Investors sometimes tell me that closed-end funds (CEFs) are complicated—riddled with jargon-y terms like discounts to NAV and net investment income (NII).

The truth is, while it may take a little bit of time to learn the ropes, the effort pays off in spades, since CEFs can get you about $3,000 per month in dividend income on a $500K investment! That could mean retiring a decade or more before folks who rely on low-yielding S&P 500 stocks or ETFs.

(And of course, if you’re a member of my CEF Insider service, I do the legwork for you, letting you collect our portfolio’s 7.3% average yield, with upside, without having to spend hours in front of a computer screen.)

To show you how simple CEF investing can be, let’s look at a three-fund portfolio that will get you 7% dividends you can depend on for a decade or more. Plus, between them, these three funds are well diversified, which helps minimize your risk.

High-Yield CEFs Made Simple

At the core of our “instant” portfolio are three assets: stocks (because they outperform other investments in the long run), bonds (to provide stable income in periods of uncertainty) and real estate investment trusts, or REITs (because they boast yields more than double those of regular stocks, and REITs tend to move independently of stocks in general).

This three-pronged approach—stocks, bonds and real estate—is how most investors create wealth and a comfortable retirement, so it’s a good backbone for our CEF adventure.

CEF No. 1: A Monster 9.6% Payout From America’s Best Stocks

For stock exposure, consider the Liberty All-Star Equity Fund (USA), which pays a whopping 9.6% yield and boasts a portfolio of America’s most successful companies:

Source: All-Star Funds

Top holdings Alphabet (GOOG), Amazon (AMZN), Facebook (FB) and PayPal (PYPL) tell you right off the bat that you’re getting the biggest and most important US tech giants when you buy USA. But don’t let that lean toward tech hold you back; while nearly a quarter of USA is in tech, financials (17.4%), healthcare (14.4%), and consumer discretionary (13.8%) are important parts of the portfolio, too, so it’s well diversified.

And you get that monster 9.6% dividend, which as we all know is far more than you’d get if you bought these companies individually or through an ETF.

Now let’s talk performance.

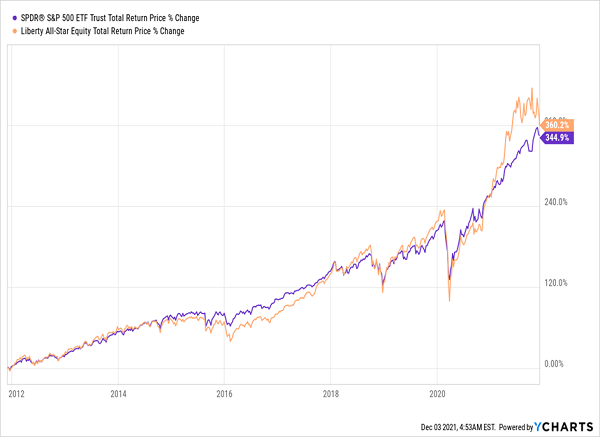

USA Outruns the S&P 500

USA’s portfolio has helped it beat the market, getting investors a 360% total return in a decade. And unlike those who bought the benchmark ETF, USA investors got much of their return in cash dividends.

Despite that gain, USA trades right around its net asset value (NAV) as I write this. That simply means its share price is roughly the same as the value of its portfolio (as CEFs can’t issue new shares to new investors once they’ve launched, they tend to trade above or below NAV, giving us a crystal clear indication of a fund’s value).

This fund has traded at premiums of more than 15% in the last year, so that par valuation is reasonable right now (though to be honest, we always prefer to buy at discounts).

CEF No. 2: A Tax-Free 4.5% Dividend That Could Be Worth 7%+ to You

Let’s move on to bonds, where the Putnam Managed Municipal Income Trust (PMM) is a great defensive play for shaky markets. As the name suggests, it holds municipal bonds, which are issued by states, cities and towns to fund infrastructure projects.

With assets spread across the US, this 4.5%-yielder gives you lower volatility, meaning you can keep it in your account, collect $375 per month for every $100K invested, and not have to panic about drops like we saw in early 2020 (or late 2018, or early 2016 or through 2007 and 2008).

Plus, for the vast majority of Americans, municipal bonds’ payouts (and by extension PMM’s dividend) are tax-exempt, meaning investors in the top tax bracket would have to earn 7.5% in dividends from stocks to get the same amount of net income.

Our only hesitation is that PMM trades at a 1.3% premium to NAV, well above the 0.5% premium at which it’s traded for the past year, which could hinder its upside. So you could go ahead and buy it now, but that premium could hinder its upside in the near to medium term.

CEF No. 3: A Dominant Real Estate Fund Trading at a Discount

Finally, let’s talk real estate. The 6%-yielding Cohen & Steers Quality Income Realty Fund (RQI) may not have the biggest yield in the CEF market (where the average payout is a bit south of 7%), but its yield is lower for the best possible reason: its stock price has soared.

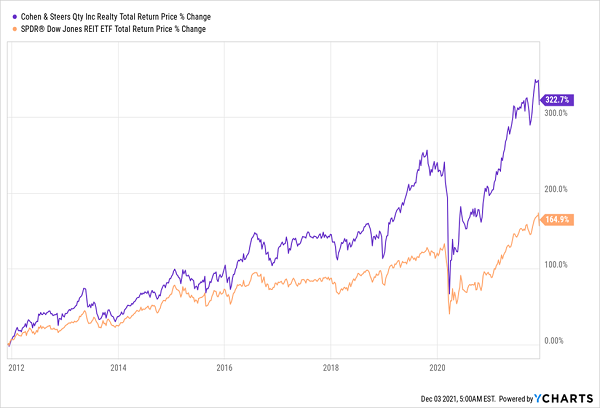

RQI Crushes Its Benchmark

Not only did RQI easily survive the COVID-19 selloff, it’s recovered far more than the REIT index and has continued to beat said index. That’s the real reason why RQI’s dividend looks so humble; with a payout that’s stayed stable for five years, this fund’s 8.1% yield in 2016 has fallen to 6%, since yields go down as prices go up.

But investors who bought RQI a year ago have gotten $100K in profits for every $100K invested, while the fund’s dividend has become safer and the chances of a dividend hike have risen. What’s more, RQI trades at an attractive 5% discount to NAV as I write this, which is below its 52-week average of 3.2%, so you can expect a bit of upside from that closing discount.

The Final Word: a 6.7% Dividend With Growth Potential (and Price Upside)

Combined, these three funds give you exposure to the three main asset classes most people invest in and give you a 6.7% income stream that’s likely to rise. That’s not even considering the tax-free status of the muni-bond income; take taxes into account, and for most Americans this is a well-diversified 7%+ yielding portfolio that can be bought with three clicks of a button.

4 Even Better Buys for 27%+ Returns in 2022

The best way to squeeze the biggest gains out of your CEFs is to buy when discounts hit ridiculously oversold levels, and while these funds’ valuations are okay, they’re not quite the screaming deals we like to see.

When discounts are truly absurd, from a historical perspective, you can set yourself up for some truly incredible gains indeed. The 4 CEFs I recommend you buy now, for example, have been unfairly tossed in the bargain bin.

That’s why I have them pegged for 20%+ in discount-driven gains in 2022. With a solid average dividend of 7.3% between them, it’s only a matter of time before investors realize their mistake and buy back in. Heck, it’s already starting to happen!

The time to buy these 4 income powerhouses is now. Click here to get full details on all of them: names, tickers, current yields, my complete analysis of their management teams and everything else you need to know before you buy.