Few things ease financial worry like knowing you can walk away from work anytime you want.

Closed-end funds (CEFs) give us just that kind of security—and we talk about that a lot in my weekly articles and in my CEF Insider service. With yields of 8%, 9% and more, CEFs generate huge payouts that could let you retire earlier than you think.

It’s such a powerful—and overlooked—way to invest that it’s worth revisiting again today. We’ll color our discussion by looking at how some typical American retirees could retire with CEFs.

And we’re going to work in some real-life numbers, too.

I can’t stress enough that we’re not doing anything exotic to grab these yields: One of these three CEFs invests in S&P 500 stocks. The others are almost as familiar, holding corporate bonds and publicly traded real estate investment trusts (REITs).

More on these funds in a moment. First, let’s look at some real figures to see how much income investors could potentially book from CEFs.

Retirees Are Doing Better Than You Think (and Could Do Better Still)

First, let’s get some data about the net worth of the average retiree. Fortunately, the Federal Reserve regularly collects this information.

The numbers say something startling: The average retiree is doing well, with the 65-to-74-year-old cohort sporting an average net worth of $1.79 million in 2022, with some of that being in their primary residence. Since that was a lousy year for markets, that net worth is probably higher now.

Of course, not everyone is doing well. Because many haven’t been able to save as much as the top tier, the median retiree has a net worth of about $409,900. This means they need to rely on Social Security.

However, even a less-wealthy retiree could have a comfortable retirement with the three funds I’m about to show you—and we’ll get to those in just a moment.

But first, let’s talk about our average retiree, with that $1.79-million net worth.

They probably have at least some of their wealth in S&P 500 index funds, which yield around 1.3%. That translates into $2,000 in monthly income if they had the full $1.79 million available to invest (an assumption we’ll make as we move through this article).

They could get much more through the three funds we’ll discuss next—all of which will be familiar to CEF Insider readers.

“Financial Freedom” Buy No. 1: Adams Diversified Equity Fund (ADX)

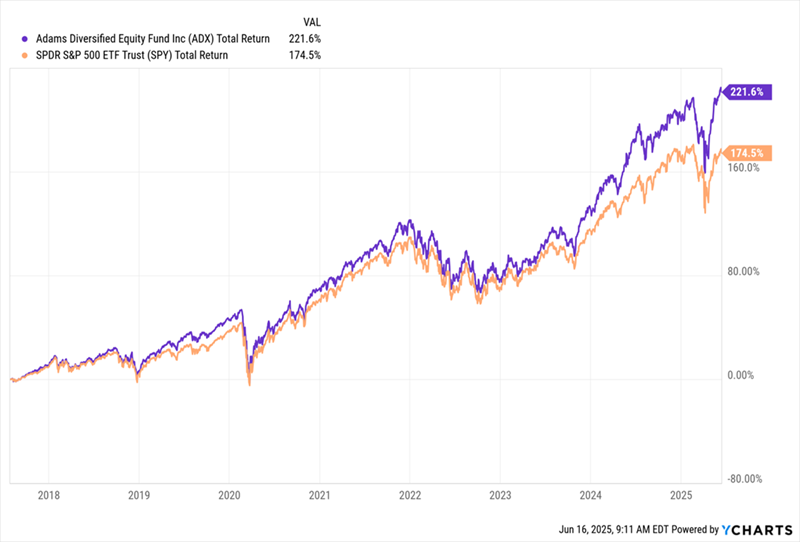

The Adams Diversified Equity Fund (ADX) yields 8.8% and holds well-known stocks like Apple (AAPL), Microsoft (MSFT) and Visa (V). It’s also one of the world’s oldest funds, having launched in 1929, days before that year’s market crash.

Moreover, ADX has a history of strong returns: It has crushed the S&P 500 for decades, including our holding period at CEF Insider, which began nearly eight years ago, on July 28, 2017.

ADX Demolishes the Index, Returns 222% for CEF Insider

Despite that outperformance, ADX has a 7.5% discount to NAV that has been closing since the middle of 2024 but still remains quite wide. One other thing to bear in mind: ADX commits to paying 8% of NAV out per year as dividends, paid quarterly, so the payout does float as its portfolio value fluctuates.

“Financial Freedom” Buy No. 2: Nuveen Core Plus Impact Fund (NPCT)

Next is the Nuveen Core Plus Impact Fund (NPCT), a 12.2%-yielding corporate-bond fund. Its discount has been shrinking in the last few years, from over 15% to around 4.1% today.

NPCT Gets Attention

Again, the portfolio shows why: NPCT’s managers have picked up bonds from low-risk issuers, including utilities like Brooklyn Union Gas and financial institutions like Standard Chartered and PNC Financial Services Group.

More importantly, they’ve taken advantage of higher interest rates to lock in high-yielding bonds with long durations, with an average leverage-adjusted duration of 8.4 years. (This measure takes the effect of the fund’s borrowing into account, making it a more accurate description of rate sensitivity.)

That stands to pay off when rates decline, cutting yields on newly issued bonds and boosting the value of already-issued, higher-yielding bonds like the ones NPCT owns.

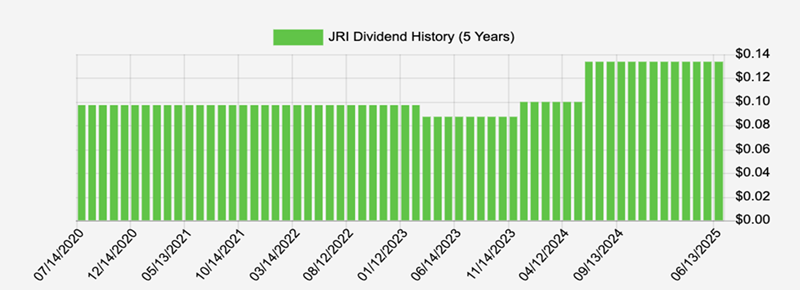

“Financial Freedom” Buy No. 3: Nuveen Real Asset Income and Growth Fund (JRI)

Let’s wrap with the 12.3%-yielding Nuveen Real Asset Income and Growth Fund (JRI). Its portfolio features powerhouse REITs like shopping-mall landlord Simon Property Group (SPG) and Omega Healthcare Investors (OHI), which profits from the aging population by financing assisted-living and skilled-nursing facilities.

That huge dividend has a history of growth, too:

JRI’s Rising Payout

Source: Income Calendar

The fund has seen its discount shrink to 3.1% from the 15% level it was at in mid-2023, even after the pandemic hit REITs hard, and that discount continues to have upward momentum.

An 11%-Paying “Mini-Portfolio” That Pays the Bills (and Then Some)

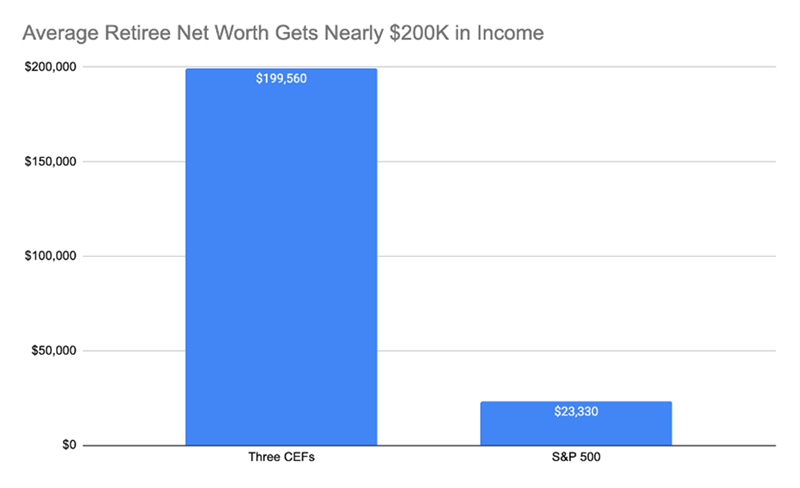

Put those three CEFs together and you have a “mini-portfolio” yielding 11.1% on average. Here’s how that income stream looks with $1.79 million invested.

Source: CEF Insider

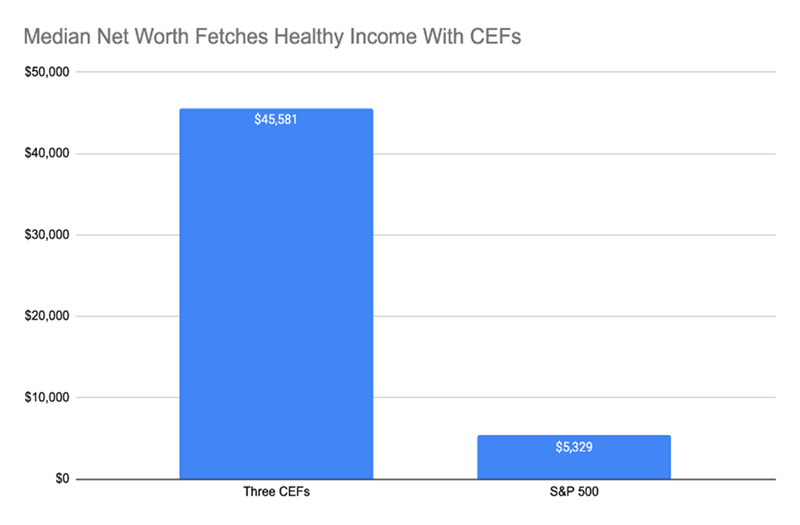

As you can see, with these CEFs, the average retiree’s net worth could fetch around $200,000 in annual income, or $16,630 per month. What about the median, though? Well, their $409,900 would bring in a nice income stream, too.

Source: CEF Insider

Now we’ve got $3,798 per month, a smidge higher than the median income for US workers (which is $3,518 per month, again per the Federal Reserve). Add the median $2,000 per month in Social Security benefits, and that turns into nearly $6,000 a month.

Retire? Keep Working? It’s Your Call With These 4 Reliable 9.5% Payers

The beautiful thing about CEFs is they’re open to everybody—not just the rich (though these incredible income funds are certainly favorites of the billionaire set).

CEFs aren’t just for retirees, either. Got a job you love? That’s fine—keep at it and use your CEF dividends to reno your home, take more time off or help out the kids. It’s all up to you.

That’s the very definition of financial freedom.

One thing I do urge you to do, though, is consider my top 4 CEFs to buy now for the core of your plan. These 4 funds offer huge 9.5% dividends and discounts poised to slingshot their prices higher as they vanish.

This is, quite frankly, the kind of investment strategy everyone should follow. But few people do, preferring to stick with familiar S&P 500 names instead.

Let’s not stay chained to a cubicle like these folks. Click here and I’ll walk you through these 4 high-yielding funds and give you a free Special Report revealing their names and tickers.