It’s a trap I see investors fall into all the time: pouncing on yields that are so high as to be, frankly, absurd. Case in point: the 89% (not a typo!) yielder we’re going to talk about today.

I get where the temptation of a payout like that comes from. Inflation is sticking around. The job market? Precarious, to say the least, with AI replacing humans at an accelerating pace. Another disappointing jobs report, released on Friday, sure doesn’t help here, either.

At a time like this, an 89% annualized payout sounds like a dream, especially if you’re looking to get to (and hopefully stay in!) retirement.

I’m talking about the payout on the YieldMax Ultra Income Strategy ETF (ULTY), which we last discussed in March.

Now, as I did then, I’ve got three main beefs with this one:

- That huge 89% yield (of course), which entails a lot of risk.

- Massive investment turnover, to the tune of 717% of its average portfolio value, in just eight months!

- ULTY’s recent move from monthly to weekly payouts.

Let’s dive into that 89% yield (which is based on the annualized weekly payout for the last week of August) straight away, as it’s the number that (by far) leaps out the most.

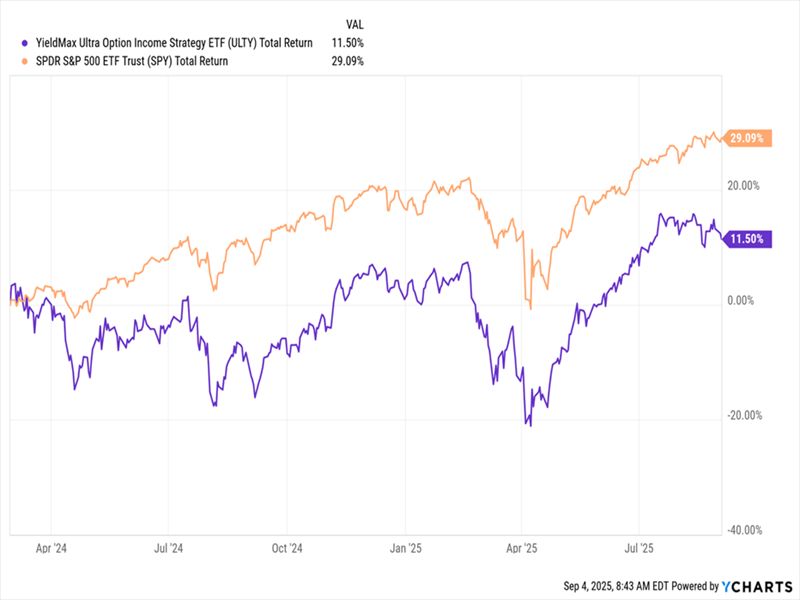

At that level, it sounds like you’re getting your whole upfront investment back in a little over a year in dividends alone. Sounds tempting, doesn’t it? By that logic, those who bought ULTY when it launched in February 2024 should have recouped their cash and then some by now, right?

Even with that huge payout, these folks have only seen an 11.5% return, as of this writing, with dividends reinvested. That’s a bit more than a third of what they’d have gotten if they just bought a plain-vanilla S&P 500 index fund!

Big Dividend Doesn’t Help ULTY Investors …

It gets worse, because as you can see in the chart, investors in ULTY (in purple above) had to endure a much more volatile ride.

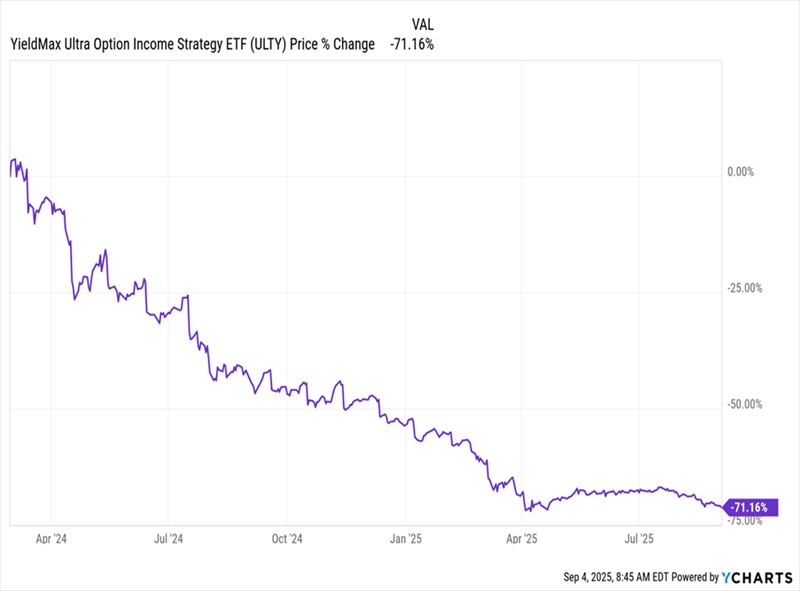

What happened here? Simply put, ULTY’s price plunged, draining off most of the return from the payout. If you strip out the dividend, the fund’s price has nosedived 71% since ULTY’s launch. That’s a big reason why it yields 89%, since yields and prices move in opposite directions.

… And Its “Price-Only” Return Has Been Brutal

This drop is especially disappointing because ULTY uses covered calls to generate income. By doing so, the fund sells investors the right to buy its stocks at a fixed date and price in the future. No matter what happens with these trades, ULTY keeps the option “premium” it charges these buyers.

Selling calls is a great way to generate income. The drawback? It can cap upside in a rising market as the fund’s best performers are sold, or “called away.”

Option Trading, the Complicated Way

Let’s take a closer look at ULTY’s approach. The fund says it has a menu of covered-call strategies it uses on its stocks, which typically number from 15 to 30. These strategies are constantly monitored and adjusted as needed.

This brings me to my second problem with ULTY: All this tinkering results in a lot of turnover: From the fund’s launch, on February 28, 2024, through October 31, 2024, its turnover rate hit 717% of its portfolio’s average value, as we touched on a second ago.

So there’s a lot of management required here, resulting in an expense ratio of 1.3%—high for an ETF. Right now, ULTY is focused on tech, holding names like payment processor Affirm Holdings (AFRM), trading platform Robinhood Markets (HOOD) and crypto exchange Coinbase Global (COIN).

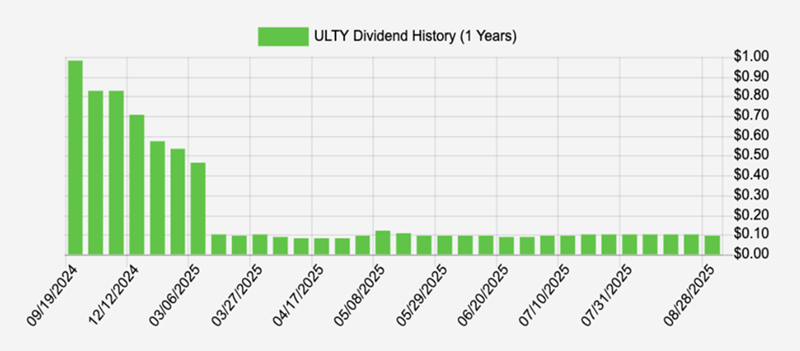

Volatile stocks like these do work well for option trading, but they also add plenty of risk. Then there’s the dividend itself, which, as mentioned, shifted from a monthly payout to weekly last spring.

Weekly Payouts Are More of a Gimmick Than a Help

At first blush, getting paid weekly sounds like a plus. But it doesn’t really help us. If we’re already getting paid monthly—aligned with our bills—why shift to weekly? In a way, it puts us back to managing the “lumpy” payouts we get from the quarterly payers of the S&P 500! And those extra payouts add administrative costs, too.

Small changes in a weekly payout can also paper over large shifts in the fund’s yield on an annualized basis, as we’ll see next.

If we look at the last year, for example (including the fund’s switch from monthly to weekly payouts at the left side of the chart below), ULTY’s weekly dividend jumped to $0.118 a share in the weeks following the April “tariff tantrum.” That makes sense, given its options strategy.

It also makes sense that payouts have drifted lower in the relatively calm markets since.

ULTY’s Dividend Slips After the April Selloff

Source: Income Calendar

The fund’s dividend payable August 29 was $0.0949 a share paid weekly, down from $0.1181 payable on May 9.

That doesn’t sound like much, but it’s a 19.5% reduction, and amounts to an 89% yield, compared to 112% in the spring (both amounts annualized based on ULTY’s share price as of this writing).

All of this is why, instead of chasing too-good-to-be-true payers like ULTY, we focus on high, safe dividends, like the 8.2%-average payers in my Contrarian Income Report service’s portfolio—backed by reliable businesses generating real cash flow.

That’s the right way to build an income stream that can help carry us into retirement and keep us there—on a reasonable nest egg, too.

Forget ULTY: This Growing 11% Dividend Is the Best Buy on the Board

One of my favorite picks in our portfolio is the 11%-paying fund I think all investors—no matter where they are in life—MUST own.

Check out the dividend history on this stout 11% payer: Its monthly payout hasn’t just held steady—it’s grown, and its lucky shareholders have pocketed periodic special dividends, too!

This 11% Dividend Is the Real Deal

It’s also run by one of the best managers in the bond business—he’s been recognized as the top talent in the field on multiple occasions.

Being able to drop an 11% dividend that grows proves his dominance!

All of this is why I see this “battleship” fund as a must-buy for all income investors, especially in uncertain times like these.

I want to give you full details on this fund now—and an extra bonus: 60 days’ access to Contrarian Income Report and its full portfolio of 8%-average payers.