Worried about a recession? If so, this “slowdown-resistant” 4.3% dividend is for you.

Unemployment just hit 4.3%, the highest since early 2021. Payrolls keep missing, and revisions keep knocking prior month numbers even lower. Employers are clearly pulling back.

The jobless headlines suggest an incoming recession. Perhaps. A big driver is automation—white-collar work being replaced by AI. Software is cheaper, faster and never calls in sick. That may eventually weigh on consumer spending in our service-driven economy.

But here’s the investing play: while AI is trimming jobs, it’s also fueling a bull market in energy demand.

Over the past few years, AI started as a tech story. It’s quickly evolving into a power story. Every query to a chatbot taps into racks of servers running in data centers. Each one draws electricity on the scale of a small city.

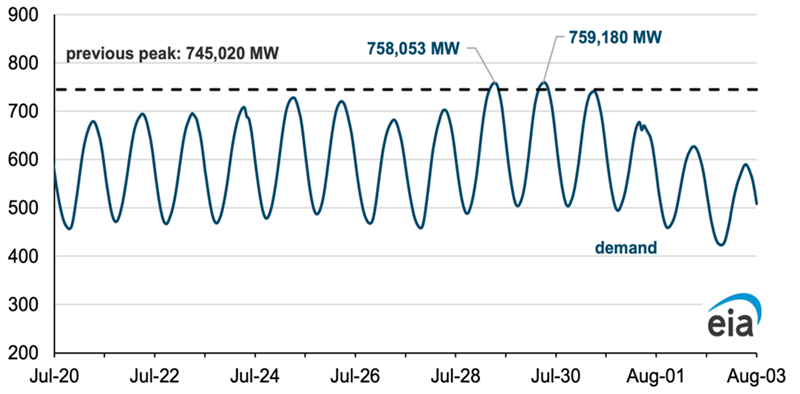

US electricity demand, flat for decades, is surging. The country set two new records for “juice guzzling” in July alone as air conditioners and ChatGPT motored continuously:

Hourly Electricity Demand for Lower 48 (Thousand MW)

Source: US EIA

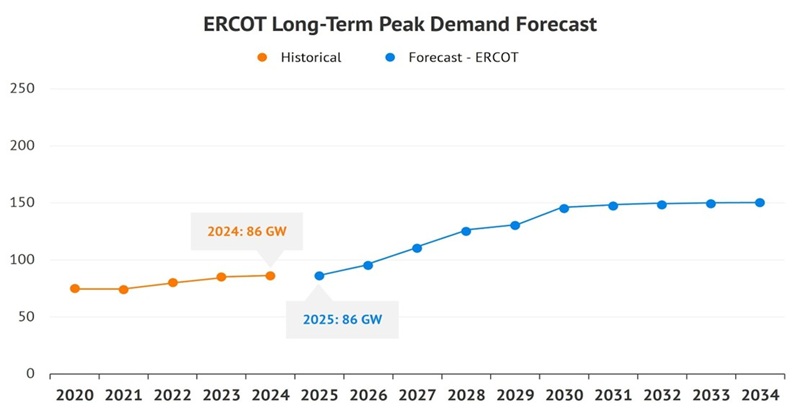

Let’s take Texas, ground zero for the AI-power boom. Low taxes and local incentives have enticed Microsoft, Google, Amazon and Meta to build data centers there. The tech giants are drawn to the largest wind fleet in the US, a fast-growing solar industry and plenty of natural gas. (If Texas were a country, it would be the third largest natty producer after the U.S. and Russia!)

The Electric Reliability Council of Texas (ERCOT) projects Texas will need 139 gigawatts (GW) of new juice by 2030. That’s a 62% jump in only five years!

And this isn’t just Texas. Grid operators nationwide are scrambling to add capacity as data center demand soars. AI can’t happen without natural gas, which makes pipelines the quiet winners of this boom.

Renewables are growing, sure, but most new data centers are still tied to gas-fired power plants because gas is abundant, reliable and fires up instantly when demand spikes. Which means every new AI deployment is more business for the pipelines feeding these plants.

Federal policy now favors more drilling and pipelines. Washington today leans pro-infrastructure, and utilities are leaning on plentiful gas while renewables ramp up.

For Kinder Morgan (KMI), green regulatory lights mean faster approvals, lower legal costs and more pipes in the ground. America’s blue-chip toll collector runs 79,000 miles of pipelines throughout North America, moving crude oil, carbon dioxide, and most importantly about 40% of all US natural gas production. A significant percentage of chatbot requests are powered by gas that travels through Kinder’s network—cha-ching for the toll collector.

Kinder is built to weather energy cycles because 90% of its cash flow is fee-based. The gas flows whether the spot price is $2 or $10. Kinder has boosted its dividend every year since 2018 thanks to rising pipeline volumes. Next, AI demand for energy and a favorable regulatory environment are kicking in.

For 2025, management expects $5 billion of distributable cash flow against only $2.6 billion in dividend obligations. That leaves Kinder with an additional $2.4 billion for growth projects and debt reduction. With dividends requiring just over half of Kinder’s cash flow, payout hikes may accelerate. That’s why a 4.3% yield from Kinder looks unusually safe in this uncertain economy.

AI “pick and shovel” dividend plays like Kinder are cornerstones of my Recession-Resistant Retirement Plan. These are stocks that are set to deliver double-digit annual returns throughout economic cycles. Wall Street is sleeping on them today but catalysts—such as natural gas demand from data centers—will send these stocks soaring tomorrow. Read about my five favorite recession-resistant dividends here.