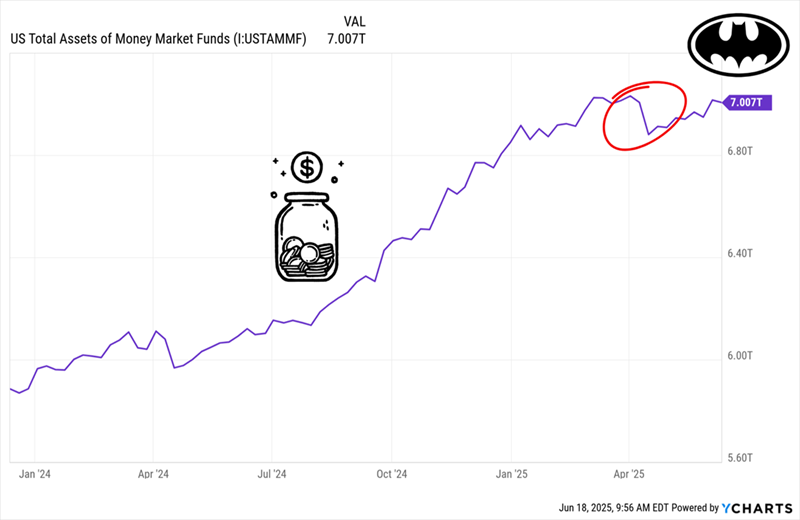

Stocks—especially dividend stocks—have every reason to shoot higher from here. In fact, they have 7 trillion reasons.

That’s how much Americans have parked in money-market funds. But a chunk of that is about to shake loose. When it does, I see it piling into top dividend payers (and growers)—including the three we’ll discuss below.

Investors Wait for the Stock-Market “Bat Signal”

Before we get to that, the chart above is worth a look. Starting last summer, pre-election fears sent investors piling into money-market funds, pushing assets past $7 trillion.

Then something strange happened: They pulled cash out of these funds after the “Liberation Day” tariffs were announced. It seems many folks really did listen to President Trump’s tweet (Truth?) to buy the dip!

But look to the right: You can also see that cash hoard building once more. That’s our cue, because mainstream investors’ fears, once again, are overwrought.

The current “wall of worry” the market is climbing goes like this: The government’s deficit is exploding, with the Congressional Budget Office projecting a $1.9-trillion shortfall for fiscal 2025.

Then there’s the “Big Beautiful Bill”: Over the next decade, it’ll tack $2.8 trillion onto Uncle Sam’s deficits, again according to the CBO. That means higher Treasury yields—and higher interest rates (and with them debt-servicing costs for the government). That drives debt higher still. An economic “doom loop!”

We “second-level” thinkers see things differently. Buried in the angst is a “trigger” set to tip a chunk of that $7 trillion into our favorite dividend payers.

Bessent Vs. the 10-Year Treasury

In recent articles, we’ve talked about Treasury Secretary Scott Bessent and Jay Powell working together to “paper over” Uncle Sam’s debt problem.

Wait, Jay? Who Trump just called “a stupid person”?

Trump’s low opinion of Powell isn’t really news. In Trump 1.0 he called the woebegone Fed chair an “enemy.” More recently, he’s pegged him with the “Too Late” nickname.

No doubt the poor man is counting the days till his term ends in May 2026!

But the real “truth” is that Jay isn’t really a priority for Bessent and Trump. Bessent has straight-out said he’s more focused on the “long” end of the yield curve set by the 10-year Treasury rate, benchmark for consumer and business loans.

He’s going around Powell, in other words. And he’s doing it by leaning on short-term debt issuance. That cuts Treasury demand, driving up the “long bond’s” price and cutting its yield.

But Powell isn’t entirely out of the picture here. While he’s holding the line on rates, the Fed has quietly stepped up its monthly bond buying by $20 billion! That’s another anchor dragging down bond yields.

And don’t forget, the midterms draw nearer by the day. Trump and Bessent do not want to head into them with a recession raging. They’ll pull out all the stops.

3 “Front-Runner” Dividends Paying Up to 8%

Now, about that trigger I mentioned earlier: As rates fall, yields on money-market funds and Treasuries will fall with them. That’ll “smoke out” a slice of that $7 trillion—and send it searching for income.

When it does, I expect these three smartly run dividend plays to be on their lists.

From Municipal Bonds …

First up, the Nuveen Quality Municipal Income Fund (NAD), a closed-end fund (CEF) trading at a 4.9% discount to net asset value (NAV) as I write this.

That’s CEF-speak for saying that we can buy its portfolio of bonds, issued by state and local governments to fund infrastructure projects, for 95 cents on the dollar. Those include bonds from the Orlando Aviation Authority, New York Transit Development Corp. and Colorado’s E-470 Highway Authority.

That’s a sweet deal for us, especially since municipal bond income is tax-free for most Americans (though there has been concern about the tax break’s future, especially on newly issued “private activity bonds,” or those used to fund projects partly or wholly owned by private firms, as Uncle Sam looks under all the couch cushions to cut the deficit).

That concern (which hasn’t yet materialized in legislation) has led to a rash of muni-bond issuances, keeping a lid on the market. That’s another reason to buy at today’s discount and start tapping this fund’s 8.1% dividend, which is likely worth a lot more to you on a taxable-equivalent basis, depending on your tax bracket.

… To Our Favorite “Bond Proxies” …

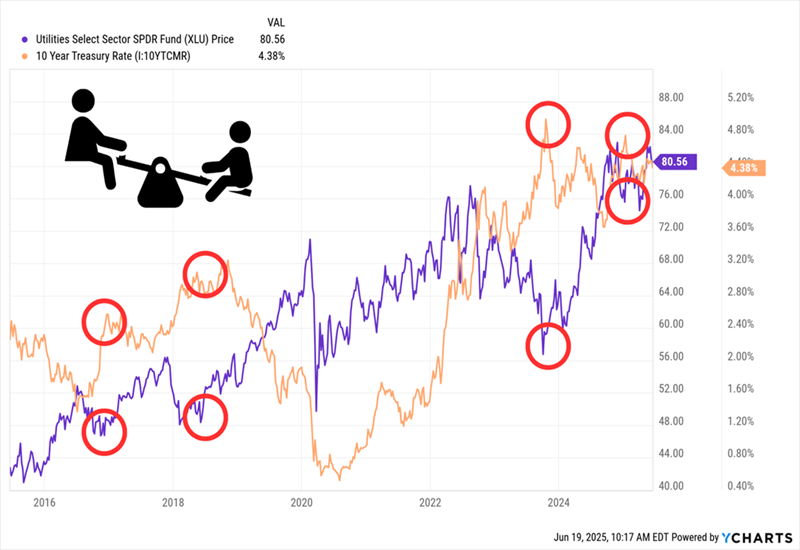

Utilities are another smart play as rates decline, as their prices rise as bond yields fall. You can see that reflected in the benchmark Utilities Select Sector SPDR Fund (XLU):

The Rate/Utility Teeter-Totter

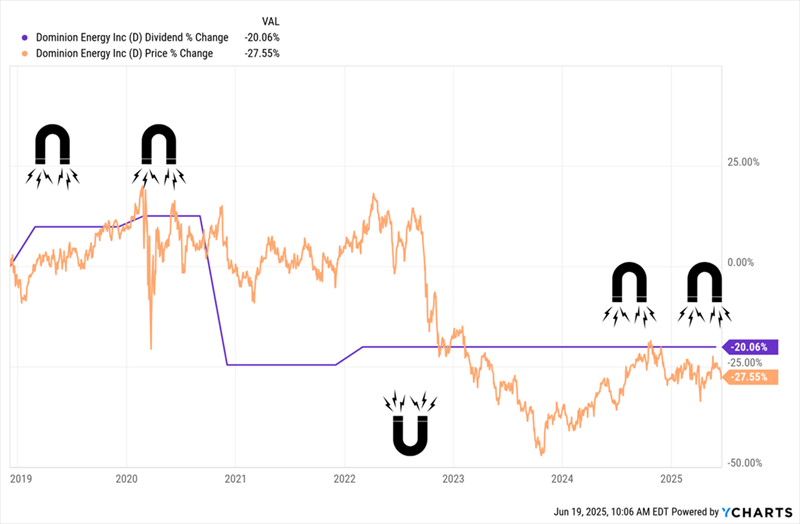

We can do better than XLU’s 2.8% yield, though, with one of the biggest utilities out there: Virginia-based Dominion Energy (D), which yields 4.9% and whose stock is still in the doghouse after management cut the payout way back in 2020.

While D has resumed hikes, the market hasn’t forgiven it—yet. You can see below how the stock’s “Dividend Magnet” has dragged it lower after the cut (with a bit of a delayed reaction) and is now poised to pull it back up.

D Shares Set for a Rebound

That drop is in spite of the fact that D’s Virginia domicile perfectly places it to supply AI’s bottomless thirst for power, with the so-called “Data Center Alley” located near Ashburn, in Loudon County. Dominion’s forward price-to-earnings ratio of 16, well below its five-year average of 19.2, underscores the deal on the table here.

… And Another “Overdue” Dividend Magnet

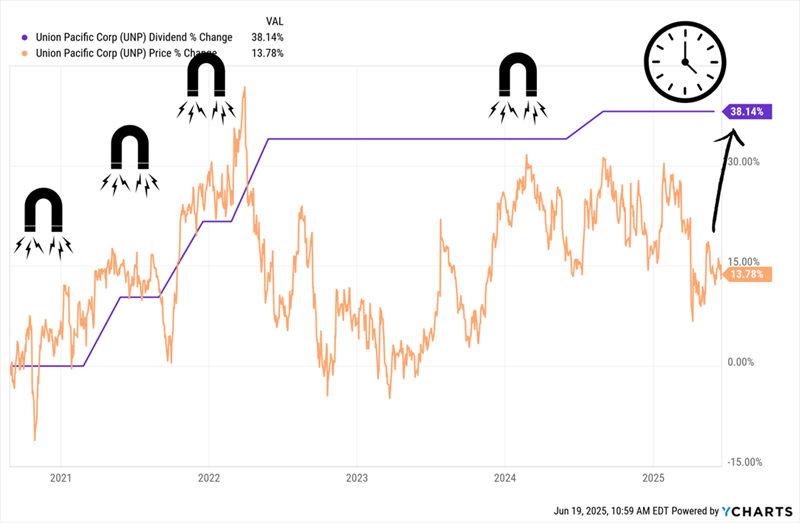

Finally, Union Pacific (UNP) involves a little more risk than our two other picks and starts us off with a lower yield: 2.4%. That’s why I’ve slotted it into our No. 3 spot.

UNP’s network spans 23 western states, connects to key Pacific ports and stretches into Mexico. The stock is down around 2.4% this year, on tariff fears.

But there are plenty of reasons to hope for a turnaround. For one, Canada and the US are in deep discussions—and Prime Minister Mark Carney has slapped a 30-day timeline on those talks to “focus minds.”

There are also talks around cutting or removing tariffs on Mexican steel, another plus as the North American neighbors get set to renegotiate the USMCA next year. Those talks could go better than expected, coming just a few months ahead of the midterms.

Then there’s UNP’s “Dividend Magnet.” As you can see below, the payout’s growth has been slow over the last few years. But the stock is still well behind the payout’s meager gains and is overdue to close the gap.

UNP’s Dividend and Share Price Come Unhooked (for Now)

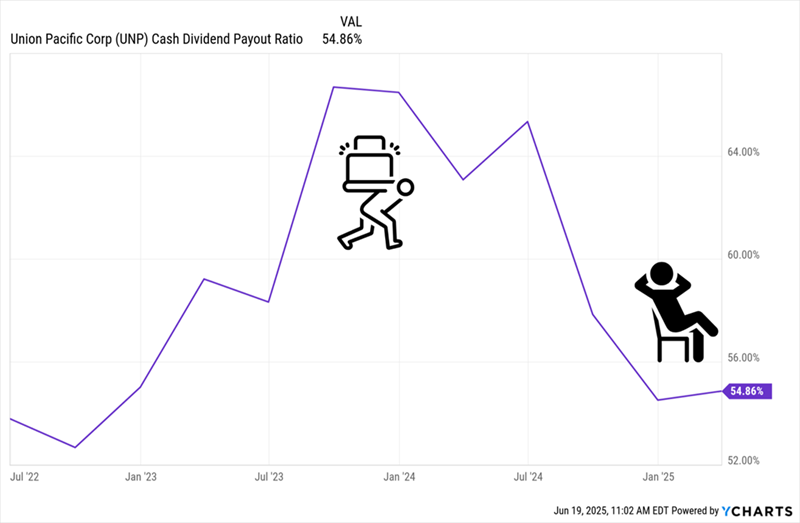

Meantime, UNP pays a comfortable 55% of its last 12 months of free cash flow (FCF) as dividends, down sharply from its peak of around 66% in the third quarter of 2023.

UNP’s “Dividend Load” Lightens

That puts faster payout growth on the table, as do lower interest rates and easing trade tensions. A couple nice payout hikes would, in turn, grab investors’ attention, especially if they come as a “cash wave” flows out of money-market funds. Meantime, we can pocket already high 4.9%+ yields from NAD and Dominion.

This 11% Dividend Will Crush It When Money-Market Funds Drain

Let’s get even more direct: When the dam breaks on that $7 trillion and rates inevitably drop, we’ll go straight to the heart of the matter and buy bonds.

Not Treasury bonds, though. No way. They don’t pay enough now, and their yields are only set to go lower.

Instead we’re going to corporate bonds—and to one bond fund in particular that’s run by a manager so successful he’s taken home the coveted Fixed Income Manager of the Year title. His fund pays a massive 11% dividend and pays dividends monthly.

So if you buy today, you’ll be collecting your first big dividend check—on your way to 11% in cash in your first year—in just weeks!

And that doesn’t include the upside I see as this fund pulls in income investors with promises of huge, regular, reliable and monthly payouts.

Now is the time to buy this 11%-paying cash machine. Click here and I’ll tell you more about it and give you a free Special Report revealing its name and ticker.