Today we’re going to discuss the secret to double-digit annual returns every year, forever, with secure real estate investment trusts (REITs).

We income-seekers love REITs for a simple reason: high dividends! The typical REIT yields twice as much as the average S&P 500 stock. That’s mainly because these trusts receive reliable recurring revenue—they simply collect the checks that roll in every month, take out enough to maintain the buildings and then send the rest to us.

And some REIT dividends are true standouts in today’s low-yield world, like the 5.5% thrown off by warehouse landlord W.P. Carey (WPC).

WPC is a two-time winner in our Contrarian Income Report service’s portfolio, having returned a tidy 28% in dividends and gains in 12 months in its first tour and a steady 16% return in 14 months (and counting) in its second.

Recurring Revenue—a Killer Edge in Uncertain Times

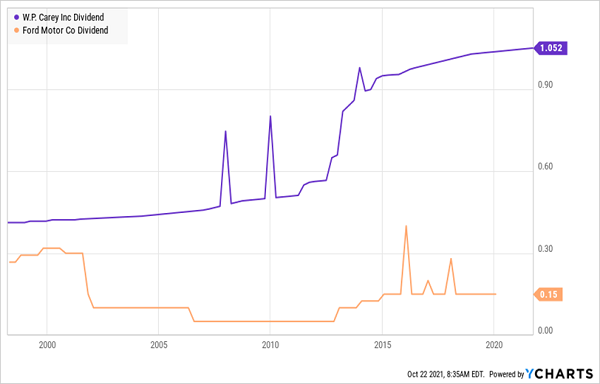

It’s tough to overstate the advantage REITs’ recurring revenue gives them (and us!): where firms like Ford Motor Company (F) have to start from scratch every quarter, keeping current customers happy while winning others over one by one from nimble competitors like Tesla (TSLA), our REITs sit back and pocket rent checks that roll in like clockwork, mostly from tenants who signed on years earlier.

It’s a proven model we can rely on. And that’s why WPC’s dividend has a lovely upward arc (with special dividends thrown in for good measure), while Ford’s volatile sales translate into a jittery payout that finally conked out in 2020.

WPC’s “Recurring” Payout Dusts Ford’s Clunker

And if you buy REITs with two other advantages—long-term leases (ideally with yearly escalator clauses) and high occupancy rates—you get a dividend that’s largely insulated from competitive pressures (not to mention rising interest rates).

There’s one more factor that powers our REIT dividends: these trusts pay zero corporate taxes. With no taxes to pay (as long as they hand out 90% of their taxable income to us as dividends), REITs are left with more money to fuel their payouts.

But even with these advantages, we still need to be selective. We’ll lock in our forever cash flows by zeroing in on REITs with three strengths (besides top-quality properties tenants can’t live without):

- Growing dividends, which tend to pull a company’s share price higher. We’ll see this “set-your-watch-to-it” phenomenon play out in dramatic fashion a little further on.

- Rising funds from operations (FFO for short). This is the main REIT performance figure, and we want to see growing FFO (powered by increasing rents and in-demand properties) to back our rising dividend—and our upside.

- A safe payout ratio: With most stocks, I demand that no more than 50% of cash flow be used to support the payout. But REITs are different—due to their predictable recurring revenue, ratios up to 90% can be sustainable.

WPC ticks those boxes: its payout growth is supported by rising FFO (up 5% year over year in the second quarter) that’s backstopped by its 98% occupancy rate and rent escalators: of its total leases, 99% include contractual rent hikes, with 60% linked to the consumer price index, giving WPC a nice inflation hedge.

WPC is far from alone: there are plenty of other REITs successfully transforming recurring—and rising—FFO into rising dividends (and share prices!).

Consider self-storage REIT ExtraSpace Storage (EXR), which is raking in cash as people load up on consumer goods. ExtraSpace yields 2.7%, which is already 100% more than the average S&P 500 stock pays, but has boosted its payout a phenomenal 792% in the last decade. In other words, if you bought back then, you’d be raking in an incredible 22.4% yield on your original buy now.

We can clearly see EXR’s rising payout pulling its share price higher—the pattern is unmistakable:

EXR’s Recurring Revenue Drives Explosive Payout (and Price) Growth

ExtraSpace can easily keep this roll going, with its high 97% occupancy rate and its dividend accounting for a reasonable 76% of forecast 2021 FFO. Plus, management expects the REIT’s FFO to surge 24% this year.

The kicker: the stock is perfectly positioned to gain as supply chain kinks get worked out, giving consumers more products to buy—and store.

How We’ll Tap “Recurring Revenue” Stocks for Safe 7%+ Monthly Dividends

Big dividends like these—either paid “upfront,” like WPC’s 5.5% yield or built up over time through dividend growth (like ExtraSpace’s astonishing 793% in payout hikes) are the keys to funding the retirement you want.

To those I’d add one other thing: dividends that come your way monthly. That way your payouts match up with your bills. And if you’re reinvesting your dividends, monthly payouts let you do so faster than quarterly ones do.

And of course, we want those payouts backed by businesses with solid recurring revenue, so we don’t have to worry about a crisis wiping out our income stream—the same fate our unfortunate Ford investors met in March 2020.

To help you build your monthly dividend stream, I’ve assembled my “7% Monthly Payer Portfolio.” As the name states, it pays you 7%+ dividends that roll your way every month. So a $500K investment would pay you a reliable $2,917, month in and month out.

I’m ready to share this diversified high-income portfolio with you now. Click here and I’ll give you a complete guided tour, including details and other vital stats on every investment inside.