix stands out for its steady, no-drama gains: it’s crushed the S&P 500 in year to date and has done so with a lot less volatility:

A Portrait of Calm in a Rough Year

That low volatility is an Equinix trademark: it boasts a five-year beta rating of 0.43, meaning its 57% less volatile than the market as a whole.

I expect those steady gains to continue—and accelerate.

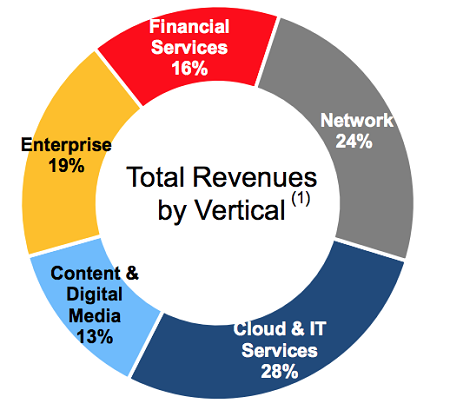

First off, the REIT boasts 210 data centers across 55 cities and five continents, so it’s nicely diversified geographically. And as you can see below, it has clients in a wide—and evenly spread—range of sectors:

A Diversified IT Provider

Source: Equinix Q1 investor presentation

Equinix’s clients also sign on via long leases, and those have a long time to run (18 years, on average, if all extensions are enacted).

Dividend growth will also drive price upside: Equinix yields just 1.9% now, but it’s goosed the payout 57% since it started paying dividends five years ago. If you’d bought back then, you’d have more than doubled the yield on your original buy.

I expect folks who buy today to be able to say the same in 2025, for a couple of reasons. First, Equinix’s payout ratio is safe, with the dividend accounting for just 47% of its last 12 months of FFO (funds from operations, the best measure of a REIT’s cash flow), so it can easily afford more hikes. Management also sees FFO growing 4% to 8% this year, fueling more dividend growth—and price upside, too.

Warehouse REITs Are Another Good Pandemic Play—But Be Choosy

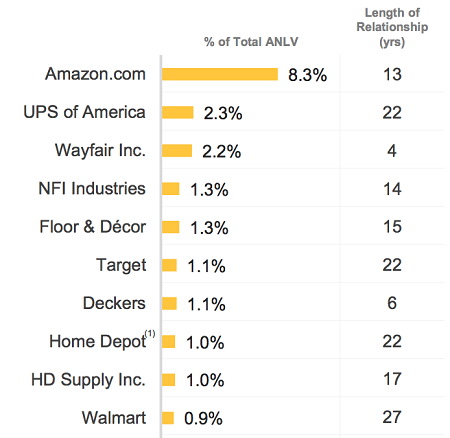

Finally, let’s talk about warehouse REITs, which are great plays on surging online shopping. The standout here? Duke Realty (DRE), whose top-10 tenant list reads like a who’s who of e-commerce.

DRE: A “Pick and Shovel” E-Commerce Play

Source: Duke Realty NAREIT REITweek 2020 conference presentation

As you can see, the poster child for e-commerce, Amazon.com (AMZN), is Duke’s top client, and other retailers that are either solely online or have robust online operations, such as Walmart (WMT), Target (TGT) and Home Depot (HD), are also onboard. United Parcel Service (UPS), another obvious e-commerce beneficiary, is nicely placed in the No. 2 spot.

That’s why, unlike mall REITs, Duke hasn’t lost many rent checks in this crisis: it collected 95.4% of its rent in May, with 3.5% deferred. What’s more, total deferrals are inconsequential at just 1% of yearly revenue.

What’s more, the company has only $3.4 million of debt maturing this year, which is easily covered by its $188 million of cash on hand.

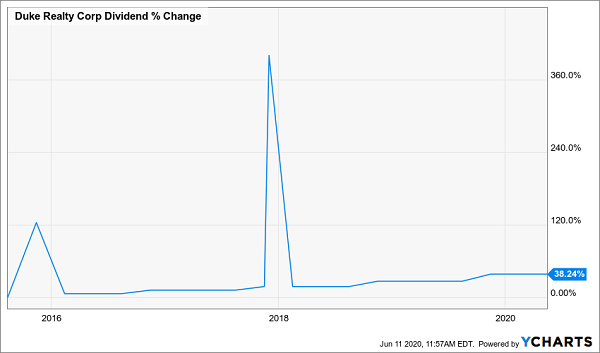

That brings me to the dividend, which yields 2.6% today but has jumped 38% in the last five years. Duke also pumps out special dividends on the regular:

Duke’s Rising Dividend

Is the payout safe? You bet. In the last 12 months, Duke paid 63% of core FFO as dividends. That’s ultra-conservative in REIT-land, where sustainable ratios of 85% and more are common.

An Urgent “7-Buy Alert” for 15%+ Yearly Gains (for Life)

Duke and Equinix should be on any dividend investor’s short list now, because it’s tough to imagine two other companies better suited to this pandemic.

But they’re just the start: we can do even better with a basket of 7 overlooked stocks that are not just surviving this whipsawing market—they’re poised to thrive.

My Hidden Yields team and I have carefully assembled them into a “recession-resistant” portfolio we’ve designed to hand you steady 15%+ gains, year in and year out, even if markets take (another) header.

Add these 7 sturdy picks to your portfolio now and you can look forward to steady dividend hikes—and price upside—to lead you through this crisis (and beyond!). Don’t miss out. Get full details on all 7 of these “recession-proof” stocks (and a no-risk trial to Hidden Yields) right here.