“Programmer.”

My wife nailed it as we stepped into the open house, staring into the front room labeled “home office.” Shoes off, respecting the homeowners still living there.

“They’re hoping for a rentback,” explained the realtor. “The couple has to move out of town for work.”

Ah, another casualty of the return-to-office mandate! Back to the Bay Area for these two. They’re far from alone. Major cities—Boston, New York, San Francisco—are shaking off five years of downtown rust, preparing for commuters back four or more days each week.

Even here in Sacramento, I had to battle morning traffic this week for the first time in more than five years. My drive from dropping off kids just outside the city (at science camp) back into the city (to my office) had me feeling like it was 2019.

Which is why we’re talking about undervalued “return to office” REIT dividends up to 14.4% today.

Office REITs were left for dead in the shredder. COVID sent whole offices into their homes, and it looked like these landlords were done—until bosses started telling workers to get back to the office!

This isn’t a free pass to every office space owner. Consider that just last month, Sunbelt office-space owner Piedmont Realty Trust (PDM, NO yield) completely halted its dividend payments for the first time in company history, and CEO Brent Smith said he didn’t expect for dividends to return until at least late 2026. (But even then, there’s a silver lining for office retailers: While PDM’s cash flows were weak, it was preserving cash for tenant buildouts amid a frenzy of leasing activity.)

Let’s look at five other office REITs with better prospects—and more yields (up to nearly 14%).

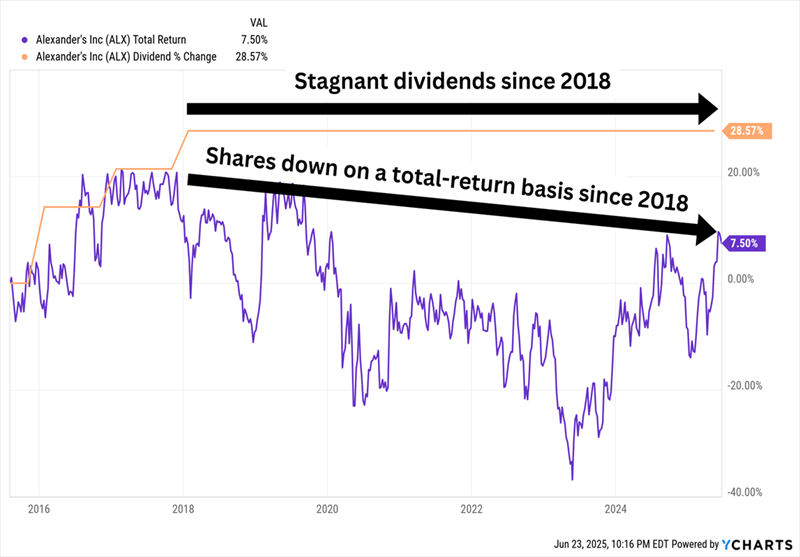

Alexander’s (ALX, 8.2% yield) has one of the most spartan property rosters you’ll ever see: just five properties in the New York City metropolitan area. It’s actually managed by the much larger Vornado Realty Trust (VNO), which is important to know because it squeezes annual management fees out of several of those properties and is also entitled to development fees when applicable.

ALX, to be honest, has a lot of things going against it. Five properties isn’t exactly diversified to start with, but also understand that it has high single-tenant risk: Bloomberg accounted for nearly 60% of Alexander’s rental revenue during Q1 2025, up from about 50% in the year-ago quarter.

“No other tenant accounted for more than 10% of our rental revenues,” reads Alexander’s first-quarter Form 10-Q. “If we were to lose Bloomberg as a tenant, or if Bloomberg were to be unable to fulfill its obligations under its lease, it would adversely affect our results of operations and financial condition.”

Almost bafflingly, ALX has been one of the most resilient office REITs in the post-pandemic era, boasting about 30% in total returns over the past five years (versus losses for most of its peers) and keeping its dividend intact throughout COVID.

Unfortunately, that dividend, while generous, also hasn’t grown in a long time.

No Dividend Growth, No “Dividend Magnet”

The main reason is coverage issues. In 2023, it paid $18 per share in dividends against $15.80 in funds from operations (FFO) per share. In 2024, it paid the same $18 against an even lower $15.19 in FFO. And ALX paid $4.50 per share in dividends during 2025’s first quarter against just $4.06 in FFO. More worrying still: At the start of 2025, the company owed $502 million in debt repayments versus about $340 million in cash holdings.

Easterly Government Properties (DEA, 8.1% yield) is a highly specialized office REIT boasting 100 properties, 92 of which are leased out to U.S. government tenant agencies such as Veterans Affairs, the FBI, and the Drug Enforcement Administration, with the remaining handful leased primarily to state or local government tenants or private tenants. Its buildings go beyond traditional cubicle farms, spanning outpatient facilities, warehouses, courthouses, labs, even built-to-purpose properties.

Still, if a government REIT sounds exactly like the kind of company that “DOGE” would drag down, you’d be right. Back in March, I highlighted some REIT studs and duds, and DEA was solidly in the latter camp:

“While Easterly might defy the odds and not die by DOGE’s sword, this is a company that already had a longstanding problem consistently growing FFO. Hard pass on this double-digit divvie.”

Readers who failed to heed that warning are now sitting on a single-digit divvie. Just a couple weeks later, Easterly slashed its dividend by roughly a third, from 26.5 cents per share to 18 cents per share. It also announced a 1-for-2.5 reverse stock split to get its shares back above $10 per share; as of the stock split, that dividend becomes 45 cents per share.

Investors at least have a harder decision now than they did before. A massive dividend cut, especially one so recent, is a major strike against Easterly. But the dividend now sits at a much more affordable 60% of core FFO estimates. Unfortunately, despite losing half its value over the past five years, including a double-digit drop in 2025, we’re still paying a fair-at-best 13 times 2025 FFO estimates—all while DOGE and government cutbacks continue to cast a shadow over DEA’s tenants.

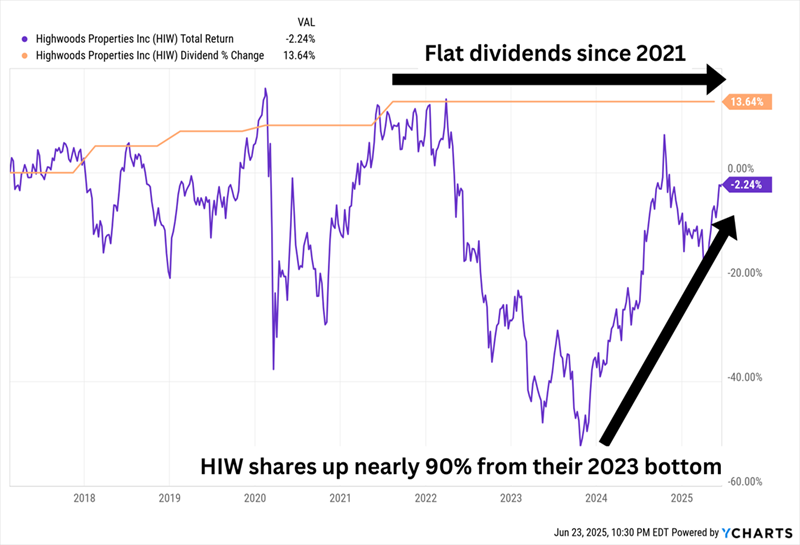

We’ll find a smaller but safer-looking payout from Highwoods Properties (HIW, 6.4% yield), which owns 26.7 million square feet of office space with more than 95% exposure to Sunbelt markets such as Dallas, Orlando, Atlanta, Nashville and Charlotte.

Put differently: HIW is rooted in cities with higher-than-the-national-average population growth, rent growth and office employment growth. It also boasts extremely low leverage compared to the space, and shares are decently valued at 9 times FFO estimates.

Like ALX, Highwoods never cut its payout during COVID, but you could argue it should have raised it since then—dividend coverage is extremely generous, with an FFO payout ratio of just 60% based on 2025 estimates.

A Long-Awaited Payout Hike Could Be the Breakout Catalyst HIW Needs

Some readers might not be ready to fully dive into office REITs but still want a taste. That’s where hybrid REITs come in.

Take American Assets Trust (AAT, 6.7% yield), for instance. It’s a modestly sized REIT at just 31 buildings across the Pacific Coast, Hawaii and Texas, but those buildings include 4.1 million square feet of office space, 2.5 million square feet of retail space, 2,302 multifamily units, and 369 hotel suites. Still, office space is the largest chunk of cash net operating income (NOI), at just over half.

AAT’s dividend was a COVID victim, cut from 30 cents per share to 20 cents in 2020. Dividend growth resumed just two quarters later, though, and the stock was back to 30 cents by the back half of 2021. Better still? The payout has grown in every year since—glacially, but it’s the right direction.

Those dividends represent just 70% of projected 2025 FFO, and the stock trades at roughly 10 times those estimates.

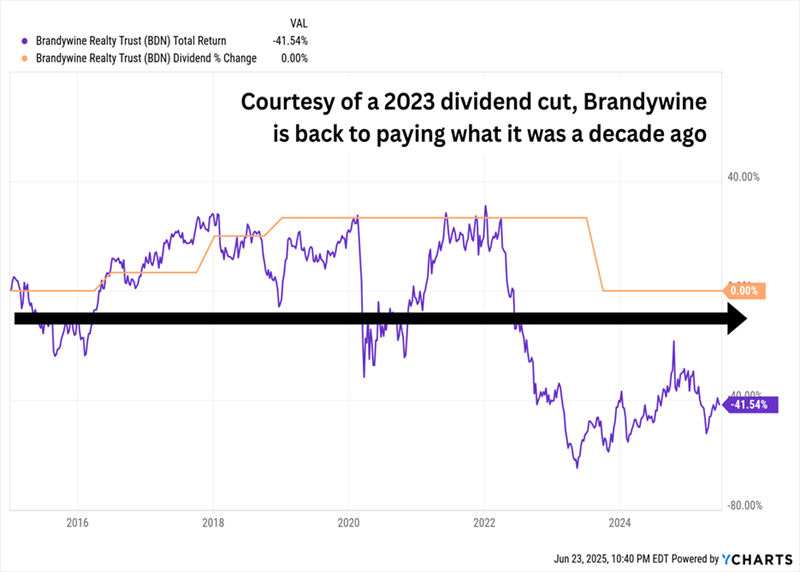

Brandywine Realty Trust (BDN, 14.4% yield) is another hybrid REIT with 64 properties and a similarly thick office concentration, but it’s trying to change that—projected NOI based on its current pipeline is expected to be 42% office, 32% life science and 26% residential. It’s also extremely focused on two areas: greater Philadelphia (77% of NOI) and Austin, Texas (15%).

I mentioned a few months ago that BDN’s dividend arrow is pointed in the wrong direction.

The Payout Is Standing Still. BDN Shares Wish They Were.

Part of the problem is that development projects are dragging Brandywine down. Some of its construction has been funded by expensive capital, and its arrangements with partners require Brandywine to recognize full interest and other costs until the projects become profitable.

I had hoped Brandywine’s latest report would inspire confidence; it did anything but. First-quarter FFO fell below expectations, “normalized” FFO was off by more than 40% year-over-year, and cash available for distribution (CAD) fell below the company’s 15-cent dividend for a third straight quarter.

This 11% “Trump 2.0 Buy” Is on Firmer Footing—And Another Big Distribution Is Coming Up Soon

Office real estate isn’t the pariah it was before, but danger still lurks around at least some of the companies in the space.

Until we see more, we’re only interested in trading the space, not so much buying and holding.

If you’re looking for high yields you can hold for the long run, however, we’re buying a different investment that delivers both high yields and solid track records.

It’s a closed-end fund (CEF), and a heralded one at that. But more importantly, it checks off a bunch of important retirement boxes in a major way:

- A huge dividend—11% at current prices!

- Monthly distributions

- A big—and highly unusual—discount in disguise!

This isn’t some vanilla index fund. This CEF is actively run by bond royalty. This fund captain has been named Fixed Income Manager of the Year by Morningstar, and he has been inducted into the Fixed Income Analysts Society Hall of Fame!

As rates fall and other income options wane, I expect this 11% payer’s discount/dividend combo to be a shiny lure for the mainstream crowd. And we have a shot at “front-running” them today.

Don’t miss this opportunity. Click here and I’ll tell you more about this incredible 11%-paying fund and how to get your FREE Special Report revealing the name, ticker and my detailed research.