This levitating stock market has brought back worries about a crash (and a recession). I know, I know. We’ve been hearing that doomsday forecast for what feels like forever—and nothing of the sort has come to pass.

But a recession will eventually show up. We just don’t know when. In the meantime, stocks could keep drifting higher.

We do not want to miss out on that. But we do want to pay special attention to assets beyond stocks now (and minimize the amount we have sitting in cash, by the way, which is getting eaten up by still-hot inflation).

This is where corporate bonds (many of which are oversold) enter the scene, particularly bond-focused closed-end funds (CEFs), many of which yield well over 8%.

3 Cheers for Corporate Bonds

There are three reasons why corporate bonds are timely pickups now.

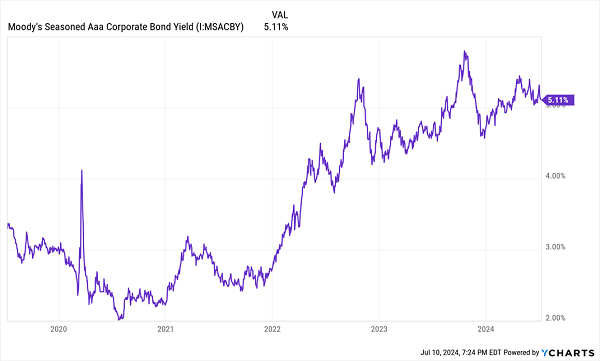

- Yields Are Soaring

Bond yields have soared with interest rates—and corporate bonds are now paying out more than they have in decades. The average high-quality, high-ranked bond, something that Apple (AAPL) or Amazon.com (AMZN) would issue, yields 5%+ now, more than double what it would have yielded in the 2010s.

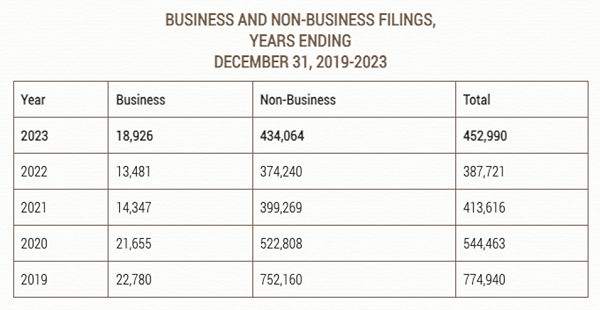

- Bankruptcy Rates Are a Non-Issue

Higher yields sound like a risk for corporate managers. Surely if businesses are paying more to borrow, more of them will fail, right? It sounds logical—until we remember that most firms have profit margins above 5%, so borrowing money is still profitable, just not as profitable as it used to be.

As a result, the total number of business bankruptcies are below pre-COVID levels today, even though there are more companies than there were then.

Source: United States Courts

This means just 0.22% of US firms are going bankrupt today, fewer than the 0.28% in 2019, itself a historically low number. Businesses are clearly having no trouble paying the higher rates on their debts.

- (Some) Corporate-Bond Funds are Underpriced

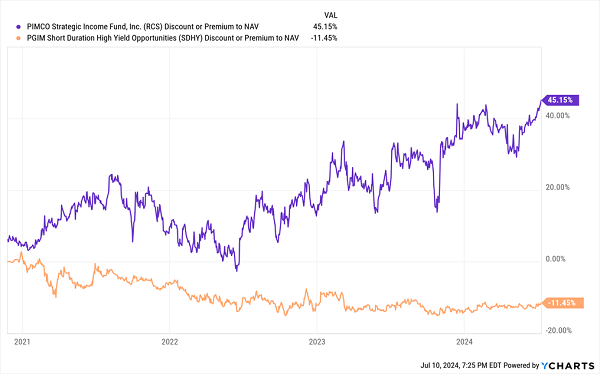

Which brings us to our favorite way to invest in corporate bonds: through CEFs. In addition to their 8%+ yields, corporate-bond CEFs trade at average discounts to net asset value (NAV, or the value of their bond holdings) of around 3.9% as I write this.

There’s a wide range of discounts within that average, including overly popular options like the PIMCO Strategic Income Fund (RCS), which, as you can see in purple below, trades at a 45.2% premium to NAV! That means we’d pay nearly $1.45 for every $1 of assets.

2 Bond Funds, 1 Obvious Bargain

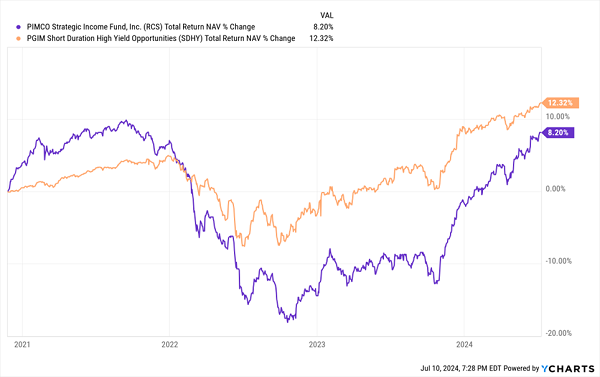

Meanwhile, there are plenty of bond funds trading for less than their portfolio value, like the 11%-discounted PGIM Short-Duration High Yield Opportunities Fund (SDHY), in orange above. That discount is surprising, as SDHY has outrun RCS on a NAV basis since SDHY’s inception in late 2020:

SDHY Is the Clear Winner

Of course, neither fund has been a great long-term hold, simply because interest rates were basically zero from 2020 to the start of 2022. And both funds were designed for a higher-rate world like the one we’re in today.

In the case of SDHY, the fund’s shorter-duration focus is also driving its discount lower. But the fact that rates have stayed “higher for longer” means this is priced in a little too much at the moment, making the discount overly large.

And while stocks have priced in many of the improvements in the US economy, corporate bonds haven’t. Which is the basis of our opportunity here.

Plus, if you buy a fund like SDHY, you’ll be drawing the fund’s outsized 8.4% income stream—a payout that rolls out monthly and has been as predictable as tomorrow’s sunrise since the (admittedly young) fund’s launch.

A Steady (Monthly) 8.4% Yielder

Source: Income Calendar

Admittedly, this is less than RCS’s 9.5% yield, but that’s fine because the potential upside from SDHY’s discount narrowing makes it a better buy than pricey RCS. Moreover, SDHY’s discount means the odds of its price falling fast are low (as the fund is already cheap) compared to RCS.

Finally, SDHY’s bond focus makes a strong total return more likely, even if stocks see short-term volatility or the bull market comes to an end.

If it takes longer for that discount to vanish than expected? No problem! Buying today means collecting that 8.4% income stream in the meantime. We can also sleep well at night knowing we didn’t buy an asset that could see a 50%+ price drop like an overpriced fund such as RCS could face.

5 More (Cheap) Monthly Paying CEFs Paying More Than SDHY

With CEFs, you can build an entire portfolio of funds, like SDHY, that pay dividends every month. Try doing that with regular stocks or ETFs. There just aren’t enough monthly payers to make it work.

Many CEFs, meanwhile, offer investors dividends every single month, right in line with their bills.

To help you build the biggest (and safest) monthly income stream you can (on as small of an upfront investment as possible), I’ve released a 5-CEF “Monthly Payer Portfolio” I’m urging income investors to buy now.

The 5 CEFs inside yield 9.2% on average and are primed for 20%+ price gains in the next year, thanks to their deep discounts.

I’ve put all the details on this portfolio, including a free Special Report you can download naming all 5 of these monthly paying CEFs, in an informative investor bulletin you can read right here.

Don’t miss your chance to “lock in” this 9.2%-yielding monthly income stream before the Fed starts cutting rates. When that happens, income-starved investors are likely to bid these 5 CEFs’ prices higher—and send that 9.2% yield lower!