Let’s talk about energy dividends because, well, you know why. But let’s not chase the headlines.

Let’s focus on energy “toll collectors” that will make money regardless of tomorrow’s geopolitical landscape. Steady cash flows support these 4.2% to 9.5% yields.

This runs counter to the outlook for exploration and production companies, as well as equipment and service providers, which have profits that are tightly bound to the price of energy commodities. These stock prices follow crude oil movements too closely.

Energy infrastructure companies are calmer plays. Companies that own and operate pipelines, processing plants and storage facilities aren’t nearly as reliant on energy prices—they just take a cut whenever oil, natural gas, nat-gas liquids, etc., flow through their various assets. Hence “toll collectors.”

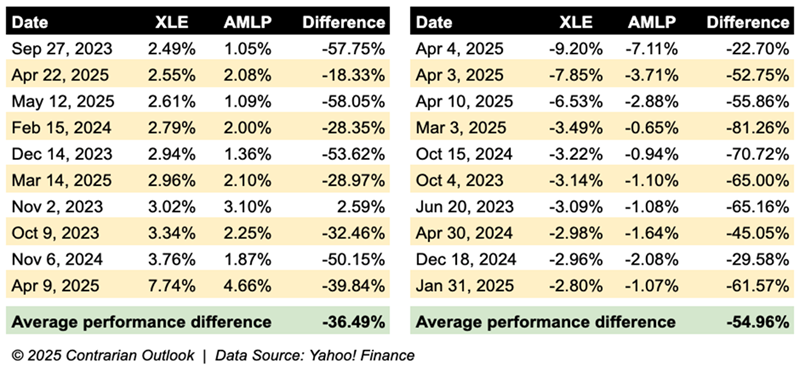

Just look at how differently an energy infrastructure master limited partnership ETF (AMLP) acts compared to a broad basket of energy stocks (XLE).

These tables illustrate how both ETFs performed during the XLE’s 10 biggest single-day gains and 10 biggest single-day losses of the past two years. And as we can see, AMLP is significantly less volatile.

Energy Infrastructure Keeps Calm and Carries On

Better still? Energy infrastructure actually tends to go with the flow a little bit more during rallies, but slinks away from the crowd during downturns!

A good example of this kind of stock is Kinder Morgan (KMI, 4.2% yield), a blue-chip energy payer that boasts 79,000 miles of pipelines transporting natural gas, crude oil, carbon dioxide and other products. A huge 40% of natural gas produced in the U.S. flows through Kinder’s systems—to 139 company-owned terminals storing petroleum products, chemicals and renewables.

At 4%-plus, KMI’s yield is good, not great—but it could be great over time. Kinder Morgan slashed its dividend by 75% back in December 2015 amid one of the worst oil price crashes in years. But since 2018, KMI has been restoring the dividend at a roughly 11% annual rate. Not to mention, at a beta of 0.75, it’s a quarter less volatile than the broader market and less shaky than energy stocks as a group.

Plains All American Pipeline LP (PAA, 8.2% yield) is a juggernaut in the space. Its operations include 20,000 miles of crude oil and NGL pipelines and gathering systems, 170 million barrels of storage capacity, 5,400 crude oil and NGL railcars, and 2,300 trucks and trailers.

PAA’s most recent results showed strength in NGLs; pipeline volumes were up 9% and fractionation volumes up 23%. But we’d want to keep an eye on America’s continued trade tiff with China, where chemical manufacturers use NGLs as feedstock.

Plains’ distribution history is concerning, too. Plains cut its payout three times in five years: 2016, 2017, and 2020. PAA did announce a 20% hike to its distribution earlier this year to 38 cents per unit, putting it back above pre-COVID levels. However, Plains has demonstrated that it’s willing to stretch on its distribution, then pull the rug if it needs to.

Plains’ Recent Hikes Are Admirable, But Are They Dependable?

Another big energy infrastructure company worth a second glance is Western Midstream Partners LP (WES, 9.5% yield), which manages 21 gathering systems, 69 processing and treating facilities, and more than 14,373 miles of pipeline spread across seven natural-gas pipelines and 12 crude oil/NGL pipelines. It does this on behalf of Occidental Petroleum (OXY), which owns nearly 45% of the company and manages WES via its subsidiary, Western Midstream Operating LP.

Western also halved its payout in 2020, but unlike PAA, WES’s cut was an isolated incident.

In early April, I mentioned that I was looking forward to Western Midstream’s mid-month earnings report, hopeful that it would continue its distribution growth. Mixed news there. On the one hand, it did raise the distribution by 4% to 91 cents per unit, good for a yield north of 9%. However, that’s a massive slowdown compared to the 50%-plus raise it authorized a year before. As I mentioned, its Pathfinder Pipeline project, among several others, are expected to inflate its capital expenditures, which could keep distribution-growth minimal for the next few years.

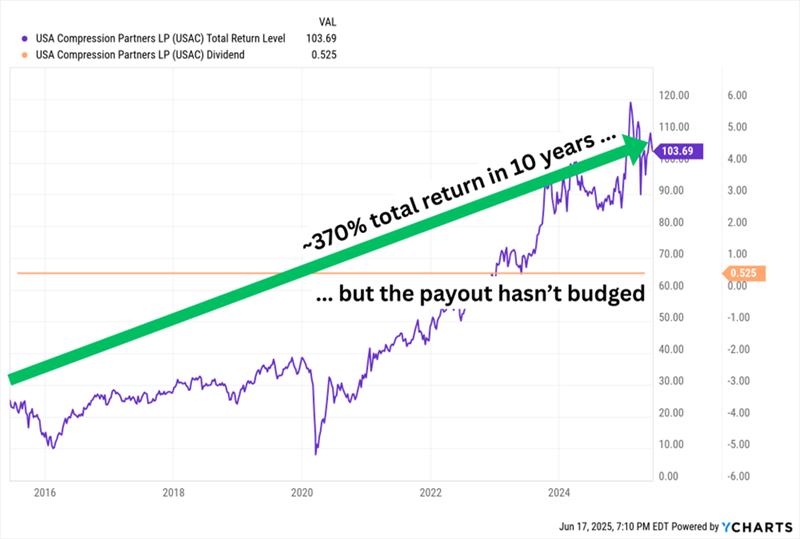

USA Compression Partners LP (USAC, 8.4% yield), which has been one of the more productive MLPs of the past few years, is a niche player in the space. It provides natural gas compression services, including designing, operating, servicing and repairing its compression units, and maintaining related support inventory and equipment.

USAC’s most noteworthy feature, however, is long initial contracts and high barriers to get out of those contracts. That produces an extremely high level of stability that shows up in its performance—its five-year beta is a very low 0.4, suggesting it’s less than half as volatile as the broader market.

Heavy investments into the business are great for growth, but they prevent USAC from making much of a dent in its debt, and from paying unitholders more. The distribution has been stuck at 52.5 cents quarterly for a decade.

Something Has to Give. Will It Be the Dividend … Or USAC’s Price?

There’s also the option of buying several MLPs at once with a fund.

While I usually prefer closed-end funds (CEFs) because they squeeze out much more yield than comparable ETFs can, the Alerian MLP ETF (AMLP, 7.9% yield) is anything but stingy. It holds a tight 13 stocks right now, reflecting what is a pretty narrow world of MLPs. Still, it’s easy diversification across numerous energy and asset types, and it pays out nearly 8%.

A Fully Paid Retirement for Just $500,000?

Yields around the 8% mark are fantastic—with that level of income, we can retire on dividends alone.

But if we really want to do right by ourselves in retirement, we want to receive that income at the exact same frequency as we pay all of our liabilities:

Monthly.

That’s the core principle behind my 8% Monthly Payer Portfolio: A group of generous stocks and funds that pay us enough to live on dividends alone—without ever needing to sell a single share to generate cash.

The math on this portfolio is easy to follow:

- A $500,000 nest egg can earn $40,000—depending on where you live, that could be enough for a fully paid retirement on its own.

- You can generate a $48,000 annual dividend “salary” from a $600,000 nest egg.

- And if you have managed to stow away a cool million bucks to work with, the 8% Monthly Payer Portfolio would pay you an equally cool $80,000 in dividend income every year.

Better still? You’d be cashing dividend checks not annually, not quarterly, but each and every month.

No “lumpy” payouts. No complex dividend calendars. No dumping money into certain stocks because you’re getting underpaid every third month.

Just paydays as smooth as when you were collecting a paycheck!

Don’t miss out on these terrific income plays while you can still get in at bargain prices. Click here for all the details, and turn your portfolio into a monthly dividend machine.