An intriguing article came across my desk recently, and it said something we income investors need to talk about.

It was a Q&A with Morningstar’s director of personal finance, Christine Benz—and it reinforced, to me, why now is the time to snap up one of the top (and 8.4%-yielding) picks from the portfolio of my CEF Insider service.

I encourage you to read this article. It’s mostly fine. But it contains one piece of advice I think will be widely misunderstood. At one point, Benz says:

“What we’ve seen from real estate equities is kind of a steady upward march in correlations with the broad US equity market over the past couple of decades, to the point where I really don’t see the diversification benefit.”

That sounds bad for REITs, but we’re happy to take the other side of this argument and buy. That 8.4% REIT play is our “in” here.

Before we go further, the correlation she’s referring to is the fact that, in recent years, publicly traded real estate investment trusts (REITs) have risen and fallen generally in line with the stock market. This suggests that, if you want to hedge your stocks’ risk. REITs may not be the best choice.

Hold that thought for a sec.

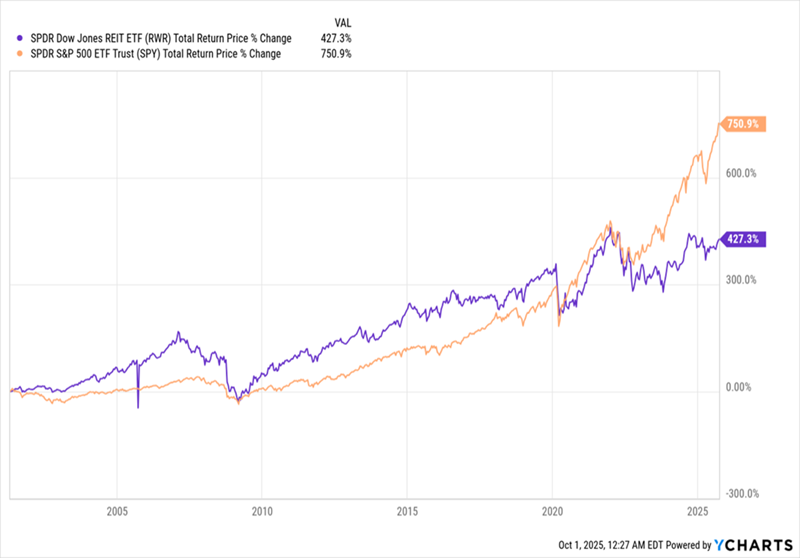

At this point, it’s worth pointing out that REITs, shown below by the SPDR Dow Jones REIT ETF (RWR), in purple, have badly lagged the S&P 500 (in orange) over the last 25 years.

REITs Were Crushing Stocks—Until the 2020 Mess

It’s worth taking a closer look at this chart. During the 2000s housing bubble, REITs were far ahead of the S&P 500, as you’d expect. They even kept their lead after the bubble popped, until the pandemic hit stocks and REITs. Stocks, of course, have recovered. REITs haven’t.

And so, just looking at this chart, yes, these days, REITs aren’t rising when stocks fall, and when stocks do rise, REITs climb, as well—just not as far.

So what Benz says is true. REITs have been moving more or less in line with the stocks of late.

But there’s another part to this story. Benz goes on to say, “You might hold real estate because of their dividend yields or because they get cheap at various points in time.”

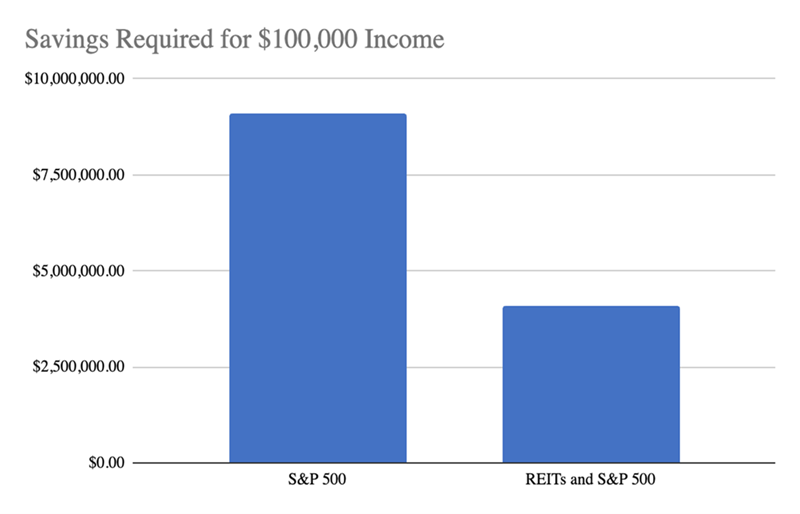

That’s a key point. RWR yields 3.8% as I write this, and the S&P 500 yields just 1.1%, so if you want to cut the amount of savings you need to get a certain amount of income, REITs make a lot of sense. You can see that below, as we compare the savings needed for $100K of passive income from both a pure-stock portfolio and a portfolio of half stocks, half REITs.

Source: CEF Insider

That makes our strategy clear: We want to hold both stocks and REITs. And if we do so through our favorite 8%+ yielding closed-end funds, or CEFs, like the one we’ll discuss in a moment, we can cut the amount of savings we need to get that $100K in passive income even further.

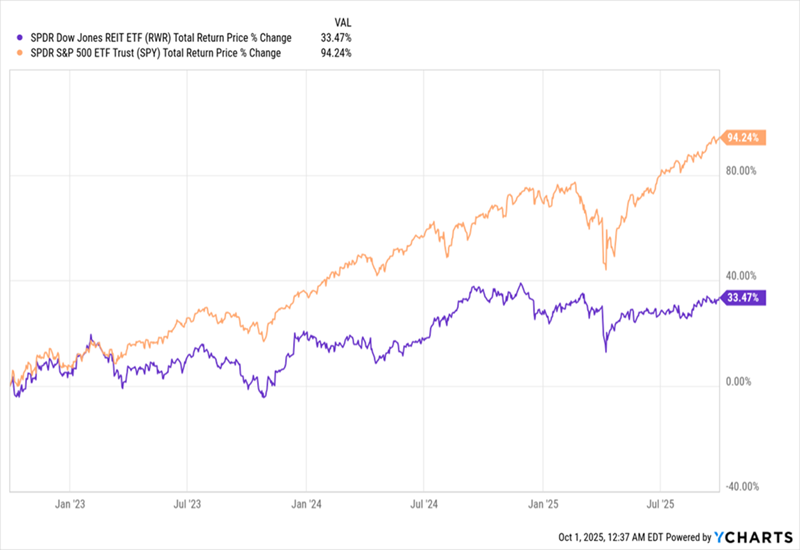

Then, when we get times where the two trade in different directions, we can sell stocks when they’re high and buy REITs when they’re low. That, in fact, is kind of what we’ve seen over the last three years. Even though REITs have risen more or less in line with stocks, they’ve posted about a third of the S&P 500’s gains, suggesting there’s still some value on the table here.

REITs’ Lag Adds to Their Appeal in a Pricey Stock Market

As Benz says, we want real estate for dividends and when it’s underpriced. And those, in fact, are two reasons to buy today—and they actually disprove her point that there’s little point in holding real estate.

But we’re not settling for RWR’s 3.8% payout. That’s less than you’d get from a Treasury.

One Click to 2X (and Then Some) Your REIT Dividends

Instead, we’re buying that 8.4%-paying CEF Insider pick I mentioned off the top: the Nuveen Real Estate Income Fund (JRS). With JRS, that $100,000 annual passive income can be had for just $1.19 million, or about an eighth of what you’d need to invest in an S&P 500 index fund.

Plus you’re getting broad diversification across the REIT sector, with 91 different holdings populating JRS’s portfolio, including warehouse REIT Prologis (PLD), senior-care REIT Ventas (VTS) and data-center REIT Equinix (EQIX) making up the three biggest holdings.

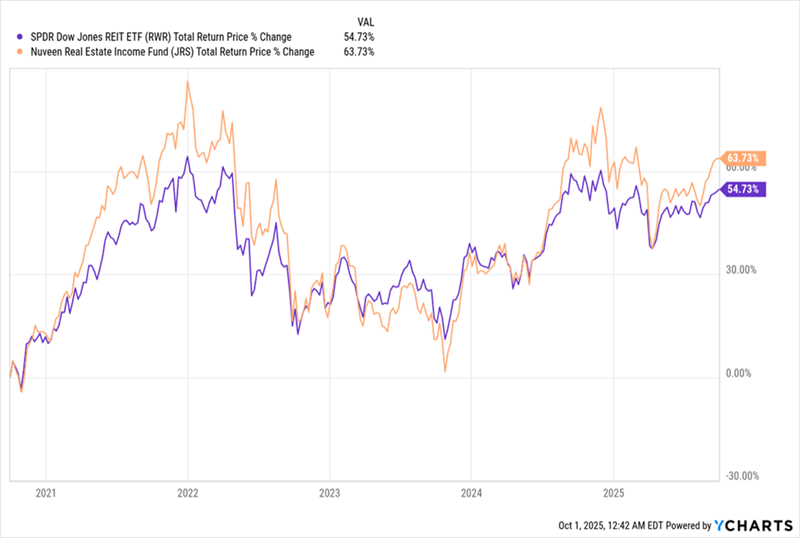

Something else that makes JRS a slam-dunk pick over RWR: It’s outrun the ETF in the last five years, on a total-return basis. And as you can see below (again in orange) its outperformance has been consistent in that time, despite a very tough period for real estate.

JRS Outruns the REIT Field …

In other words, we’re getting real estate exposure and bigger returns than the index fund, on top of an income stream that’s more than 2X that offered by RWR.

The topper? JRS is cheap, in a way that an ETF can never be.

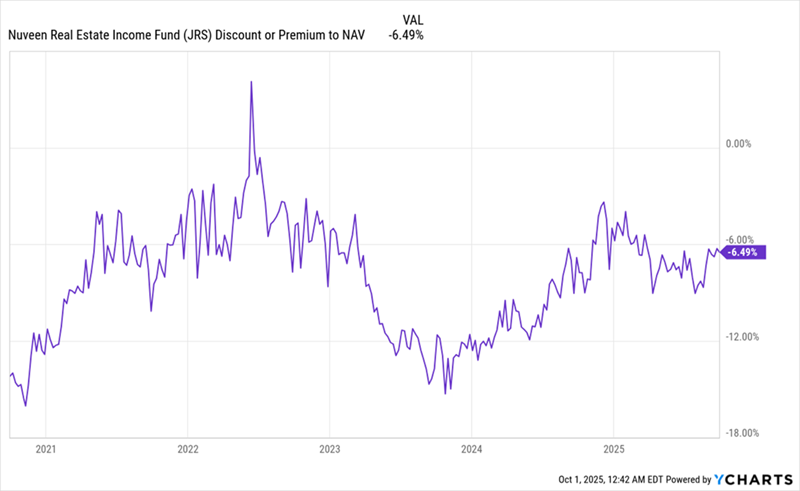

… And Offers Up a Sweet Bargain, Too

As you can see above, JRS sports a 6.5% discount to net asset value (NAV, or the value of its underlying portfolio). These discounts are unique to CEFs—they’re never offered by ETFs.

This deal doesn’t make sense. And as you can also see above, this fund is no stranger to premiums, including one in 2022. Its discount has been closing again over the last two years—but that momentum has stalled lately, giving us a second chance to buy at a bargain.

And the fund’s long-term history tells us that, yes, that 6.5% discount is likely to disappear, putting upward pressure under the share price.

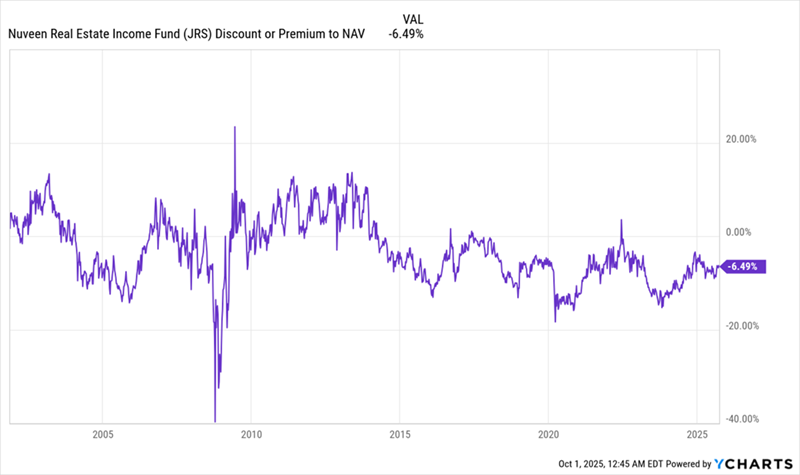

JRS Is No Stranger to Rich Valuations—and Another Is Likely on the Way

Throughout its history, JRS has traded at a premium many times. In fact, premiums were the norm in the 2000s and 2010s.

JRS’s premium may not come back for many years, but it is likely to return someday—and having to wait isn’t so bad when we get to enjoy JRS’s 8.4% dividend. This is the kind of patient approach that builds true wealth—in real estate or anything else—and we’re more than happy to do so.

My CEF Insider Members Are Buying JRS Now—and These 10.2% Monthly Payers, Too

I think you’ll agree that being paid to wait (to the tune of 8.4% a year) for a premium to come along is a pretty sweet deal. Especially when you can get in for a song.

Some of my favorite CEFs pay dividends monthly, and I know readers appreciate getting payouts every 30 (or 31 days) (or, yes, 28 or 29 if we’re talking about February).

That’s why I’ve rounded up my 5 top monthly payers into a “mini-portfolio” I want to share with you now. It pays a rich 10.2% dividend, giving us a huge monthly income stream on a modest upfront investment.

I want to introduce you to each of them now. Click here and I’ll take you on a guided tour of this life-changing 10.2% monthly dividend portfolio and give you an exclusive Special Report revealing the names and tickers of these 5 powerful income funds.