Rate cuts are finally here. So will we actually hit that vaunted “soft landing” everyone’s been talking about?

Well, I’ve got a (contrarian, naturally!) take that I know most people haven’t thought about—especially since last week’s jumbo 50-point rate cut dropped:

What if we hit a “no landing” scenario, where the economy ticks along and inflation comes back?

I’m bringing up that unpleasant idea because, usually in a rate-hiking cycle like the one that just ended, the central bank pushes the Fed funds rate higher until it breaks something.

But this time, it’s not clear it has.

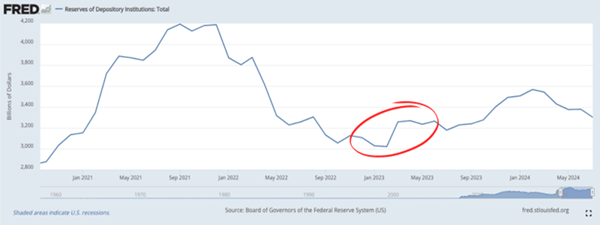

In fact, when it looked like it finally had—when Silicon Valley Bank and friends crumbled to dust in March 2023—Jay blinked, and pumped liquidity into the market through the back door, a move we’ve referred to as “Quiet QE” here many times before:

The Fed Didn’t Break Anything This Time—That May Be a Problem

With that in mind, last week’s oversized cut was understandable: The Fed has been keen to take its foot off the brake for a while now. Now that inflation is close(-ish!) to its 2% target, it’s making its move.

But here’s the thing: The government’s deficit spending is completely out of control. It is possible, perhaps probable, that Uncle Sam will overwhelm Powell.

For fiscal 2024, the Congressional Budget Office (CBO) projects a $1.9 trillion deficit on $4.9 trillion in tax receipts. (And yes, this is the CBO that paints its projections with rose-colored ink.) So we have nearly $5 trillion in revenues, and almost $7 trillion in expenditures.

A 40% overshoot.

Give me an extra $2 trillion, and I’ll show you a good economy! But the resulting monetary inflation could flow back into consumer price inflation. So how do we profit if rates bottom before the media expects them to?

Here’s an answer that might surprise you: We’re buying a company that lends money to small businesses.

Get Set for “Refi Wave 2.0” (But on the Business Side This Time)

We’re going with a small-business lender because an economy that’s nicely humming along will encourage companies—especially smaller, domestic firms seeing strong demand—to expand in the near term.

In the long run, if rates show a hint of moving up, these same firms are also likely to try to front-run them by moving up their expansion plans.

It reminds me of the “refi wave” of 2020.

Remember that? I sure do. Your income strategist nearly missed the window to get in on it, despite many reminders from my wife. Fortunately, I managed to wake up and lock in a 2%+ mortgage before rates skyrocketed (and I wound up sleeping on the couch!).

I bring this up because we could see something similar on the business side: At any hint of rates bottoming, I expect the nation’s companies to borrow more upfront to “lock in” an attractive rate, just like homeowners did.

And Ares Capital (ARCC) will be here for it.

Ares is a business development company (BDC), a class of firms that lend to small businesses. These days it’s nearly impossible to get a business loan from a bank, so BDCs have stepped in to fill the gap, providing debt, equity and other finance solutions.

A key thing to keep in mind about BDCs is that they get special tax privileges, and in exchange, they must return at least 90% of their taxable profits to shareholders as dividends. They trade just like regular common stocks, with tickers we buy and sell.

(If this sounds like a real estate investment trust, or REIT, to you, it’s because REITs get the same deal from Uncle Sam.)

As with REITs, the tax savings mean more money available to send out to us as dividends, juicing the yields on these stocks. (ARCC, as we’ll discuss momentarily, pays an outsized 9.5% dividend today.)

Ares, unlike many BDCs, builds real long-term value (I’ve been hard on BDCs in the past for chasing too many bad loans instead of creating shareholder value). Ares was, for example, one of the only BDCs that kept on lending in 2020.

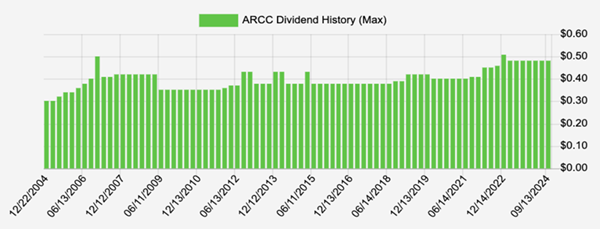

On the dividend front, the company’s 61 cents a share earnings last quarter easily covered the 48-cent per share payout. A 79% payout ratio is great in the land of BDCs.

And about that dividend: Ares not only yields 9.5% but has a history of hiking its payout. I know I don’t have to tell you that this is a rare setup in dividend-land: We usually have to pick between a payout that grows (but with a low current yield) or a high yield now.

ARCC gives us both!

Look at this chart, generated through our recently upgraded “toy” here at Contrarian Outlook—our Income Calendar dividend tracker (more on it below):

A 9.5% Payout That Grows? That’s Business as Usual at Ares

Source: Income Calendar

The “bump” at the end of 2022 was a special dividend. Ares keeps a “spillover” of extra earnings that it pays out to shareholders periodically, or it may choose to keep these funds on hand for a rainy lending day.

Plus, Ares increased its net asset value (NAV) over the past year. And those gains may begin to accelerate with a reheating economy.

Quick, Tell Me How Much in Dividends You’ll Get in October (Bet You Can’t)

ARCC is a pretty sweet pickup as rates drop, and I’ll go you one better. Once you’ve bought this sweet 9.5% divvie, I’ll give you a “one-stop” setup for tracking this rich payout (and indeed payouts from your whole portfolio) as it drops into your account.

It’s called Income Calendar, and if you use an “old-school” spreadsheet to track your payouts (or nothing at all!) it’s an absolute game-changer.

IC tells you when (down to the day) and how many (down to the penny) dividends your portfolio will kick out in the week, month and year ahead.

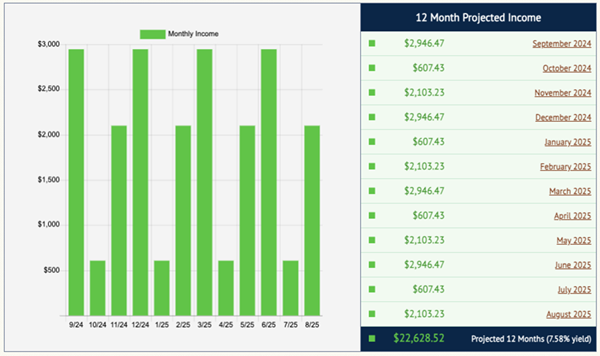

Let’s plug ARCC into Income Calendar so you can see it in action, along with a couple other high payers folks who subscribe to my Contrarian Income Report service will recognize: pipeline operator Antero Midstream (AM), with a 6% yield, and the monthly paying Reaves Utility Income Fund (UTG), current yield: 7.3%.

Let’s say we invest $100,000 in each of these three high payers. Income Calendar tells us, immediately, what we can expect in terms of dividends every month from our 3-buy “mini-portfolio”:

Source: Income Calendar

As you can see, with just these three buys, we’ve got dividends ranging from $607.43 all the way up to $2,946.47, and a total of $22,628.52 in dividends on the year, on just $300K invested. Sweet!

You can get complete breakdowns by stock, plus a month-by-month calendar giving you a heads-up on earnings dates, ex-dividend dates and other critical periods for every one of your holdings. Instantly!

Check it out. Here’s what our 3-buy portfolio shows us for December, one of our highest-paying months:

Source: Income Calendar

We can see our projected pay dates, as well as ex-dividend dates (the dates before which we need to be “in” the stock to get the next payout) and even things like market holidays.

We even get a heads-up on when our stocks are due to report earnings—though there are none of these for our trio in December (understandable, due to the holiday season).

So long, spreadsheet, hello, extra time.

Now is the perfect time to try Income Calendar, as we’ve just added a bundle of new features, including the ability to link to any brokerage (including Fidelity) in a few clicks, so you don’t even have to manually enter your portfolio. IC does it for you.

Plus you now get instant email alerts when you receive dividends, a yield on cost calculation (so you can see the “true” yield on each of your stocks, based on the timing of your original buy) and more.

Click here and I’ll tell you more about this powerful dividend planner and give you the opportunity to “road test” it out for yourself. I’m sure you’ll love it.