Today we’re going to build a portfolio that can make us totally financially independent with just $500K invested. And we’ll do it on dividends alone—without having to touch our principal.

Now I know that sounds outlandish in today’s low-yield world. Here’s how we’ll make it happen. (Hint: our plan involves three closed-end funds, or CEFs, paying dividends that dwarf the measly 1.3% you’d get from the typical S&P 500 stock.)

The Dividends-Only Retirement Portfolio

The principle behind retiring on $500,000 (or any amount, really) and being guaranteed of not outliving your nest egg is pretty simple: make sure the amount you’re taking out of your portfolio is less than what your portfolio earns you on a yearly basis.

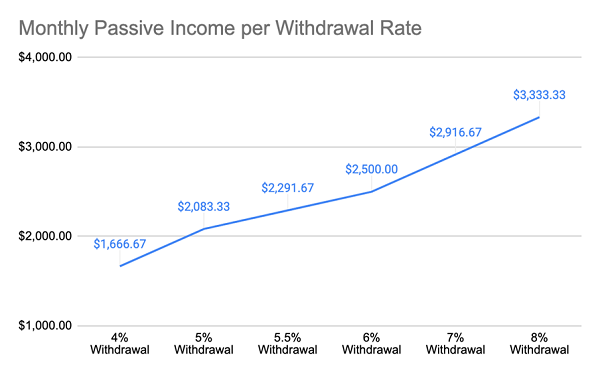

But how much can you take out of $500,000 without running out of cash? Previous studies suggested 4% was the magic number, meaning $500,000 would get you $1,667 a month in income. Let’s be honest—retirement is possible on so little, but that’s a pretty meager income stream.

More recent studies have pushed that number up a bit, and 5% seems now like a manageable amount, which translates into $2,083 per month on our $500,000. That’s better, but we’re still not much above the poverty line. Push that withdrawal rate higher (and with it your rate of return), and the money you can safely withdraw goes up, as well.

Source: CEF Insider

As you can see from this chart, the more you can take out of your portfolio without it going to zero, the more monthly income you have. Investors who can earn an 8% yearly return (including dividends) effectively get twice as much monthly income as those withdrawing 4%, and as long as their portfolio returns that 8%, they can keep withdrawing that amount of money from their account indefinitely.

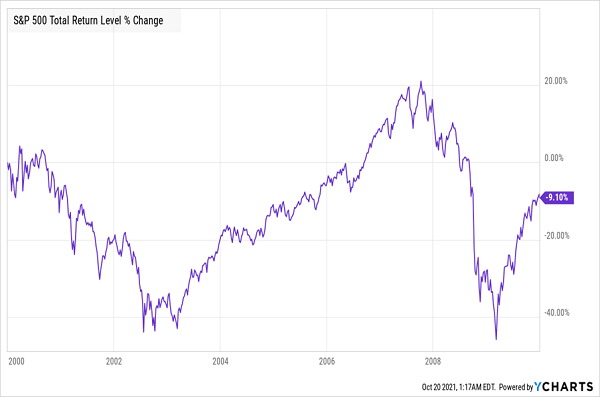

This is obviously hard to do! If you just bought an index fund like the SPDR S&P 500 ETF Trust (SPY), you could theoretically have been doing this for the last 50 years, since the S&P 500 has returned an annualized 10.8% since January 1970. But that nice headline number masks the fact that the long-term investor would face problems like the 2000s, when the S&P 500 lost money over the decade, due to two bubbles (tech stocks first, then real estate).

The Retiree’s Biggest Threat

You can minimize this problem, of course, with diversification. But then you’ll need to sell shares in several different funds, companies and other assets at different points, something that’s very time-consuming. In other words, you aren’t really retired; you’ve just become a money manager—with your own money!

CEFs: A Rich Hunting Ground for 7%+ Dividends, Market-Crushing Gains

This is where our dividends-only retirement play comes in—and those CEFs I mentioned earlier.

CEFs are smart retirement investments for two reasons. First, they’re diversified: the approximately 500 CEFs out there run the gamut of investments, including municipal bonds, large cap stocks, real estate investment trusts (REITs) and tech stocks. In other words, they let us contrarians focus on what’s undervalued at the right time and pivot when that investment gets overvalued. And we can maintain a diversified portfolio the whole time, too.

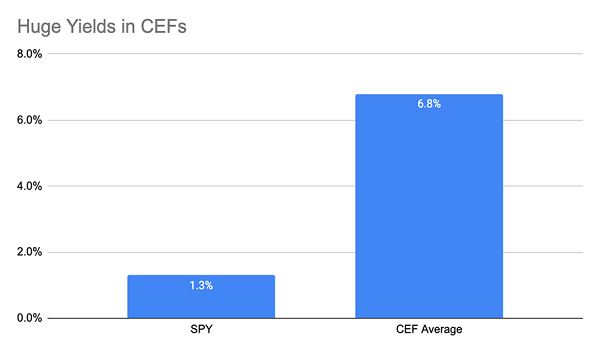

Secondly, and perhaps most importantly, CEFs yield 6.8% on average today, meaning you don’t have to constantly obsess over markets and be your own money manager. Just take the dividends and rebalance a few times a year. I can help you do that with the recommendations I make in my CEF Insider service, which, as current members know, focuses entirely on CEFs, particularly smaller CEFs, which boast the biggest upside in the space.

Source: CEF Insider

But 6.8% still only gets you less than $3,000 per month in income on $500,000, and we want more. Fortunately, we can do that by cherry-picking three funds with payouts that are higher than the CEF average and also boast strong returns since their IPO or over the last decade, whichever is shortest:

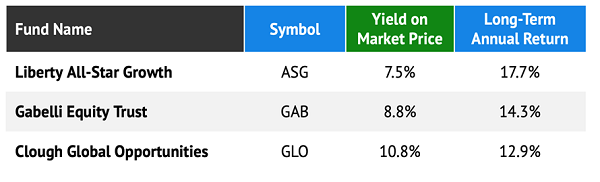

Over the long term, these funds have all vastly outperformed the market, with ASG’s total return (including dividends) coming in over twice the 8.4% yearly return we’d need to get $3,500 per month on a $500K investment. And since the average yield on all three funds is 8.9%, we can actually get more than $3,500 per month—$3,708, to be exact.

3 CEFs That Would Fuel a “Dividends Only” Retirement (on Just $500K)

That $3,700 figure is a decent middle-class income and enough to make a retiree comfortable in many parts of the world. And these three funds have delivered that much and more for investors.

It’s really no surprise these funds have been outperforming: ASG’s top holdings include fast-growing midcap stocks like Chegg (CHGG), property manager FirstService Corp. (FSV) and online lending platform Upstart Holdings (UPST); GAB owns reliable mega-cap names like Mastercard (MA), Deere (DE) and American Express (AXP); and GLO has a nice mix of top-performing tech firms, like Microsoft (MSFT), Amazon (AMZN) and Tesla (TSLA), as well as a mix of corporate bonds from across the market.

Alert: These 4 Massive Dividends Are Primed for Fast 20%+ GAINS

The only snag with these 3 funds is that they all trade at premiums to net asset value (NAV), meaning that investors are paying more than they’re actually worth! That’s an obvious cap on their upside, and it makes them more sensitive to a pullback in the next market downturn.

That’s why I’m insted urging readers to pick up the 4 other CEFs I’m recommending here. They yield 7.3% now, plus they’re all so deeply discounted that I expect them to soar 20%+, on average, in the next 12 months.

Think of what that could do for your retirement portfolio: for every $100K invested, you’d be looking at $7,300 in dividend cash, plus $20,000+ in price gains by this time next year!

That kind of dividend-plus-upside combo is exactly what we need to attain the financial independence we crave. Full details on this high-yield portfolio are waiting for you now. Click here and I’ll give you everything you need to know about these 4 powerhouse funds, including their names, tickers, current yields and my in-depth analysis of their management teams.