The Fed has finally cut rates, and if the “dot plot” is any indication, it won’t be the last. This is fuel for real estate investment trusts (REITs)—they thrive when borrowing costs fall and their fat dividends shine next to shrinking bond yields.

Today we can lock in payouts between 6% and 13% from landlords set to surge as Powell’s long-awaited pivot plays out.

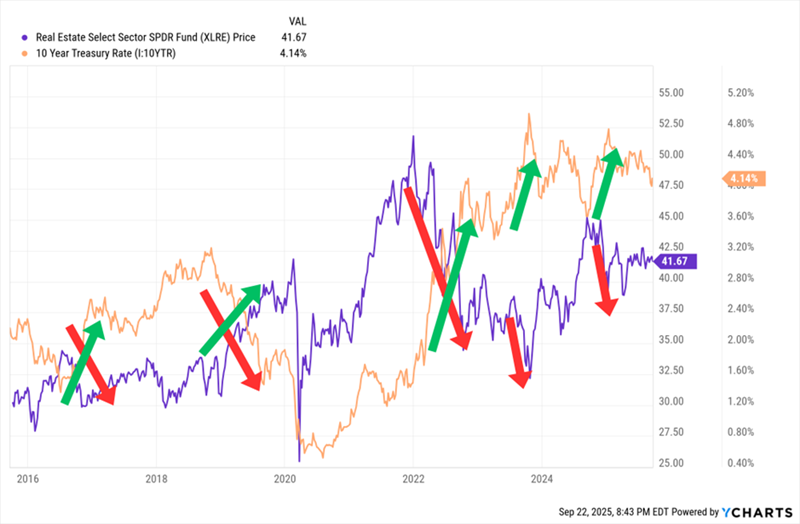

Why do REITs rally as rates fall? These stocks act as “bond proxies” that move alongside bonds and opposite rates. Here is a major REIT ETF plotted against the 10-year Treasury yield. As you can see, when the important rate zigs, the REIT benchmark zags:

REITs Zig When Rates Zag

Rate cuts don’t always hit the 10-year overnight. But the direction is now clear—and history shows that REITs rally once the bond market adjusts. So, let’s look at a lineup of landlords yielding up to 13.3% that are ready to ride Powell’s pivot higher.

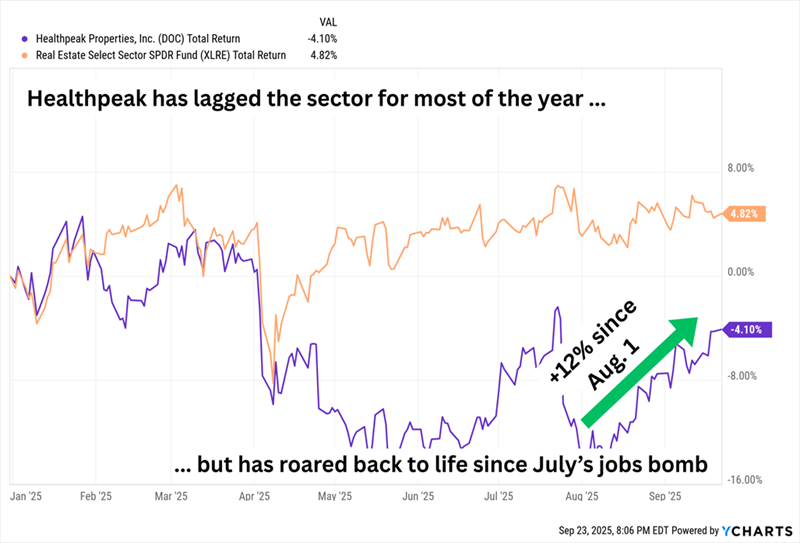

We’ll start with Healthpeak Properties (DOC, 6.5% dividend yield). Healthpeak owns 702 properties across outpatient medical, labs and senior housing. This blend has weighed on 2025 results because labs have been weak. However this “property patient” has perked up since August, when a sad jobs report foreshadowed the September rate cut.

In other words, the Fed is driving this rebound:

Healthpeak: Riding High on Rates Over Fundamentals

Broadstone Net Lease (BNL, 6.3% dividend yield) specializes in single-tenant commercial properties. Currently, its portfolio is made up of 766 properties in 44 states and four Canadian provinces, leased out to a whopping 205 tenants representing more than 50 industries.

Its blend looks a lot different than it did even a year or two ago—Broadstone has been actively shedding healthcare properties, which made up roughly 20% of annualized based rent back in 2024 but now accounts for less than 4% of ABR. Today, industrial makes up roughly 60% of ABR, retail accounts for more than 30%, and office buildings drive most of the remainder.

Broadstone deals in “net leases,” where tenants cover taxes, insurance and maintenance costs. BNL just collects rent. Those long-term leases, with built-in 2% rent escalators, deliver the steady cash flows we want from a landlord.

I said more than a year ago that although its transformation might weigh on earnings in the short term, “the renewed portfolio focus is a benefit to BNL.” At the time, insiders thought so too.

All of us were right.

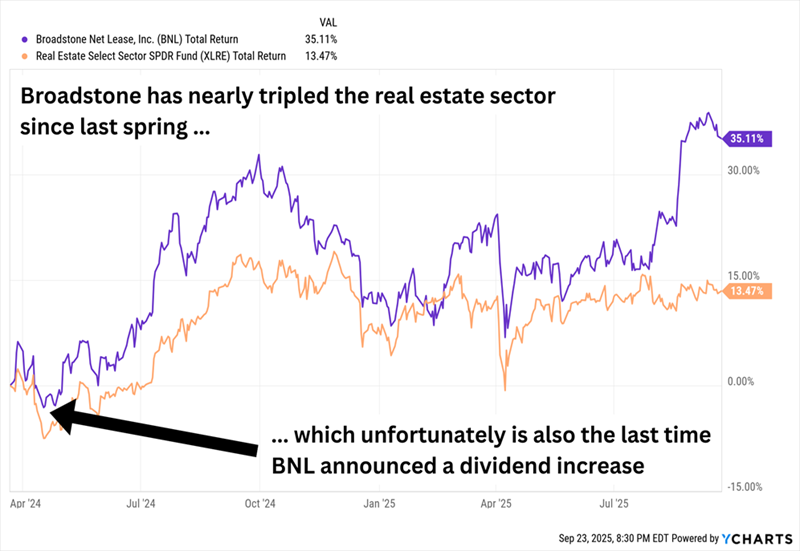

But Broadstone’s Success Is Missing One Critical Component

Broadstone’s doing a lot that we can like. It looks like it’s handling the bankruptcies of tenants At Home and Claire’s in stride. Management expects that its burgeoning build-to-suit pipeline will reach its $500 million end-of-year goal.

But it’d be nice to see BNL share the wealth. The company recently updated its full-year guidance for adjusted funds from operations (AFFO), expecting $1.48 to $1.50 per share. It’s on track to pay $1.16. BNL could easily boost its dividend. Management just hasn’t shared the wealth yet.

Global Net Lease (GNL, 9.4% dividend yield) is another commercial net-lease operator, and it has a significant international bent.

GNL’s 911-property portfolio spans 10 countries. North American operations (U.S. and Canada) account for 70% of straight-line rents; eight European companies account for the remaining 30%. The average remaining lease term isn’t as long as Broadstone’s, at just over six years, but it does utilize rent escalators, which are on 88% of leases.

Global Net Lease has also been busy trying to improve its operations. It recently completed the $1.8 billion sale of its multitenant retail portfolio, which improved overall occupancy and improved its annualized net operating income (NOI) margin. It has been buying back stock. And it has been rapidly deleveraging—GNL has shed $2 billion in net debt in roughly a year. During the company’s most recent earnings call, CEO Michael Weil noted that “S&P Global upgraded our corporate credit rating to BB+ from BB and raised our issuer level rating on our unsecured notes to investment-grade BBB- from BB+.”

The stock has been doing exactly what we’d expect in the midst of that kind of turnaround, beating the pants off the real estate sector year-to-date.

But There’s Still a Big Black Mark We Need to Talk About

GNL’s past payout cuts weren’t by choice—they were survival. Dividend coverage looks fine today, but only if cash flow keeps climbing.

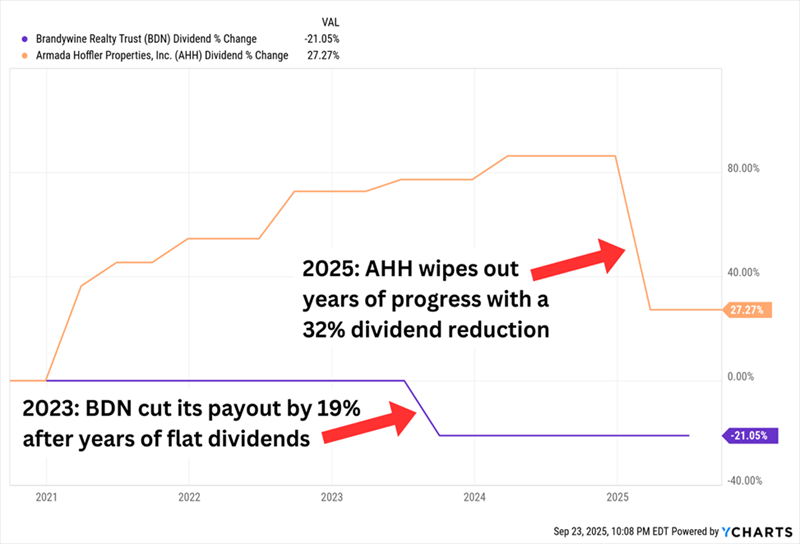

A couple “hybrid” REITs—Armada Hoffler Properties (AHH, 7.7% dividend yield) and Brandywine Realty Trust (BDN, 13.3% dividend yield) are benefiting from a one-two punch: declining rates and return-to-office mandates.

But both cut payouts this year and their balance sheets leave no margin for error:

2 Big Yields, But 2 Very Recent Distribution Cuts

Armada Hoffler kicked off 2025 with weak guidance and a quick dividend cut. It’s still on pace for a significant drop in FFO, and its guidance hasn’t changed, but the most recent quarter saw at least a few green shoots, including a slight improvement in same-store cash NOI growth.

Brandywine, while a hybrid REIT, is much heavier in office influence. BDN owns 63 properties representing ~11.8 million rentable square feet, and office space accounts for just less than 90% of each (56 properties representing ~10.4 million rentable square feet).

Joint ventures have been Brandywine’s Achilles’ heel of late; some of its development deals force BDN to recognize numerous costs until the projects become profitable, and that has resulted in significant downward revisions to FFO estimates. Relief could be on the way, though, as several JVs could be recapitalized in coming quarters. Brandywine also secured a massive deal with Nvidia (NVDA), which will occupy nearly 100,000 square feet in BDN’s One Uptown development in Austin.

But let’s keep a really close eye on the dividend. The payout was 107% of FFO through the first half of 2025, and full-year FFO are expected to just barely pay for the dividend. If Brandywine runs into liquidity issues, that 13%-plus yield could be a rug-pull just waiting to happen.

Avoid the Retirement ‘Death Spiral’: Collect 8% or More for Life

AHH and BDN aren’t buys, but they prove the point that “comfortable” isn’t safe in retirement.

The #1 mistake investors make today? They confuse “comfortable” with “safe.”

Blue-chip stocks and 10-year Treasuries might make you feel all warm and fuzzy.

But if you’ve been saving and investing “by the book,” you’re already behind—and it could take just one poorly timed downturn in retirement for you to realize your mistake.

Suddenly, you’re forced to sell a bigger-than-expected chunk of your nest egg just to pay the bills, and you find yourself way behind the 8-ball for the rest of your life.

That’s the retirement “death spiral.”

And the only way to avoid it is by making sure you live on dividends alone.

You can’t do that with IBM and T-Notes. But many retirees could with my 8% “No Withdrawal” Retirement Portfolio, which produces a sky-high level of income, allowing you to retire on dividend and interest income alone. That means never touching a penny of your nest egg and wrecking your budget in retirement.

Even if you have a mere $500,000 saved up—that’s less than half of what financial pundits say you should have saved!—my “No Withdrawal” portfolio can generate a $40,000 “salary” in retirement.

Not bad! And if you’ve saved even more, even better!

Let me show you the stealth payout plays that Wall Street overlooks: Investments that yield 8%, 9% or even more, empowering us to coast forever on dividends alone. Click here for details in my latest private briefing.