I think it’s clear by now that Trump 2.0 is going to look different from Trump 1.0.

Some areas, like tariffs, look similar to the first time around (though we expect more of them in the second term). Others are totally different. (Hands up if you had a potential crackdown on processed food by an RFK Jr.-led HHS on your bingo card.)

“Big Food” to Take a Hit, Fertilizer Stocks a Smart Buy in Trump 2.0

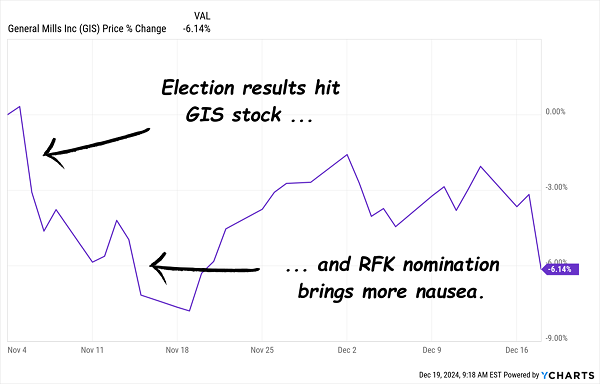

Let’s start with food stocks, which, as mentioned, are now a target for RFK Jr., should he be confirmed as HHS secretary. To be sure, that’s bad news for General Mills (GIS), which dropped following the election and again when RFK Jr.’s nomination was announced.

Add in last week’s volatility and GIS has had a very rough autumn, indeed:

Election Fallout Gives GIS Indigestion

That should be expected for a purveyor of products like Cocoa Puffs and Cookie Crisp. But to hear the pundits tell it, the “RFK factor” is the only thing worth watching in the food business right now.

Nonsense! Because while we certainly avoid stocks like GIS (mainly because of its relatively slow-growing payout), there are certainly other dividend-growing food stocks primed to soar in Trump 2.0.

Like stocks that make fertilizers and other products that boost crop yields. Because whether RFK Jr. is confirmed or not, Americans (and all of humanity, for that matter) will still eat boatloads of grains in Trump 2.0, just like they did in Trump 1.0.

It’s a “baked in” (sorry, I couldn’t resist!) global trend: According to the UN, there will be 9.7 billion people on the planet in 2050, nearly 2 billion more than now. That means we’re going to need a lot more food. And yet …

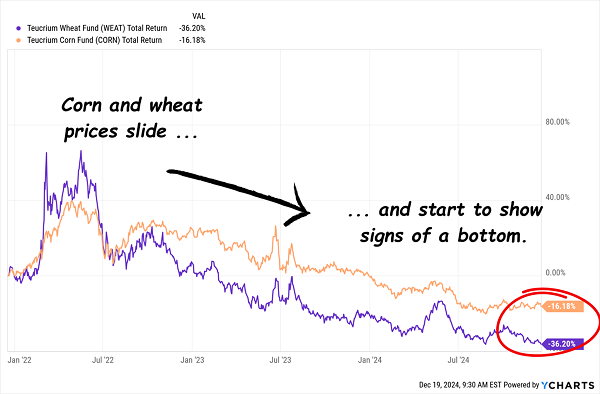

Wheat and Corn Prices Plunge, Setting Up the Next Jump

Corn and wheat prices, you may recall, spiked in the spring of 2022, when Russia invaded major wheat exporter Ukraine. Farmers boosted their output in response, spiking the prices of corn, wheat—and the fertilizer needed to grow them.

Of course, excess supply did what it always does: clobbered prices. But they won’t stay cheap because, well, they never do. Low prices are the cure for low prices, and that’ll be the case here, as farmers plant less corn and wheat in favor of something else, such as cotton, creating a supply shortfall—and setting the stage for the next price upturn.

That upturn will drive up demand for fertilizers, and CF Industries (CF), one of the world’s biggest fertilizer producers, will be waiting.

Its fertilizers are widely used on wheat, corn and soybeans. That gives it a direct tie to rebounding crop prices. CF had already forecast that fertilizer demand will outpace supply over the next four years. And that was before the election.

The dip in crop prices and last week’s volatility have given us a dip to buy CF shares, and we know CF is a bargain because, well, management has been telling us that through their share buybacks, to the tune of 16% of the company’s float in the last three years.

The other kicker here is the company’s return to dividend growth in 2021, and the 67% hike to its payout since. A bounce in crop prices, plus the fact that CF pays out just 20% of its free cash flow (FCF) as dividends, should keep the payout popping. All that, plus management’s ongoing buybacks, should combine to give the stock a lift as the next administration settles in.

Tariffs Are a Red Herring for This Humble Lock Maker

To be sure, China tariffs are a potential headwind for Allegion PLC (ALLE). Let’s remember that tariffs aren’t a guarantee; they may be a negotiating chip.

Also, ALLE has a large manufacturing footprint, including in the US, where flagship brand Schlage has a factory in Colorado Springs. Moreover, the company has the flexibility to move more production to the US if necessary.

The stock returned 84% during Trump 1.0, and I’m expecting it to post another strong performance in the coming months as a continued robust economy and strong market for its security products—including manual and electronic locks—continues to grow.

On November 20, for example—well after the election—construction consultant ConstructConnect forecast a 6.9% increase in non-residential construction in 2025, and a 12% increase in residential construction.

You can draw a direct line between those numbers and lock demand, which is likely why Allegion raised its EPS guidance in its Q3 earnings report.

Further dividend growth is a “lock” (sorry again!) here too, with the payout up 380% in the last decade—and even then, it still accounted for just 28% of the last 12 months of FCF. So ALLE could double the payout tomorrow and still be right around my 50% safety line.

Now, with construction growth set to pick up as interest rates move lower (if a little more slowly than previously expected), we’re likely to see the payout keep accelerating, taking the share price up with it. That makes now a terrific time to buy and … wait for it … lock in your shot at more upside.

The Dividend Magnet: Our Roadmap to Surging “Trump 2.0” Profits

One thing has held true no matter who is in office or what interest rates are doing: A rising dividend is the No. 1 (and 2 and 3!) driver of share prices.

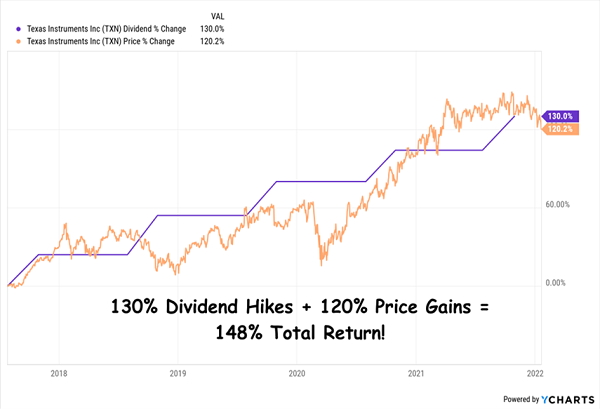

I can show you chart after chart after chart of how soaring dividends have delivered big price gains for us in the past. Like with Texas Instruments (TXN), whose payout soared 130% during our holding period, driving the stock up 120% as it did:

TXN’s Dividend Magnet Fires Up

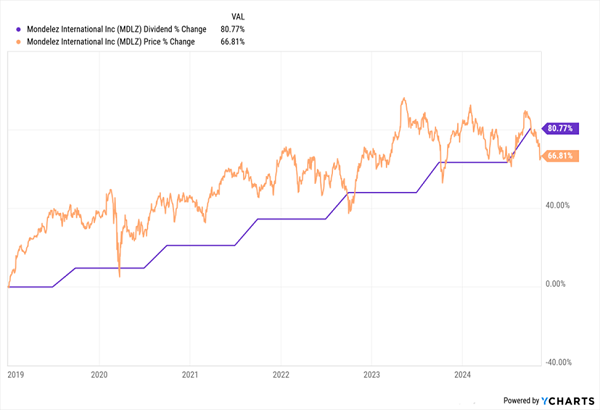

Or Mondelez International (MDLZ), whose 81% dividend growth inflated its share price 67%:

MDLZ’s Dividend Magnet Drives Steady Gains in All Market Weather

Now I’ve zeroed in on 5 stocks I see as the next Dividend Magnet winners. They’re my top picks for the fastest-growing payouts—and share prices—through 2025 and beyond.

I want to share them with you now. Simply click right here and I’ll tell you more about these 5 “Dividend Magnet” winners and give you access to a free Special Report revealing their names and tickers.