A recession or more rate hikes in late 2023? We contrarian dividend investors don’t care—we’ve zeroed in on a group of stocks that will prosper no matter what.

Three, in particular, are begging us to buy them now. We’ll talk tickers in a moment, but let me start by saying they boast four key strengths we demand when we buy any stock in my Hidden Yields dividend-growth advisory:

- A healthy yield, so we’re starting off with a strong income stream.

- Rising dividends primed to keep soaring—and even accelerate. That increases our income stream, the yield on our original buy and, as we’ll see below, drives share prices higher, too.

- Megatrends—all three stocks below are tied into societal trends that will roll on for decades, defying any short-term pullback we might see.

- Low beta ratings: Beta is a volatility measure, and you can spot it on most screeners. Simply put, a stock with a beta of 1 trades more or less alongside the market. Betas below 1 are less volatile, while those above are more volatile.

With that in mind, let’s dive into our trio.

First Industrial: Cashing in as US Industry Comes Home

First Industrial Realty Trust (FR) owns 442 warehouses across the country, with a focus on the coasts. Hidden Yields members who’ve been with us for a while will remember this one—it handed us a 28.5% return in a bit less than two years the last time we held it, from May 2016 to March 2018.

These days, FR’s worth another look, as the “onshoring” trend has picked up since we sold. (Onshoring refers to US and multinational companies shifting their operations to the US and away from basket cases like Xi’s China.)

Every month, it seems, we’re reading about a new factory opening in America: just in June, LEGO Group announced a $1-billion facility in Virginia; Kubota rolled out plans to expand in Georgia; and a bevy of pharma companies announced openings of new facilities in South Carolina and Maryland.

All that new hammering, welding and assembling happening on American shores has cranked up demand at FR’s warehouses: in the first quarter, occupancy was 98.7%, up from 98% a year ago. And space at its three new developments literally flew off the shelves, with all three booking 100% in Q1.

So it’s no wonder management boosted guidance, to $2.33 to $2.43 in funds from operations (FFO, the key profitability metric for REITs like FR) for all of 2023. The dividend occupies just 54% of the midpoint of that range, so it’s plenty safe.

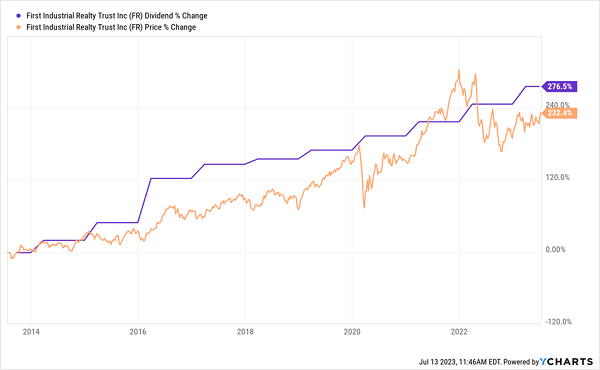

Speaking of the payout—one reason why we sold FR is that its dividend growth had gone a bit flat, as you can see below. But it’s been sprightlier lately, which has drawn more attention to the stock—and driven the price up in lockstep:

First Industrial Hammers Its Payout—and Price—Higher

As you can also see above, the stock now lags the dividend—and it tends to “catch up” over time. That’s another sign of upside potential here.

With onshoring showing no signs of easing, warehouses in the right spots to capitalize and FFO on the rise, FR’s payout growth could accelerate, pulling the share price higher as it does.

So why haven’t we re-added this one to Hidden Yields? First, the 2.2% yield is a little low, and the five-year beta of 1, which is about the same as the market is a little high for us—especially these days, with the S&P 500 looking a bit toppy. But if you can live with those caveats, this stock could be worth a buy.

BCE: An Overlooked Telco With a Surging 6.4% Dividend

BCE Inc. (BCE), is a 143-year-old Canadian telecom provider with a 6.4% payout that’s growing like a weed.

The appeal of investing in Canadian telcos is that the three biggest players: BCE, Telus Corp. (TU) and Rogers Communications (RCI), form an oligopoly that competitors have a tough time cracking. BCE is the largest of the lot, with 30% of the market.

Meantime, Canadian mobile-data use continues to rise, totaling an average 6.07 GB a month in the third quarter of 2022, nearly triple the amount used in the same quarter four years earlier.

And the best part for the “Big 3”—but not their customers!—is that Canadians pay the world’s highest cellphone rates.

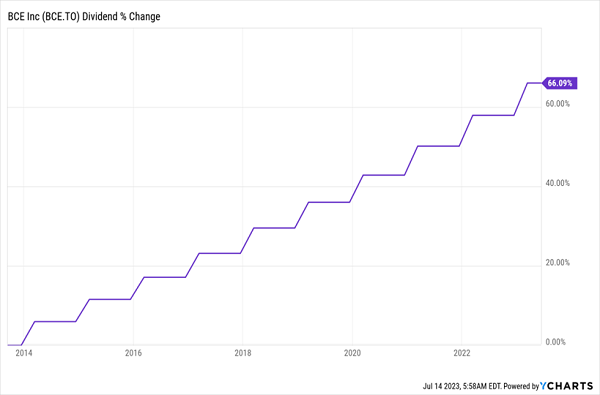

It all adds up to about the closest thing to “guaranteed” sales growth there is—and BCE is dishing that cash as dividends. As you can see below, not only does the company boast a 6.4% yield, it’s sent its dividend up 66% (in Canadian dollars) in the last decade. What’s more, BCE trades at 18.4-times forward earnings, below its five-year average of 19.3.

BCE’s High-Speed 6.4% Dividend

The stock checks out on the volatility scale, too: its 5-year beta of 0.49 gives it the kind of stability folks who hold S&P 500 index funds would love to have.

One other quick note: you won’t have to open a Canadian brokerage account to buy this one—it trades on the NYSE under the BCE ticker.

Also, because BCE pays dividends in Canadian dollars, your payouts won’t show the clean line of growth you see in the chart above. But the “loonie” has been relatively stable against the greenback recently. And with the Bank of Canada hiking rates at more or less the same speed as the Fed, that’s likely to continue.

Abbott Labs: A Healthcare Dividend That’s Overdue for a Bounce

Healthcare is backed by one of the most reliable megatrends there is—the aging of the population, and the matching rise in healthcare spending. According to the Centers for Medicare & Medicaid Services, the US will spend 5.1% more a year on health, on average, until 2030, when the total bill will come in at $6.8 trillion.

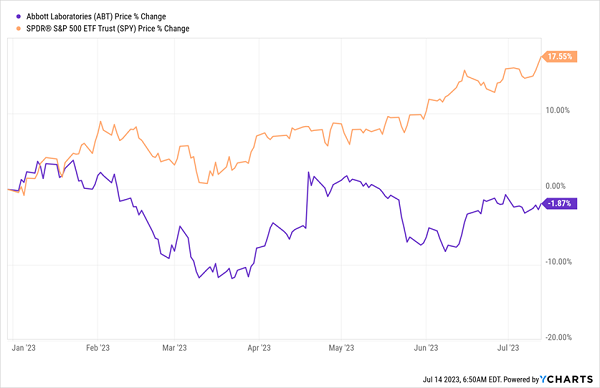

Yet healthcare stocks—including testing and diagnostic equipment maker Abbott Laboratories (ABT)—have been left out of the 2023 rally.

C’mon Abbott, What Gives?

That makes healthcare a coiled spring, and Abbott an interesting stealth pick.

The company has been a major supplier of COVID tests, and now that the virus has become endemic—cutting the need for testing—Abbott’s seeing major sales declines. Organic sales at its diagnostics business, for example, plunged 47.1% in the first quarter. But this was expected: strip COVID tests out and these sales rose a healthy 4.4%.

Meantime, Abbott continues to see strong demand for its diabetes products, including its Libre Freestyle system, which helps patients better monitor their glucose levels. The need is definitely there, with the disease afflicting 11.3% of the US population, according to the Diabetes Research Institute.

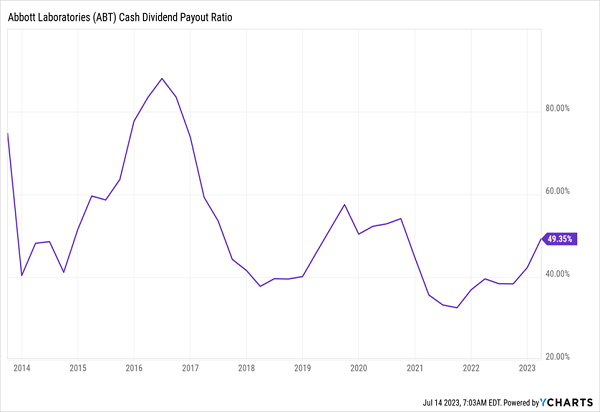

Despite any overhang from COVID test demand, this Dividend Aristocrat—it’s hiked payouts for 51 years and paid dividends for 99—has plenty of room for more hikes, with the payout occupying just 49% of its last 12 months of free cash flow. And while that’s crept up lately, it’s still near decade lows:

ABT’s Healthy Dividend Coverage

That growth is enough to convince us to overlook ABT’s low current yield of 1.9%, as its powerful Dividend Magnet continues to work its magic on the shares.

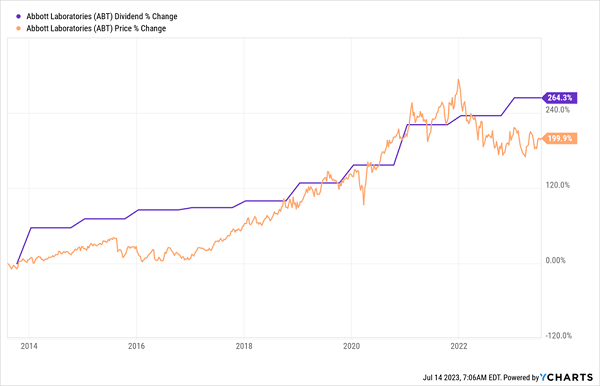

Abbott: Another Dividend-Up, Share-Price-Up Winner

As with FR, we’ve seen a gap between price and dividend growth lately. That, plus the general lag of healthcare stocks this year, points to more upside for ABT, despite its seemingly high forward P/E of 24.

Last up, ABT sports the low volatility we crave: with a five-year beta of 0.68, it’s 42% less volatile than the S&P 500.

5 “Dividend Magnet” Winners Set to Send Your Income Soaring

The pattern we saw with the stocks above—of a soaring dividend yanking the share price higher—is no fluke. It happens again and again and again with dividend stocks.

I call it the “Dividend Magnet,” and it’s one of the most -reliable patterns I’ve seen in investing. And I’ve uncovered 5 stocks whose Dividend Magnets dwarf the power of those of the two stocks above, with faster-growing payouts—and surging share prices to match.

The time to buy these 5 “dividend accelerators” is now. Click here and I’ll tell you more about my Dividend Magnet strategy and show you how to download a FREE Special Report revealing the names, tickers and my latest research on these 5 winners.