We hear a lot of chatter in the business media about productivity these days—specifically how it could decline in the US (and, by extension, hit our gains from stocks—and stock-focused CEFs).

Today we’re going to look at why this fear is overblown, and how we income investors can profit—and collect a 6.7% dividend at a 13% discount—off that disconnect.

US productivity, for its part, rises by about 2% on average per year. As we discussed a couple weeks back, the S&P 500 has posted a 10.4% annualized gain since the late 1980s, and we can say that rising productivity accounts for about a fifth of that, so about a 2% gain in stocks on an annualized basis.

Before we go further, we should spell out what we mean by productivity. The Bureau of Labor Statistics sees it as a measure of how much more efficient private companies become due to technology improvements, economies of scale, resource allocation, labor, management and infrastructure that influence overall efficiency.

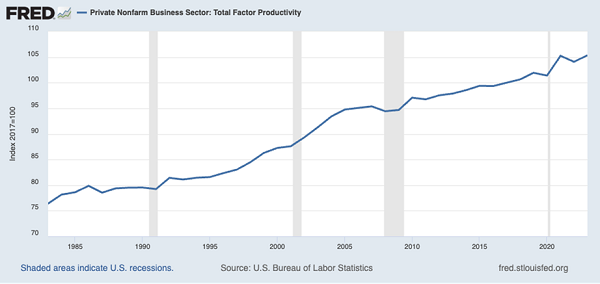

Productivity’s Long-Term Gains

Over the last 40 years, productivity has grown by 0.8% per year. (This number is lower than the 2% rate for public companies because it includes private firms). This rate has stayed steady over this 40-year period, suggesting that American companies aren’t running out of ways to make more with less.

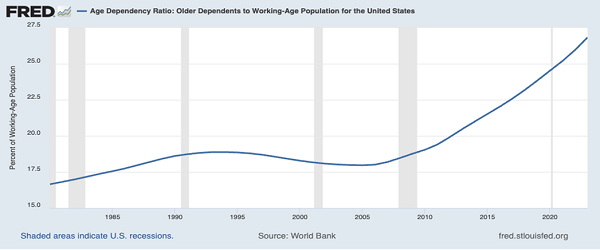

Crucially, this has happened while the US population aged at an accelerating rate.

America Gets Older, Not Less Productive

If we look at the age-dependency ratio (a ratio of people older than 64 to the working-age population, defined as people from 15 to 64), we see that it’s risen by 1.1% annualized over the last 40 years. But most of those gains happened in the last 20 years; in the first 20 years, this ratio went up by a mere 0.2% annualized.

So if an aging society were a hit to productivity, we would expect the productivity gains to slow down or even reverse in the last 20 years versus the prior 20 years by a big margin, and the data simply doesn’t tell us that.

So how much older can America get before demographics become a real concern?

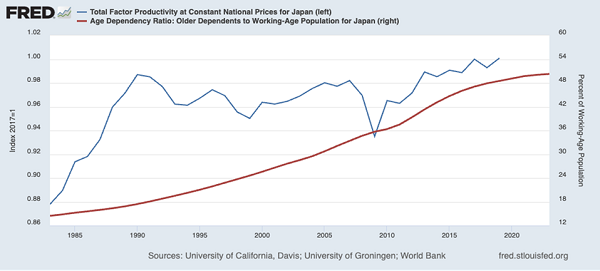

One way to think of this is to look at Japan, where the age-dependency ratio is 50, nearly double America’s current rate. In Japan, productivity has flatlined since the late 1980s as a result of that country’s economic bubble bursting. But even as its age-dependency ratio sped up in the 1990s and 2000s, Japan’s productivity didn’t collapse.

Japan Survives a Demographic Bomb

Of course, the flatline in productivity would mean that the 2% annualized gain for S&P 500 companies we noted as being driven by productivity gains above would vanish, lowering stock returns. So maybe we aren’t out of the woods yet?

There’s just one problem with this conclusion: The flatlining in productivity started when Japan’s old-age dependency ratio was two-thirds what it is in America today, at the level the US saw in 1980.

So it clearly wasn’t demographics that caused this productivity drop in Japan. And, in fact, if we zoom out, we quickly see the issue: From 1954 to 1990, Japan’s productivity across all sectors grew at an annualized 2% per year, and from 1954 to today it’s grown by 1.0%, still ahead of America’s 0.8% rate!

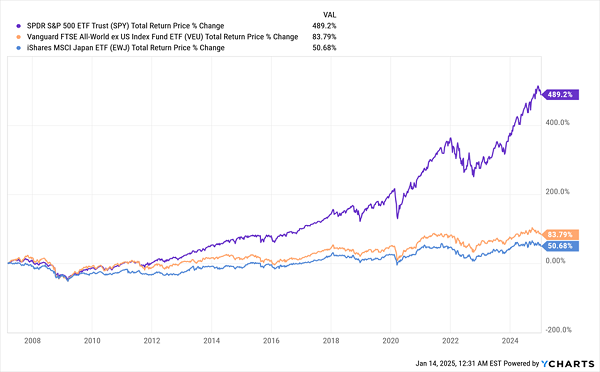

If you know your history, you can see what’s happening here: The after-effects of World War II and the demographics of that period were a lot different from today’s world, which is why extrapolating productivity trends from the ratio of old to young just doesn’t make sense. There are more important factors at play today, like technological gains, business regulation and whether public firms are incentivized to keep passing on their earnings to shareholders.

America has outrun both Japan and the rest of the world on all of these factors, as we can see from this chart of the gains in benchmark index funds for the S&P 500 (in purple), global stocks, excluding America (in orange) and Japanese stocks (in blue).

US Stocks Remain the World’s Top Performers

Considering this, the current pause in stock-market gains we’ve seen in 2025 so far is a blessing and an opportunity. For those who’ve been out of the market out of fear that the recovery of the last two years is played out, the mostly flat movement of the S&P 500 over the last month allows some time to jump back in.

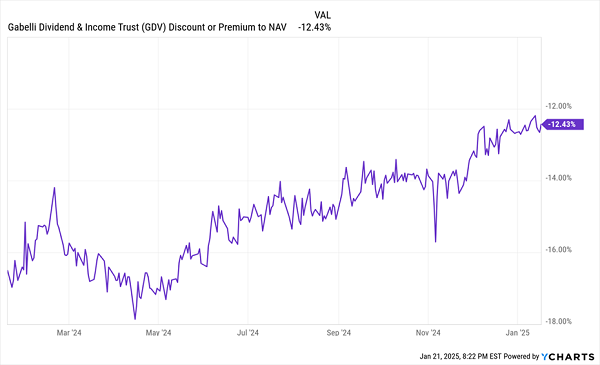

It’s also creating an opportunity to compound this potential in some high-quality stock-focused CEFs like the 6.7%-yielding Gabelli Dividend & Income Trust (GDV), whose discount to net asset value (NAV, or the value of the stocks it holds) has been narrowing, while still remaining attractive, at around 13%:

A Wide Discount—With Momentum

GDV has been oversold for a while, and investors realized this last year and started to bid its discount up from the near-18% level to where it is today.

However, the fund remains much cheaper than the average 6.6% discount for all equity CEFs and is focused on high-quality US companies like American Express (AXP), Mastercard (MA) and JPMorgan Chase (JPM), its fund’s top-three holdings.

Plus, because of GDV’s deep discount, the yield on its NAV (as opposed to the discounted market price) comes in at 5.9%. That’s significantly below the 6.7% yield on market price and is much less than the fund’s 7.4% annualized total NAV returns over the last decade.

4 MORE CEFs to Profit From Overdone Productivity Fears (Yielding 9.8%+)

GDV is a smartly run fund, and it’s trading at a solid discount, but its 6.7% yield isn’t enough to get our hearts racing, especially when you consider that the typical CEF yields around 8% as I write this.

And many yield a lot more.

Like the 9.8% average dividend paid by the 4 other CEFs I’m pounding the table on now. What’s more, their deep discounts give us a “head start” as stocks move higher, as I see them disappearing in the next year, catapulting these 4 funds’ prices higher.

In all, I see 20%+ price gains from these funds, to go along with their 9.8% average dividends!