Most income investors limit themselves to mere “common” dividends. But there’s no need for us to settle for 2% blue-chip yields when we can bank 6%+ payouts from the same companies.

Let’s use Bank of America (BAC) as our example. The stock should keep sailing as the 10-year Treasury rate grinds higher.

Common shares of BAC yield just 1.8% today. (This is what we receive when we type in “BAC” and hit the “Buy” button.) That’s not much. Fortunately, we can look past common dividends for higher yields without sacrificing safety.

Companies also can issue what’s referred to as “preferred stock.” We hear them referred to as “stock-bond hybrids” because they boast elements of each. They trade on popular exchanges and represent ownership like a stock. But they tend to trade around a par value like a bond, and their “dividends” are fixed like bond coupon payments.

They also have some superior security qualities of their own:

- The dividends have “preference.” In most cases, dividends on preferreds must be paid out before common-stock dividends are paid, giving them a little protection from being cut or suspended in financially troubled times.

- Some preferred dividends are “cumulative”—which means if a company has to miss dividends for any reason, it must pay preferred-stock owners those dividends before they can dole out income to any other shareholders.

- They boast bigger yields. Namely, most funds dealing in preferreds at the moment yield several times more than the broader market at the moment. BofA, for instance? Its Series L preferreds yield a juicy 5%—that’s nearly 4x the S&P 500 right now! And most preferred funds will get you anywhere between 4% and about 7%.

These “pullback-proof” qualities attract many savvy retirement investors. Preferred ETFs tend to pay between 4% and 5%, and we can do even better by focusing our attention on closed-end funds (CEFs).

These actively managed portfolios are handpicked for the best preferred values. The result is higher yields and better returns. Let’s look at three well-run CEFs that yield between 6.2% and 6.9% today.

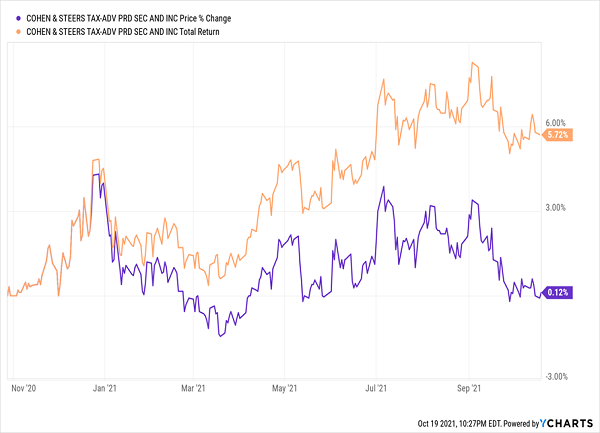

Cohen & Steers Tax-Advantaged Preferred Securities and Income Fund (PTA)

Dividend Yield: 6.2%

First up is a new CEF: the Cohen & Steers Tax-Advantaged Preferred Securities and Income Fund (PTA), which got its start just less than a year ago near the end of October.

Usually, when you hear “tax-advantaged,” that’s code for municipal bonds, which distribute income that’s exempt from federal (and sometimes state and even local) taxes.

This isn’t quite that, but it still provides a little bit of an edge up on the IRS.

Cohen & Steers says PTA “seeks to achieve favorable after-tax returns for its shareholders by seeking to minimize the U.S. federal income tax consequences on income generated by the Fund.” It does that in two ways:

- Invest in preferreds that pay qualified dividends (which many already do).

- Game holding periods to achieve favorable tax treatment—in other words, hold positions longer to get the favorable long-term capital gains rate.

Past that, much of the portfolio looks like your standard preferred-fund fare. Banking/insurance/brokerage/finance collectively make up more than three-quarters of the fund, including issues such as JPMorgan Chase (JPM) 6.75% preferreds, Wells Fargo (WFC) 5.875% preferreds and PNC Financial (PNC) 6.75% preferreds. The rest is sprinkled across utilities, telecoms, real estate and others.

PTA’s managers can do a few other things to juice returns, should they want. They can invest in common stocks, government bonds and even munis. But at the moment, the fund primarily does its juicing the good ol’ fashioned CEF way: with a hefty amount of debt leverage (currently 32%) to invest additional assets into management’s picks.

There’s precious little price and selection history to go off here, so just know you’re wading into mostly uncharted waters. But you’re getting a little bit of a bargain to do so—Cohen & Steers’ CEF trades at a 4% discount to its net asset value.

The Dividends Make the Difference

John Hancock Preferred Income Fund (HPI)

Dividend Yield: 6.9%

The John Hancock Preferred Income Fund (HPI) is a far more established preferred fund that has been around since 2002.

It boasts a portfolio of 121 preferred and preferred convertible securities, though management does have the option of also holding U.S. government agency bonds, corporate bonds, foreign bonds and both domestic and international stocks.

What sticks out about HPI is that it focuses on high credit quality. Specifically, management is required to dedicate at least half of its assets to investment-grade securities. It’s very close to that line right now, with a little more than 50% of assets in BBB-rated preferreds, but another 35% is in BB—junk, but its highest tier.

While high quality normally keeps a lid on yield, HPI’s 6.9% is at the high end of the preferred-fund spectrum. High leverage (32%) helps here, too, and juices price performance during strong periods for preferreds. It results in a bumpier ride than a vanilla index ETF, but ultimately, it’s for the best.

HPI Largely Gets the Job Done

Just note that, like many preferred CEFs at the moment, HPI is effectively “double charging” you—not just its regular expenses, but also a 4% premium to NAV (which itself is a little higher than its 2.5% five-year average premium), so you’re buying those preferreds at $1.04 on the dollar.

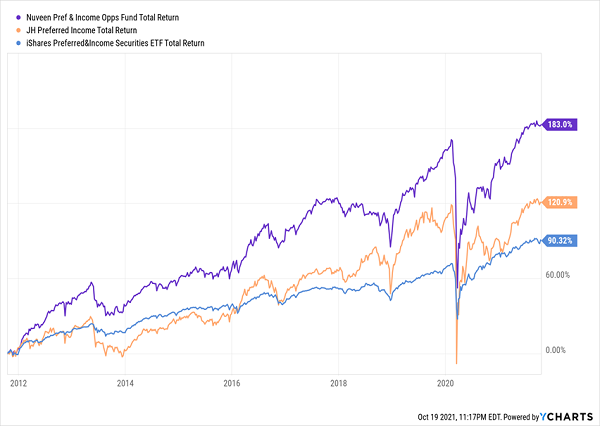

Nuveen Preferred & Income Opportunities (JPC)

Dividend Yield: 6.5%

It’s hard to make the same complaint about Nuveen Preferred & Income Opportunities (JPC), which at a fractional premium is as fairly priced as a CEF gets.

In fact, it’s hard to complain much about JPC at all. Because a few slight differences from HPI seem to add up in a big way.

A Real Preferred-Stock Powerhouse

Nuveen’s preferred fund, like HPI, will make sure its portfolio is at least 50% invested in debt rated BBB or higher—though right now, it’s somewhat higher at more than 60%. Financials shoulder most of the load, which is par for the course. Internationals play a bigger role in JPC, at roughly 30% of assets versus closer to 10% for HPI. It also uses slightly more leverage at 36%.

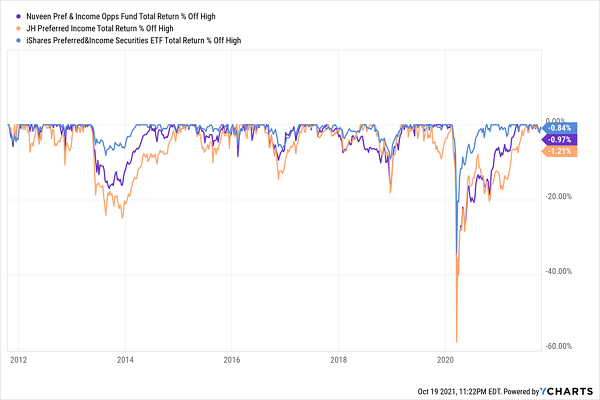

The overall performance difference alone is enough for investors to take notice. But also reassuring to long-term investors is a less volatile portfolio whose drawdowns are still deeper than an index, but not as sharp as HPI’s.

A Key to Successful Retirement Investing: Holdings That Keep Their Cool

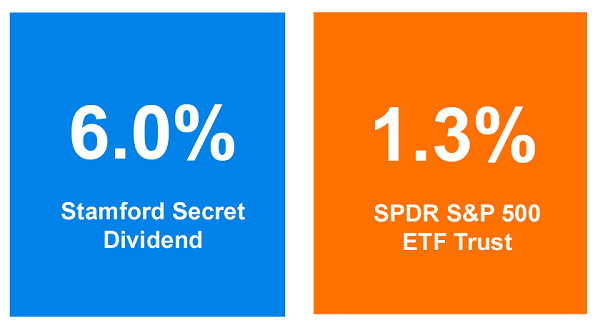

Mysterious “Stamford Secret” Dividend Plan Exposed

While all three of these funds are worth keeping an eye on, they can’t hold a candle to my absolute favorite preferred CEF.

It’s a secure 6% payer that will hand you $30,000 annually on a mere $500,000 nest egg. And it has a killer edge its competition can only dream of:

Its managers, an unsung duo from sleepy Stamford, Connecticut, get first crack whenever a new stock comes on the market!

You’ve always wondered what it would be like to buy Microsoft before its IPO. Or IBM. Or even Apple. Well, these guys can actually do it—in a fund that you can easily buy in almost any standard brokerage account!

No wonder this low-key duo ALWAYS beat their benchmark. An “automated” ETF simply can’t keep up with these “ultimate insiders.”

Powered by this hidden advantage, their fund throws off a massive 6% dividend that dwarfs the payout on common stocks:

Huge “Stamford Secret” Dividend Reigns Supreme

This terrific fund is a “must own” for anyone looking for inflation-proof income, whether you’re in retirement or still building your nest egg.

I’m ready to share all the details with you now. Click here and I’ll give you everything you need to know about this amazing income play, including its name, ticker symbol and full profiles of its high-powered management team.