Artificial intelligence is supposed to be graceful, just code humming in the cloud. Yet it’s anything but lightweight. AI is an energy hog.

Every time a chatbot like ChatGPT spits out an answer, it pulls from enormous racks of servers running in data centers. Those servers draw electricity on the scale of small cities.

Over the past few years, AI has been a tech story. With increasing adoption, however, it is about to evolve into a power story.

AI can’t happen without natural gas. Renewables are growing for sure but most new data centers are still tied to gas-fired plants. Gas is abundant and reliable, and it fires up quickly when demand surges.

Which means every new AI deployment is more business for the natural gas pipelines feeding those power plants.

This is bullish for utilities as well as gas producers and pipelines companies. Today we’ll discuss a trio that yields up to 7.5%.

In 2024, Chesapeake Energy merged with Southwestern Energy to create Expand Energy (EXE, 3.3% yield)—America’s largest natural gas producer. It’s a direct play on higher prices.

The Oklahoma City-based E&P firm boasts approximately 1.83 million net acres in the Appalachia and Haynesville basins. Production is huge and growing: EXE produced 7.2 Bcf/d, 92% of which was natural gas, in the most recent quarter, and it expects volumes to grow to 7.5 Bcf/d by 2026.

Free cash flow is also taking a big leap. The company believes it will produce $425 million and $500 million more FCF in 2025 and 2026, respectively, thanks to better-than-expected synergies from the Southwestern acquisition, as well as lower operating expenses, as well as a tax lift from the One Big Beautiful Bill.

A big chunk of that cash is going toward doubling its debt reduction in 2025 (from $500 million previously to $1 billion). The rest? In addition to funding an exceedingly well-covered base dividend of 57.5 cents quarterly, Expand Energy also bought back $100 million worth of stock during the first half, and announced a variable dividend of 89 cents per share, bringing its yield up from about 2.4% to 3.3% (and further variable payouts could add to that yield).

But So Far, EXE’s Variable Payout Hasn’t Triggered the Dividend Magnet

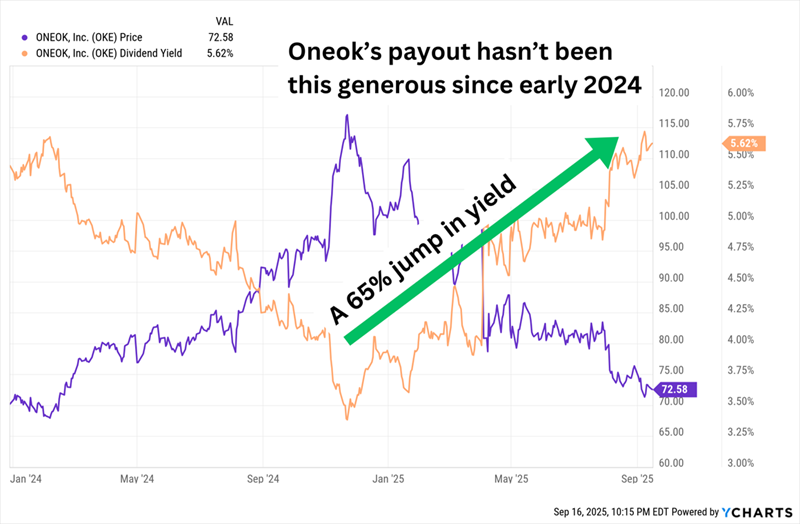

ONEOK (OKE, 5.7% yield) is a warm name to my Contrarian Income Report readers, who enjoyed a total return of 183% on this once-booming energy name.

For the unfamiliar: ONEOK is a “toll collector” that owns some 60,000 miles of pipelines used to transport natural gas, natural gas liquids (NGLs), refined products and crude oil. Its refined products pipeline, at 14,000 miles, is the longest such pipeline system in the US, offering access to roughly half of America’s refining capacity. Its other assets include 53 refined products terminals, four marine terminals, and 115 million barrels of storage.

And CEO Pearce Norton is hearing about demand for those assets directly from AI firms:

“When we met with AI data center companies [last year], they were more interested in, “How can we use AI to help you?” Norton told Hart Energy during CERAWeek, an annual energy conference hosted in March. “That’s flipped. Now they’re saying, ‘How can you help us?’ And it’s because they need energy, and they all seem to be in a hurry for it, which the midstream part of the industry is not going to slow that part down.”

He added that tech companies could put their facilities around existing production in areas such as the Permian Basin and Midcontinent. “That’s going to be speed to market, in and around our existing assets.”

We booked profits as its valuation was beginning to swell. That’s less the case today—shares trade at a fair 12 times 2026 earnings—thanks to a nearly 25% pullback in 2025 alongside declining natural gas prices.

The Upside? ONEOK’s Yield Has Come Roaring Back, Too

As a midstream energy play, ONEOK primarily just gets a cut of whatever’s flowing through its infrastructure and thus shouldn’t live and die by commodity prices. However, prices can reflect slumping demand, plus they can weigh on the profitability of ONEOK’s processing segment.

Let’s note however that ONEOK has taken on a massive amount of debt in its efforts to grow, including the 2023 buyout of Magellan Midstream Partners, in which OKE assumed $5 billion in debt. Its current long-term debt sits around $30 billion, which is two-thirds of its $45 billion market cap.

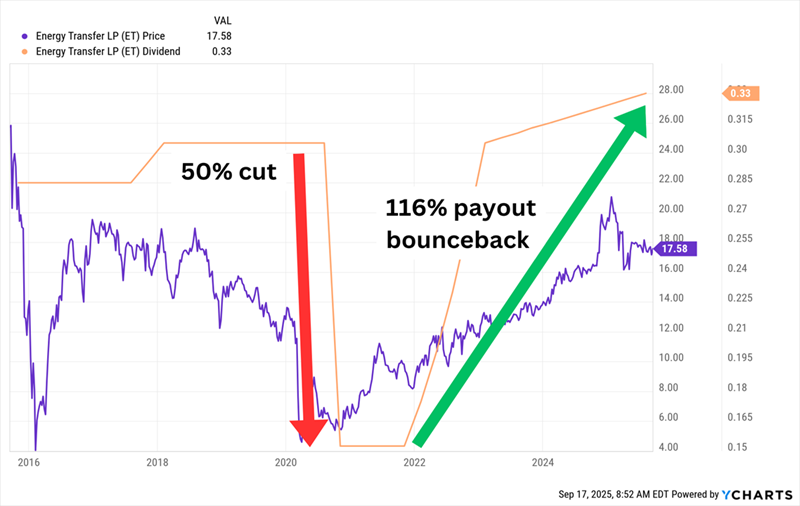

Fellow “toll taker” Energy Transfer LP (ET, 7.5% yield) is another huge infrastructure player with well more than 130,000 miles of pipelines transporting natural gas (~107,000 miles), crude oil (~18,000 miles), NGLs (~5,700 miles) and refined products (~3,760 miles). Its assets also include more than 70 nat-gas processing and treating facilities, 73 million barrels of oil storage capacity, 35 active refined products marketing terminals with 8 million barrels of storage capacity, stakes in other operations, and a developing large-scale LNG export facility in Louisiana.

ET has been a relentless distribution raiser over the past few years, hiking on a quarterly basis since 2021. However, the majority of that has been “catch-up ball” from 2020, when it hacked its payout in half.

The Good News? Distributions Are Back on Track, Back Above Pre-COVID Levels

Rising nat-gas demand over time would help ET continue its streak of quarterly shareholder treats. And ET is seeing many signs of that demand.

Earlier this year, ET signed an agreement with CloudBurst to provide natural gas to datacenter development in Texas. “It’s almost as if Energy Transfer was working years ago to figure out where the best spots are for these data centers, because, if you look at them, the vast majority of them are within several miles of our pipeline,” co-CEO Mackie McCrea said back in February.

Fast-forward to August: Energy Transfer indicated it’s going ahead with a $5.3 billion expansion of its Transwestern Pipeline, which should improve the supply of natural gas throughout Arizona and New Mexico, which should help support demand amid expected data center growth in those states. Then in its September investor presentation, ET said it had fielded requests to connect to more than 60 power plants in 14 states for new connections, and requests to connect to roughly 200 data centers in 15 states across the ET footprint.

A Fully Paid Retirement on Just $500,000?!

ET’s elite near-8% yield almost qualifies it among the stocks that can help us retire on dividends alone.

Why 8%? The math is easy to understand:

- A $500,000 nest egg could earn $40,000—depending on where you live, that could be enough for a fully paid retirement on its own.

- You could generate a $48,000 annual dividend “salary” from a $600,000 nest egg.

- And if you have managed to stow away a cool million bucks to work with, the 8% Monthly Payer Portfolio could pay you an equally cool $80,000 in dividend income every year.

But what makes this portfolio really sing is the monthly frequency of dividends. That means we’re getting paid every bit as frequently as we’re paying the bills.

No complex accounting from one month to the next. No dividend “ladders.” Just money in our accounts every 30 days or so.

It’s like getting a regular salary—without the job!

Don’t miss out on these terrific income plays while you can still get in at bargain prices. Click here for all the details, and turn your portfolio into a monthly dividend machine.