CEFs are renowned (by the few people who know about these high-income funds, of course!) for their outsized dividends—around 8%, on average, across the board as I write this.

But buying a CEF is not like buying a regular stock. When it comes to picking CEFs, we’ve got a whole bunch of different factors sitting in front of us that we need to weigh.

Sometimes CEFs Are Cheap for a Reason

There are, for example, some things that go beyond, say, past performance or discounts to net asset value (NAV, or the value of a fund’s portfolio—the main measure of a CEF’s value).

For example, funds sometimes change management teams, and because CEFs are so far off the media’s (and Wall Street’s) radar, changes like these get almost no coverage.

That’s too bad for CEF newbies, but it’s great for those of us in the know on these funds, because a change at the top can quickly rejuvenate a CEF, making a lousy performer an attractive pickup. (Changes like these are among the things we look for when picking funds for my CEF Insider service.)

Beyond that, there can be a time when buying a “bad” CEF can be a good idea. I know that sounds counterintuitive, but this can crop up when a poor performer is discounted so much that it’s priced like an even worse fund than it is—making it a great buy.

Now, I can’t go through everything that makes a fund “good” or “bad” because there are just too many things one has to weigh: management, fees, the discount, the portfolio, the fund’s mandate, economic conditions and the fund’s management team are just some of these.

So instead of telling you how to know if a CEF is great or potentially a losing pick, it’s better if I show you instead.

For this exercise we’ll look at two municipal-bond CEFs, although much of what I’m going to go over applies to other kinds of CEFs, too. (The key thing to know about “munis” is that their dividends are tax-free for most Americans, so their headline yields could be worth more to you, depending on your tax bracket.)

Let’s start with PIMCO Municipal Income Fund II (PML), with a 5.5% yield (before the fund’s tax advantages are factored in) and the BlackRock Municipal Income Fund (MUI), with a 5.3% dividend.

These are the best- and worst-performing muni-bond funds of 2024, and they’ve each had assets under management above $200 million over the past five years.

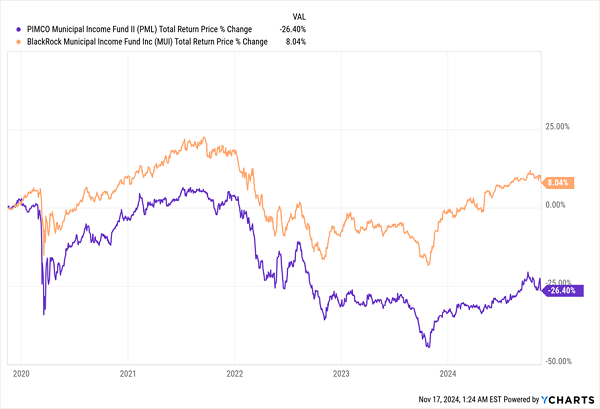

Past Performance: MUI Takes an Early Lead

First off, I should point out that even the best fund here—MUI, in orange above—has had a weak showing of just 8% gains in the last half-decade. This isn’t surprising given that the last few years have been difficult for muni bonds in general (which is why we’ve been trading lightly in the space in CEF Insider—as I write, we hold just one muni-bond CEF in our 18-fund portfolio).

This is the first takeaway with CEFs: the actual asset class you pick matters a lot, in terms of not only past performance and future outlook but also how the fund fits your portfolio diversification and personal goals.

Now, as we’re talking about funds, the first thing that may come to mind for you is fees: I am honestly flabbergasted at the degree to which investors focus on fees, especially since fees and actual returns have no real correlation in the CEF world.

That’s a bit of a spoiler because, you guessed it, the lower-fee fund did not overperform here. PML’s fees are 2.28% of assets in total, while MUI’s are 3.94%. (Note that all performance figures shown in this article are net of fees.)

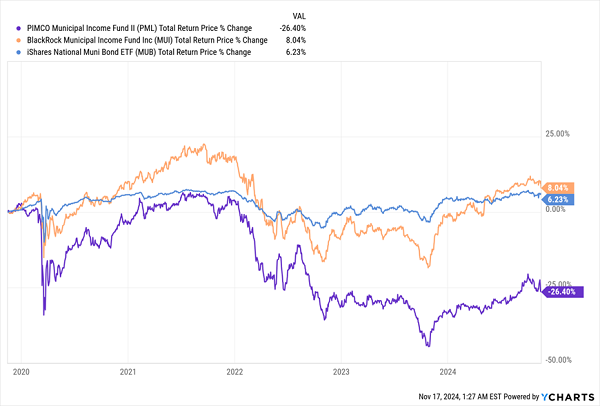

Both numbers seem high to investors used to index funds charging almost 0% fees, so let me show you that the muni-bond index fund, the iShares National Muni Bond ETF (MUB), with a 0.05% expense ratio (in blue below), did outperform PML (in purple) but did not outrun MUI (in orange), whose fees, as I just mentioned, are 3.94%—many times those of MUB.

MUB Beats PML, Not MUI

This again shows that the link between low fees and fund performance is shaky at best.

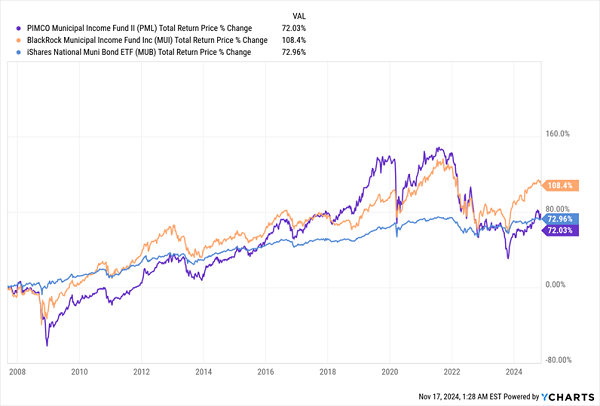

And if we zoom out, we find something interesting: While PML did lag the pack in the five-year chart above, over the longer run (since the 2008/2009 financial crisis), it did closely match MUB (in blue in the chart below) and had a pretty strong long-term return, although still far behind MUI’s doubling (in orange below).

Long-Term, MUI Still Wins

So in sum, while we’re seeing PML track the ETF in the longer run, the last five years have seen it lag badly. So what went wrong? When a CEF sees a sudden reversal like this, the first thing to look at is its market price relative to its NAV.

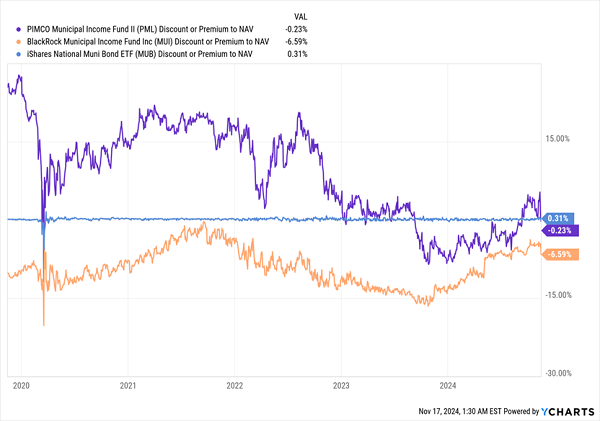

PML’s Problem Emerges

Like all ETFs, MUB (in blue above) trades close to its NAV, which shouldn’t surprise us (but this also underscores how little alpha you get from ETFs: Why not buy an asset class at a discount, like you can with CEFs?).

Plus, we see that MUI (in orange) trades at a discount (unsurprising again, since most CEFs are discounted). But note how that discount has been disappearing as the Fed shifted away from rate hikes and toward cuts. That makes sense, as lower interest rates raise the value of bonds.

So it’s no surprise that MUI’s absurd 15% discount would start to evaporate. Another thing to bear in mind is that MUI is a BlackRock fund, and the fund helped erase that discount with a buyback announcement earlier this year (I discuss that in detail here), ensuring more profits in the short term for investors who bought ahead of this development.

The PIMCO fund (PML), meantime, was trading at a huge premium to NAV throughout the early 2020s, when muni bonds struggled. So why would the market price PIMCO’s muni-bond fund at a premium when municipal assets were being discounted elsewhere? The simple answer is a little weird: geography.

PIMCO is based in California and courts a lot of Californian wealth managers who don’t pay as much attention to their clients’ portfolios as they should and as a result don’t sell these funds from their clients’ portfolios when they’re overpriced. That causes premiums that tend to last. Investors saw this inefficiency and started selling PML in 2022.

This was also a year when all assets were crashing and some investors sold to increase their portfolios’ liquidity, causing demand for PML to fall and its premium to disappear. The fund’s underperformance has just exacerbated the trend.

So where does that leave us? Right now, still-discounted MUI is the best pick of these two. There’s no reason why the fund can’t get the price premium that PML once had as it attracts more investors—especially with the Fed now in rate-cutting mode.

Beyond Munis: 4 High-Yielding CEFs (9.8% Yields) That Let You Cash in on AI

A second ago, I mentioned that you can tap into any corner of the economy with CEFs, drawing a huge yield as you do.

I meant it.

Take, for example, AI, a technology few people associate with high dividends. But that changes right here, because I’m pounding the table on 4 CEFs that let us tap into AI at big discounts, and collect outsized cash payouts while we do. I’m talking monster 9.8% yields here!

From AI kingpins like Microsoft (MSFT) and NVIDIA (NVDA) to smaller firms developing the next stage of this breakthrough tech, these 4 CEFs get you in on them all at a bargain. I know I don’t have to tell you what a rare setup this is in AI-land these days.

Don’t miss your chance to buy these 4 funds while they’re still off most investors’ radar. The next big AI announcement could drop at any time, sending them on their next let up.

By then it will be too late. Click here and I’ll tell you more about all four of these unusual funds and give you a free Special Report revealing their names and tickers.