Drug development will never be the same! AI is compressing time-to-market and extending the sales calendar for pharma. More profits from new medications. More new medications, too.

Many pharma and biotech stocks will boom as we enter the “sci-fi” stage of research and development. And this elite 8.8% dividend will directly benefit.

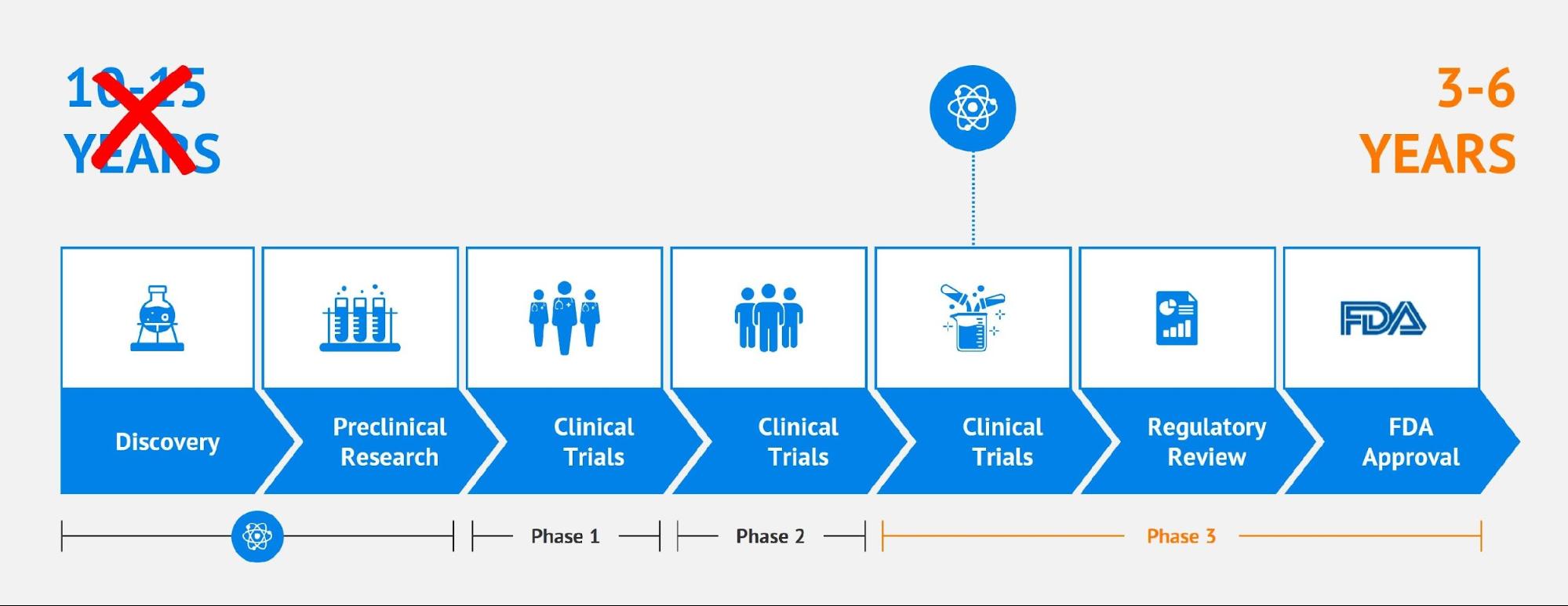

It typically takes 10 to 15 years to develop a new drug. Every month matters because patents last only 20 years. The faster a company gets a drug to market, the more months and years it enjoys with monopoly pricing power.

When patents expire, the generic versions hit the market. And the profit party is over for the original blockbuster.

AI is changing all of this in favor of pharma profits.

Drug discovery cycles are already compressing. From 10 to 15 years, they will soon approach six years or less. Industry experts, in fact, are saying three to six years will be the new normal. Whoa! That shift hands pharma a decade or more monopoly pricing!

No, AI isn’t replacing scientists—it’s multiplying them. These tech models run overnight, on weekends, forever. They eliminate dead ends and push more viable drug candidates into trials.

In the years ahead, pharma will have more shots on goal. Which will result in more drug candidates and approved medications. And by getting these drugs to market faster, these companies will have more time to monetize the winners.

Cash flow is about to compound. So, let’s dial in this 8.8% divvie while we still can.

BlackRock Health Sciences Term Trust (BMEZ) is a closed-end fund (CEF) that owns the companies benefitting directly from pharma’s new sci-fi age. Faster drug development cycles will buoy their bottom lines. Bigger profits will boost stock prices and BMEZ’s net asset value (NAV).

Then, a higher NAV will reward investors with price gains! It will also support BMEZ’s 8.8% payout. And likely reduce or eliminate the CEF’s current 13% discount to NAV.

About that discount. A fun feature of CEFs, unlike ETFs, is that they often trade at discounts to NAV. They have a limited pool of shares, so increased demand for the stock boosts the price. ETFs trade at par—no discount or premium—to NAV. They issue more shares when their funds are in high demand and take shares away when their funds are out of favor.

CEFs “let it ride” with a fixed share count. Which means discounts (and premiums) happen with market emotion. Often. Good for us—buy low and sell high!

As we speak, BMEZ trades at a 13% markdown to its NAV. So, we’re literally paying 87 cents for $1 of assets. A fantastic deal considering the sector’s fundamentals are this strong.

BMEZ’s top holding Alnylam (ALNY) is a pioneer in “RNA interference”—a cutting-edge class of medicine that essentially turns off disease-causing genes. Alnylam’s therapeutics are being explored for treating genetic, heart and neurological diseases.

With AI, these explorations will run faster and better than ever before.

Bad genes? Alnylam fixes them. This company is going to have an R&D “field day” as it deploys AI into its laboratories.

Alnylam’s research also benefits from less regulation. The stock soared under Trump 1.0, racking up 300%+ gains. And the sequel is shaping up to be even bigger with ALNY already up 90% in Trump 2.0.

With holdings like ALNY, why does BMEZ fetch such a large discount? Earlier this year, drug developers were the market’s unwanted stepchild. Wall Street assumed Trump 2.0 would hammer drug prices even harder than Biden’s Inflation Reduction Act (IRA) already did.

Remember, Trump 1.0 kicked off the insulin caps. Biden’s IRA bill followed with price limits on ten blockbusters starting in 2026—a potential $160 billion profit hit to Big Pharma. Then Trump returned and chased Most-Favored-Nation (MFN) pricing, aiming to tie US drug prices to the lowest in the world.

Bad for pharma profit margins, to say the least! Investors dumped healthcare shares across the board in a final selling effort. After five years of underperformance, these stocks were wiped out.

But on cue, pharma did what pharma always does—it lobbied! MFN pricing stalled. The lobbyists slowed the political avalanche.

Meanwhile, the White House struck a headline-friendly deal with Pfizer. Then AstraZeneca. And three more big pharma firms. It looked like pharma was getting squeezed, but the fine print gave drugmakers exactly what they wanted: longer patents, faster reviews and cleaner reimbursement rules.

It’s a public relations win for the Administration. But most notably, it’s a quiet victory for the drugmakers. Firms are already benefiting from softer regulatory gloves and faster review cycles—the fastest ways to cash for any pharma firm.

More drugmakers will cut deals with Washington. More drugs will come to market thanks to AI. More companies will profit from their patent window as drug development times compress.

But BMEZ is still priced as if the 2024-25 pharma washout is ongoing, even though regulatory clouds are parting and AI is supercharging R&D! Let’s take the dividend deal while we can.

In our November edition of Hidden Yields, we discussed a pharma “pick-and-shovel” provider with even more upside than BMEZ! This stock could rocket as this sector enters its sci-fi age.Need a subscription to HY? Sign up on a risk-free basis here and you’ll get access to my new pick plus five recession-resistant dividend stocks set to deliver 15%+ total returns in the years ahead.