I sure started a stir last week when I mentioned the other “I” word. Our usual beat here is income, but last week we discussed inflation and what it means for our dividend-paying bonds and stocks.

We received quite the response. A big hat tip to our excellent customer service team for fielding your questions!

I owe you a bit more detail, so let’s get into our financial FAQs this week. And while we’re at it, let me stir the pot a bit more by dropping the other “D” word, deflation.

We’re not getting theoretical for the sake of it. The lens through which we make our income investing decisions depends on whether or not we have deflation (think March), inflation (think April through last week) or some “Goldilocks” ideal mix (à la 2009 to 2020).

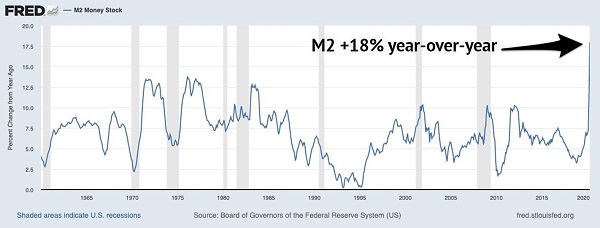

How much money has the Fed “printed” again?

Fed chair Jay Powell pulled the lever on the money printing quantitative easing machine early and often in March. In doing so, all previous records were smashed in the largest money creation event of all-time (as defined by M2, the measure of the amount of money “out there” in circulation):

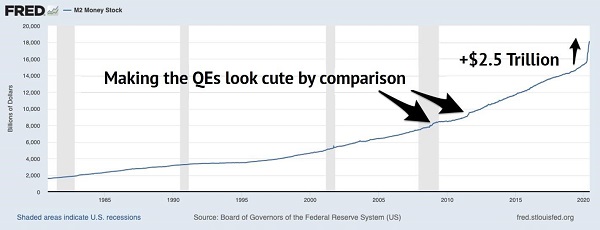

The Biggest Money Bump… Ever

A cool $2.5+ trillion and counting has been dropped into our collective accounts since March. To put this in perspective, the IRS collects about $3.4 trillion in taxes every year. We printed nearly an entire year’s worth of tax revenues.

“Now That’s How You QE!” – Chairman JP

The Atlantic’s Derek Thompson reports that, thanks to stimulus checks and higher unemployment insurance, personal income in the US actually soared by 10% in April.

So… do I need to sell my fixed-rate bonds (and CEFs that own them) right now?

Not yet. Personal income is going to plummet when our current stimulus runs out. Plus, consumers are saving and not spending. Until a true economic recovery takes hold, and people begin spending once again, it is going to be challenging for any level of inflation to “stick.”

When you hear about the “velocity” of money, this is what pundits are talking about. Japan’s central bank has printed a ton of cash in recent decades, but it’s aging population isn’t spending their yen (they are saving it). The velocity of money in Japan is low—and inflation is tame—because the Japanese are sitting on their cash rather than spending, investing and speculating with it.

(Remember the Japanese asset bubble of the 1980s? Now that was velocity in action.)

So…this is a 2021 thing? 2022?

It’s hard to picture any sustained level of inflation, or reflation, until at least 2021. (When I say reflation I’m talking about what we saw in 2009: an asset boom that eventually resulted in a slow recovery and a Bitcoin and pot stock bubble, but not the type of runaway inflation we saw in the 1970s).

Bear markets tend to last 12 to 18 months. Our 2008 experience was roughly 18 months gate-to-gate. I realize it feels like 2020 has been dragging on forever but this is only the fourth month of the downturn (yikes).

Another 14 months from here puts us in reflation territory towards the end of 2021. Unless our Fed boy JP gets really reckless between now and then, we can probably set our alarms for the back half of 2021.

Sounds like our dividend portfolios are where we want them right now. Why’d you drop the other “D” word?

In between these bouts of money printing, we are going to see more days and perhaps weeks of deflation. Remember 2008 when every single ticker on your screen was red? It happened again in March for a few weeks and, hate to say it but it’s my job to, we’re going to see more days like last Thursday where anything and everything gets dumped.

Value investor Shelby Davis famously said: “You make most of your money in a bear market; you just don’t realize it at the time.”

In April, we bought some great dividend stocks that were way down. It felt nauseating at the time (most contrarian plays do!). That is usually a good sign, and sure enough, that was the time to step in.

Now, with investor sentiment (amazingly, astoundingly, I don’t understand why but it is) bullish of all things, it’s a prudent time to be cautious. We can use the moment to trim any positions that we wished we’d sold in February. And we should be glad that we kept some dry powder because we can deploy it in the weeks and months ahead when perfectly good dividend stocks get dumped once again.

What dividend-paying stocks should I have on my shopping list?

Dividend growers! This is the time to cherry-pick dividend stocks that are going to double. As Davis would say, we can make most of our money in the months ahead because we’re still in a bear market.

I outlined my basket of seven favorite “overlooked” recession-proof dividend growers in this emergency “dividends to buy right now” report. It’s yours with a free test drive of Hidden Yields. Click here and I’ll share the details, including the stock names, tickers and my ideal “buy below” prices.