Today we’re going to look at a stock you probably own now (or have in the past)—Visa (V).

Truth is, this “go-to” S&P 500 name has a BIG secret:

Its “measly” 0.68% dividend yield is nonsense. In fact, I’d go as far as to say it’s a complete misdirection.

Buy—or worse, avoid—Visa based on that low yield and you’ll completely miss out on a terrific stock I see completely crushing the market in the years ahead.

Because here’s the real truth about “Big V”: It actually yields 5X what the free stock screeners say it does—and no one realizes it.

Most people just look at that 0.68% and move on. It’s just not enough to get their hearts racing. But the thing is, that current yield tells you almost nothing about the income (or price gains) you’re likely to get from this stock (or any dividend payer, for that matter).

Instead, we need to look at a different “yield”—shareholder yield—which gives us a far better picture (and for owners of Visa, one of the most shareholder-friendly companies in America, a much happier one!).

Shareholder Yield Beats Dividend Yield in Every Way

At the end of the day, a dividend stock has three ways to pay us:

- Its current payout: This is the dividend we get immediately after we buy.

- Dividend growth, which raises the yield on our original buy and acts like a “magnet” on the share price, with the rising payout pulling the share price up.

- Share buybacks, which cut the number of shares outstanding, juicing earnings per share and other per-share metrics.

Buybacks get a bad rap, but they shouldn’t, because when they’re done right (i.e., when the stock is cheap), they can juice our returns. This is another problem with the current yield—it tells us nothing about this buyback effect.

This is where shareholder yield, which includes buybacks and dividends, shines.

Visa’s Shareholder Yield Is the Its Best-Kept Secret

Back to Visa, a holding in my Hidden Yields dividend-growth advisory that’s returned 31% in its latest tour in our portfolio, which started just 14 months ago, in August 2024.

The stock really does nothing but move up and to the right, powered by its “tollbooth” role on the rising tide of digital payments. Moreover, Visa isn’t a lender. It just runs the “plumbing” of its worldwide payment network.

Unfortunately, most income investors miss out on this terrific buy because of that low current yield we just talked about.

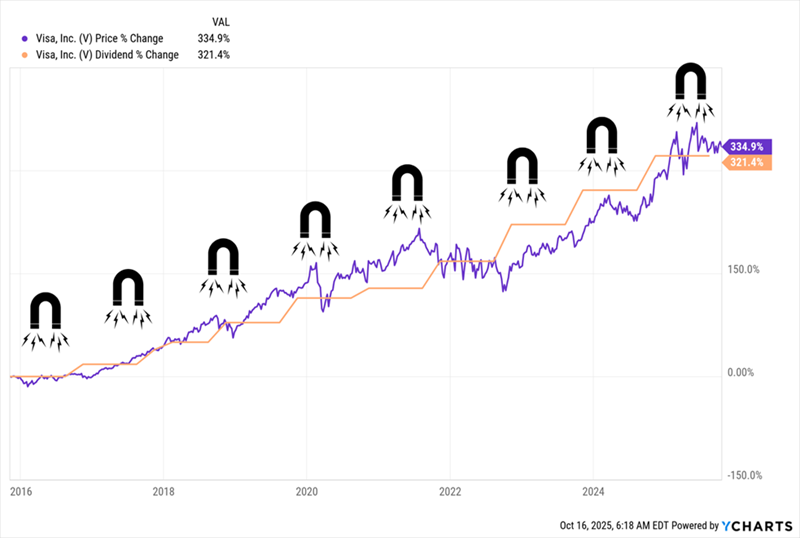

But let’s ignore that for a second and zero in on Visa’s payout growth, which has been en fuego: The dividend is up a stout 321% in the last decade. It’s no coincidence that the share price has gained almost the exact same amount—335%, to be exact:

Visa’s “Dividend Magnet” in Action

Because of that payout growth, investors who bought Visa a decade ago are actually yielding 3.1% on their original buy now. Sure, that doesn’t exactly knock our socks off, but it’s 4.5 times greater than the aforementioned 0.68% current yield.

That’s just the start.

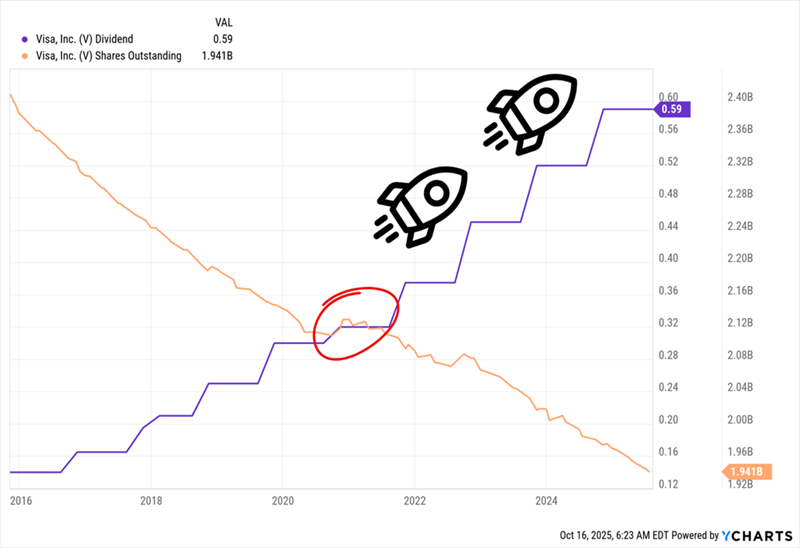

Let’s move on to buybacks: Visa has taken a full 21% (or more than one in five) of its shares off the market in the last five years, making all of the company’s per-share metrics (most importantly earnings per share) look better.

Further, those buybacks fuel dividend growth, as they leave Visa with fewer shares in which it has to pay out. It’s no coincidence that Visa’s dividend growth has taken off as its share count has dropped:

Buybacks Ignite Visa’s Share Price

Take a close look at that chart—you can see the dividend taking bigger jumps once Visa restarted buybacks after slowing them during COVID.

The beautiful thing about shareholder yield is that it combines all three shareholder rewards: current dividend, payout growth and buybacks. Shareholder yield doesn’t show up on free stock screeners like Google Finance, but it’s easy to calculate yourself.

How to Calculate Shareholder Yield

To calculate shareholder yield, take the amount a company spent on share repurchases in the preceding 12 months, deduct any cash brought in through share issuances, then add in the total spent on dividends.

You then take that sum and divide it into the company’s market cap, or the value of all its outstanding shares.

In Visa’s case, that comes out to $4.53 billion spent on dividends and $19.2 billion spent on buybacks (Visa has always favored buybacks over dividends for shareholder returns—given its performance, we’re more than okay with that!).

Add those two figures and you get a total of $23.7 billion in total shareholder returns in the 12 months ended June 30, 2025.

With a $670.1-billion market cap, we can say that Visa sports a 3.5% shareholder yield—again about five times more than the current dividend yield of 0.68%.

That’s the real yield this cornerstone stock offers, and I expect more as it grabs a bigger slice of the digital payments market in the years ahead.

Ignore Recession Fears: Visa Is About to Soar

Digital currencies are the new frontier for payment processors, and Visa’s not being left behind.

In fact, it’s leading the charge.

In the latest issue of Hidden Yields, we take a close look at how the company is putting itself on a path to grab an even bigger slice of the payments market as more of these “digital dollars,” or “stablecoins,” flow through its network.

What most people don’t realize is that these stablecoins are getting a little-reported “assist” under new federal legislation.

It’s a change that’s set to bring big—and profitable—changes to the company, and it’s changed my recommendation on the stock.

With that in mind, here’s what I want to do for you today:

Right now I invite you to try Hidden Yields risk free. As a Hidden Yields member, you’ll get instant access to our portfolio, including my latest research on Visa’s “new stablecoin frontier.”

That’s not all.

I also want to GIVE you—right now, today—my 5 top dividend-growth picks to buy now.