Each of my kids collected more than three pounds of candy on Halloween Night. Three-plus pounds! Their efforts were not superhuman by my best late-80s-to-early-90s estimation.

We are going to have these bags until Easter.

The candy hangover was real. Both YMCA basketball games played “the day after” were utter disasters for their dad and coach.

Sugar-high crashes are real. Which is why we are talking “sleep well at night” dividends paying up to 8.6% today.

Don’t be Coach Brett the day after Halloween. If you’re worried about a Wall Street sugar withdrawal, the time to prepare ye ‘ol portfolio is right now.

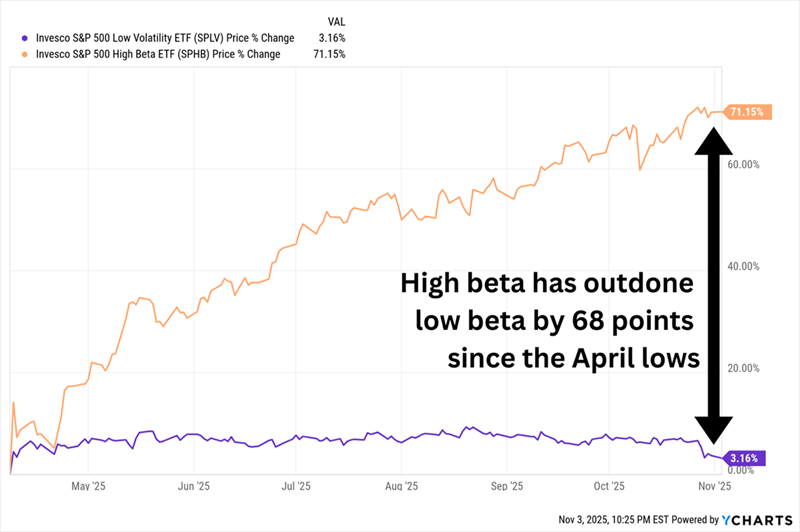

“Low beta”—the boring, sane value stock and/or dividend payer—has rarely been this cheap. The crowd is chasing the “high beta” racehorses:

“Slow and Steady” Has Lost This Race by a Country Mile

“Beta” is a quick-and-dirty way to measure volatility. A beta of above 1 means a stock is more volatile than the market, and a beta of below 1 means it’s less volatile.

Generally, the lower the beta, the more stable the stock—which cuts both ways. They’re probably not going to sizzle in a bull market like this, but they also will give up less ground (or actually gain ground) if the environment turns bearish.

So consider this a shopping list of stocks we’ll want to have at the ready should this relentless bull market hit a wall.

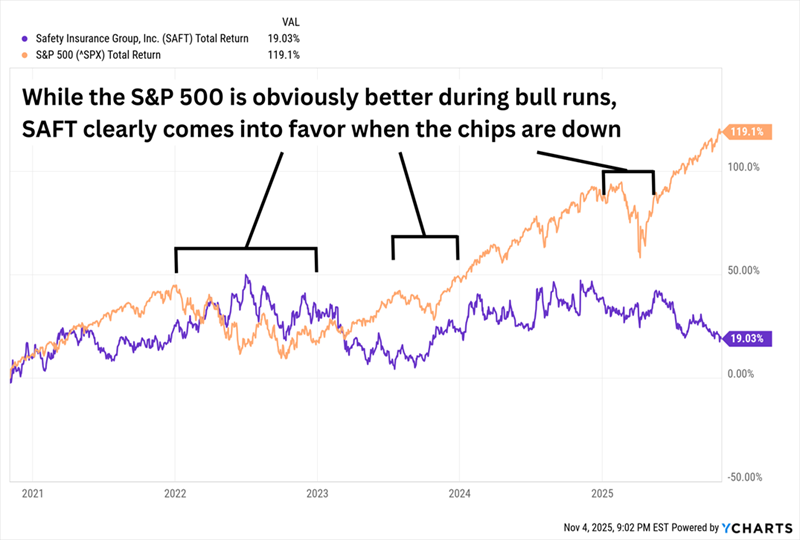

Let’s start with Safety Insurance Group (SAFT, 5.2% yield), an A.M. Best “A”-rated insurer providing property and casualty (P&C) insurer serving Massachusetts, New Hampshire and Maine. The biggest chunk of its business is writing private passenger automobile insurance (~55% of direct written premiums), it also offers homeowners (24%), commercial auto (15%), dwelling fire, umbrella, and business owner policies.

Vanilla investors don’t expect insurance to be a low-volatility business given that insurers are known for big profitability swings based on natural disasters and other exogenic events. But, in fact, the insurance industry has been about half as volatile as the broader market over the past few years, and SAFT is no exception, boasting a 1- and 5-year betas of 0.47 and 0.26, respectively, that tell the tale of a pretty sleepy stock.

Not That Sleepy Is Necessary Good Very-Long Term

The low volatility is nice for downturns, as is SAFT’s attractive 5%-plus yield.

The business itself hasn’t been much to crow about given lackluster underwriting results over the past few years. But its combined ratio (a measure of underwriting profitability that’s calculated as incurred losses + expenses / earned premium) has recently dipped below 100%, which is a big step in the right direction.

Another big step? In August, the company improved its payout by 2%. It’s small, but it’s the first raise since 2019—momentum in the right direction.

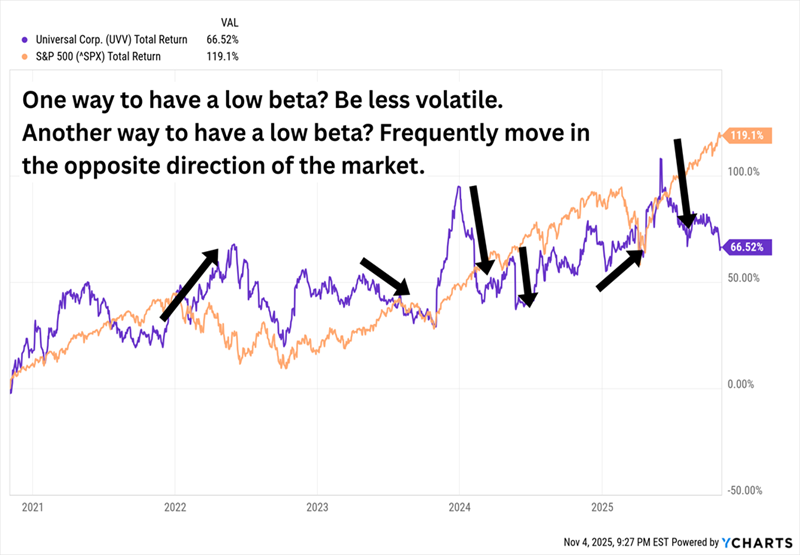

Universal Corp. (UVV, 6.4% yield) comes from a more traditional “safety” business: tobacco. But Universal isn’t our standard Big Tobacco stock, like Philip Morris International (PM) and Altria Group (MO) that produce cigarettes and other tobacco products.

As I’ve said in the past, UVV is a tobacco “picks and shovels” play. Rather than producing tobacco products, it simply provides the tobacco to companies that make the products. And in addition to its leaf tobacco business, it also has a growing ingredients division (Universal Ingredients).

UVV offers the big yield we expect out of Big Tobacco (6%-plus at current prices), but its low betas (1-year: 0.33, 5-year: 0.67) are a little misleading. The stock is actually prone to sharp spikes and quick trenches; its beta is more a result of its counter-market trends.

Universal Isn’t Very Correlated to the Market, Sure. But It’s Still Jumpy.

Universal perks up more often than it doesn’t during market downturns, but it’s not a guaranteed winner in a bear market, either.

It’s cheap, though. UVV trades at 11 times earnings estimates, half its trailing sales and just below book.

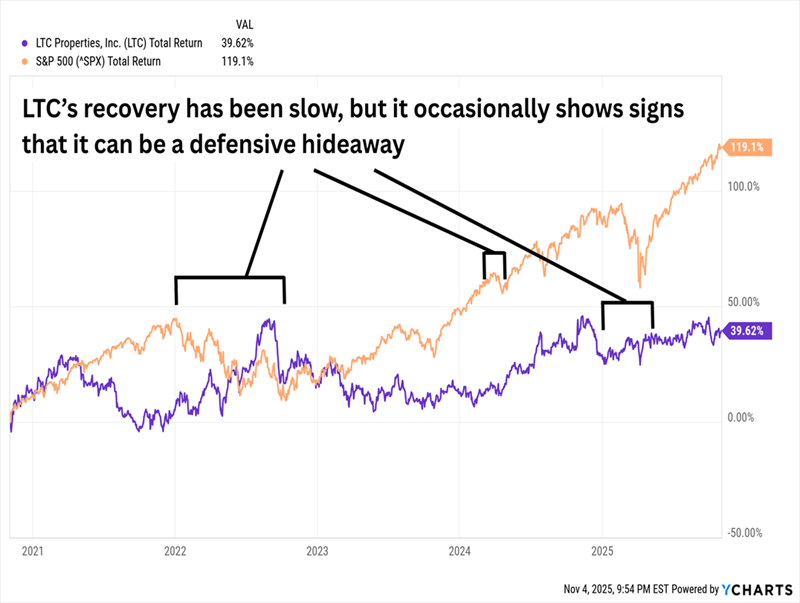

LTC Properties (LTC, 6.4% yield) is a real estate investment trust (REIT) that’s roughly 50/50 split between assisted living properties and skilled nursing facilities. And it’s low on drama, sporting a 5-year beta of 0.62 and a 1-year beta of 0.23 that reflects what has been extremely steady movement over both time frames.

As with SAFT, LTC shows how low beta can lag during bull runs.

LTC Hasn’t Exactly Been Spry Over the Past Few Years

That could change. I’ve been following LTC closely this year, in part because it’s shifting part of its business from triple-net leases (that back out taxes, maintenance and insurance costs) into REIT Investment Diversification and Empowerment Act (RIDEA)-structured contracts that gives LTC exposure to the real estate’s operations, which allows the company to participate in net operating income (NOI).

LTC’s price is OK, but not great, at 13 times funds from operations (FFO) estimates, but the dividend yield (6%-plus) is, as is the dividend frequency (monthly).

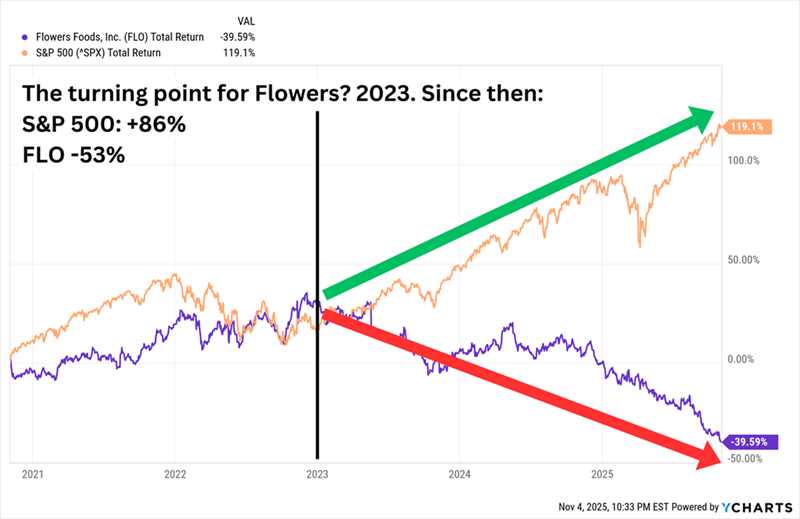

The consumer staples sector is typically good for a few low-vol stocks, and we have one in Flowers Foods (FLO, 8.2% yield). Flowers is a bakery giant whose businesses can largely be split into bread (Wonder, Sunbeam, Nature’s Own, Dave’s Killer Bread, among others) and snacks (Tastykake, Mrs. Freshley’s and more).

The good news? Flowers continues to gain share in multiple categories, and its top line has grown in five of the past six years. Profit growth hasn’t been nearly so consistent, but the arrow is still pointed in the right direction. And yet:

How Does a Company With So Much Yeast Refuse to Rise?

Again, low betas of 0.16 (1-year) and 0.31 (5-year) are misleading, more a product of FLO flopping while the market flies.

But how can a company dealing one of the most vital grocery staples—with stable financial results and a massive yield to boot—have such a floundering stock?

Flowers does face high exposure to import tariffs on key ingredients including sugar, wheat, palm oil, and cocoa. Its snacks division also faces pressure from GLP-1 drug usage. Acquisitions have also ballooned its long-term debt to more than $1.7 billion, which is more than its $1.4 billion in equity (including negligible cash holdings).

But the dividend is high, at 8%-plus, and while it’s not growing rapidly—its May hike was a 3% bump higher—it is growing. Meanwhile, shares trade at about 11 times earnings estimates and at roughly half trailing sales.

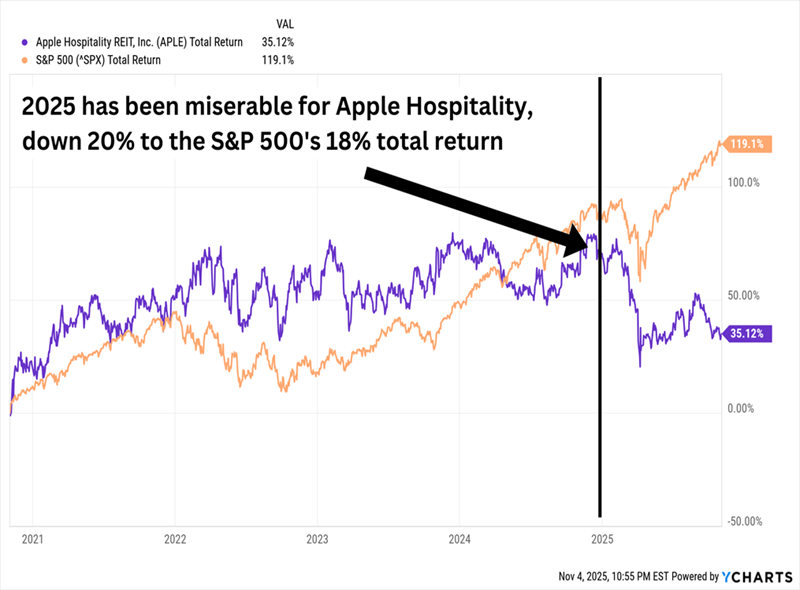

Hotel property owner Apple Hospitality REIT (APLE, 8.6% yield) has been mostly lethargic over the past few years. And as far as low-volatility stocks go, APLE isn’t even all that calm—its 1- and 5-year betas of 0.94 and 0.85 are lower than the market, but not by very much.

APLE Has Really Turned Sour in 2025, Too

Still, we’re talking about an 8%-plus monthly payer with a very safe-looking dividend (75% of adjusted FFO estimates) that trades at less than 9 times those estimates. Could this downturn in APLE be an opportunity?

Apple Hospitality’s portfolio includes 220 hotels across 85 markets in 37 states and D.C. Those are largely split between the Hilton (HLT) and Marriott (MAR) brands, at 118 and 96, respectively, with the remaining five flying the Hyatt (H) flag.

The portfolio is well-diversified geographically, it enjoys strong margins, and World Cup 2026 demand could act as wind in Apple’s sails. A big problem is what to expect until then—as business optimism fades, so too do the prospects for business travel, and Apple is more sensitive to the government shutdown than other hotel REITs.

Monthly Dividends of 9%+ We Can Actually Count On!

APLE is a well-run REIT that’s connected to some of the hotel world’s top brands, but I prefer my cash flow to be less temperamental.

If you’re a long-term investor who wants those frequent payouts at an elite level, but with better business prospects, you’ll appreciate the low-drama, high-yield blue chips I hold in my “9%+ Monthly Payer Portfolio.”

Don’t let the name deceive you.

The “9%+ Monthly Payer Portfolio” isn’t just about earning high levels of yield—it’s about earning high levels of yields by leveraging steady-Eddie holdings that won’t have you reaching for the Pepto every time the economy hiccups or Jerome Powell sneezes.

You also won’t need to stress about the size of your nest egg. Unlike many retirement plans that require you to bleed out your savings as you age, the income this portfolio can generate is so rich, it can sustain a retirement on dividends alone.

Here’s the math: A mere $500,000 nest egg—less than half of what most financial gurus insist you need to retire—put to work in this powerful portfolio could generate a $48,000 annual income stream.

That’s $4,000 every month in regular income checks!

Even better? While the current bull run has many stocks priced for perfection, many of these monthly dividend stocks still remain in our “buy zone” … but they might not be for much longer. So click here to learn everything you need about these generous monthly dividend payers right now!