Let’s get our 2026 dividend shopping finished ahead of time, shall we?

Come January, we’ll have plenty of company from vanilla investors, rushing to “figure out the new year.” Trends. Predictions. Buy this!

But there’s no reason to wait. We already know some of the key dimensions of 2026. Interest rates, for one, are on their way down. Fed Chair Jay Powell has delivered two rate cuts to end the year, with more to follow.

Whether or not Powell personally delivers them doesn’t matter to us. Powell is on his way out. But the Fed show will go on, with a ringmaster ready to roll.

Kevin Hassett isn’t some mystery bureaucrat drifting into the big chair. He’s been broadcasting his playbook for two decades. Hassett spent the 2000s arguing that the Fed moves too slowly, waits for too much data and leaves too much growth on the table. He quipped that the Fed should “cut early and cut often” because market confidence is a policy tool, too.

Now, he gets to run the show. And he’s being appointed by an administration that wants mortgage rates lower yesterday, housing market activity and growth charts that point up. Hassett knows the assignment—cut early and often!

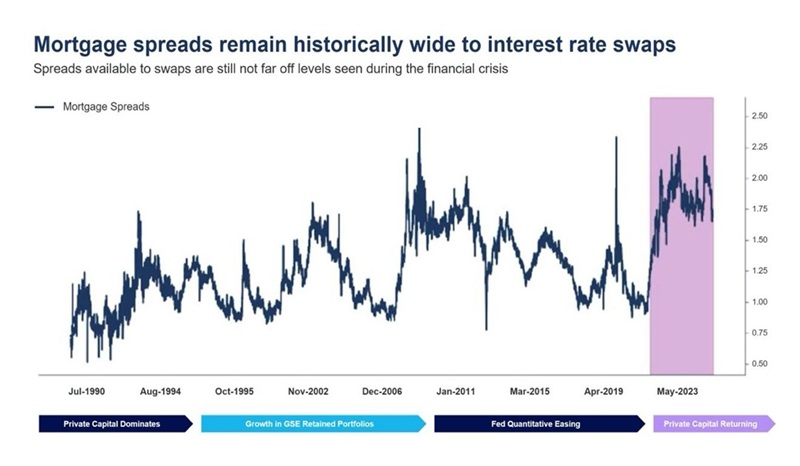

When this happens, mortgage REITs Annaly Capital (NLY) and Dynex Capital (DX) are going to run. These stocks yield 12.3% and 14.7% respectively, but these dividends are merely a generous appetizer for the main course of price appreciation. Annaly and Dynex both boast portfolios that are perfectly positioned for the dawn of the Hassett era. They own government-backed mortgages that rise in value as long-term rates fall. Few companies benefit more from falling rates than these two.

Annaly and Dynex are sneaky bargains with mortgage spreads—the difference between the 10-year Treasury yield and mortgage rates—just coming down from manic levels. Over the last 20 years, the Great Financial Crisis, 2023 bond meltdown and 2024 mortgage-rate spike delivered the greatest “spreads” in which it was a great time to be an mREIT buyer:

Mortgage Spreads Ease from Manic Levels

The spread is the engine of profit for Dynex and Annaly, and the engine rarely runs this hot. Both firms loaded up on cheap “agency” mortgage-backed securities when spreads were peaking. These are government-guaranteed bonds backed by Fannie Mae and Freddie Mac. No subprime surprises or commercial property problems here.

Spreads have been easing with mortgage rates coming down all year. The administration wants them lower. With each tick down, Annaly and Dynex portfolios gain in value.

Now 2026 won’t just be about cheaper money. It will be the first commercial year of “Applied AI”—where AI moves past the hype stage and starts showing up in margins, product cycles and cash flows.

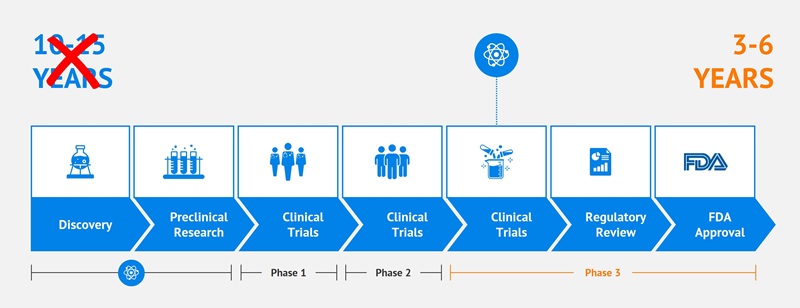

Historically, it has taken 10 to 15 years to develop a new drug. Every month matters because patents last only 20 years. The faster a company gets a drug to market, the more “gravy” months and years it enjoys with monopoly pricing power.

When patents expire, the generic versions hit the market. And the profit party is over for the original blockbuster.

AI, however, is extending the sales calendar starting in 2026.

Drug discovery cycles are already compressing. From 10 to 15 years, they will soon approach six years or less. Industry experts, in fact, are saying three to six years will be the new normal. Whoa! That can be a decade or more monopoly pricing!

No, AI isn’t replacing scientists—it’s multiplying them. These models run overnight, on weekends, forever. They eliminate dead ends and push more viable drug candidates into trials.

In the years ahead, pharma will have more shots on goal, resulting in more drug candidates and approved medications. And by getting these drugs to market faster, these companies will have more time to monetize the winners.

Profits are about to pop. BlackRock Health Sciences Term Trust (BMEZ) yields an elite 8.6%, owning some of the most innovative drug development companies on the planet. BMEZ is a neat way to buy them at a discount to their net asset value, with an enhanced dividend.

Pharma’s pick-and-shovel provider is also well positioned. A current of new pharma money will flow upstream into the company supplying the labs.

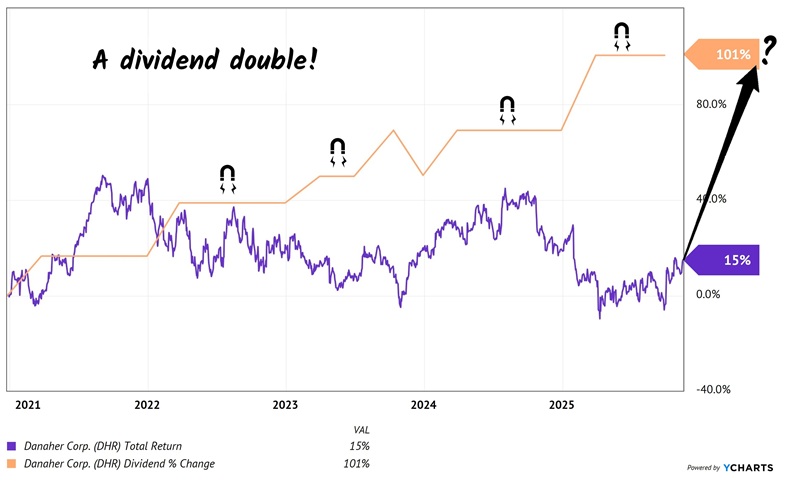

That’s Danaher (DHR), the quiet go-to company in life sciences and diagnostics. Danaher doesn’t sell drugs. It sells the tools, the instruments, the purification systems, the diagnostics, and, critically, the consumables that pharma needs to move discoveries from idea to lab to clinic to market.

No consumables, no experiments. No experiments, no drugs.

And because Danaher doesn’t sell drugs itself, it avoids the political circus entirely.

Consumables are the big catalyst here—they are the “razor blades” that labs burn through every day, and AI-driven R&D means more experiments, not fewer. That’s the first place we’re seeing gains at Danaher.

And its dividend? A phat double in a mere five years! When a payout pops 100% and a stock price rises only 15% over the same time period, saying the stock is “due” for a rally is an understatement.

Danaher’s Dividend Magnet is Due

Danaher’s management treats shareholders to regular raises, and these generous hikes add up.

Of course AI itself is a tremendous power hog. Every time ChatGPT generates a response, it pulls from enormous racks of servers running in data centers. Those servers draw electricity on the scale of small cities.

The servers are fed by the “boring” utility stocks owned by Reaves Utility Income Fund (UTG). Our closed-end fund yields 6.2%

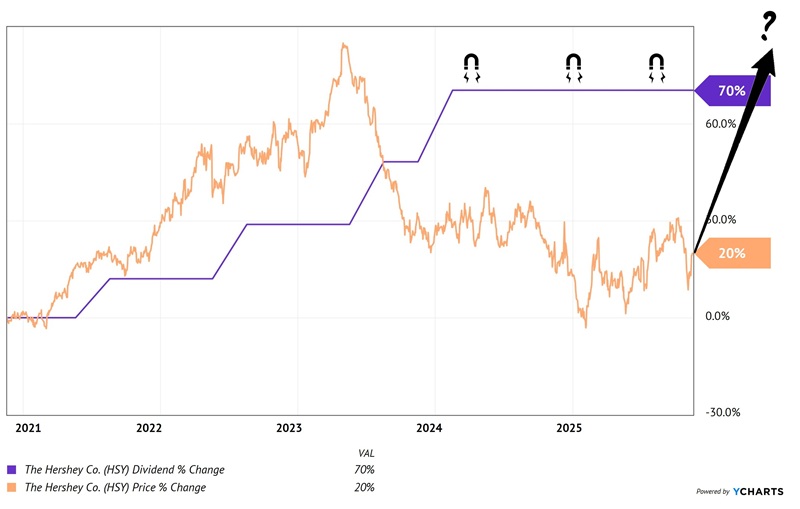

Finally, on a completely different topic from interest rates and Applied AI, let’s talk about chocolate. Hershey Foods (HSY) deserves our attention. This is an American icon that pulled back when cocoa prices exploded, input costs spiked and margins compressed.

But Hershey didn’t lose its competitive moat just because cocoa had a tantrum. The brands are as dominant as ever—Reese’s, Hershey Bars, Kit Kat, Kisses, Twizzlers—the whole candy aisle lives under this roof.

Even as cocoa kept rising, Hershey’s cash flow rebounded. Management quietly rolled out a two-year efficiency plan, pushing automation deeper into the production lines and tightening costs. They raised prices across the portfolio. And consumers, as they almost always do, kept buying their comfort food.

What we’re really buying here is the return of the dividend magnet. Hershey raised its payout 70% during a five-year period where the stock meandered. That is the kind of “magnet gap” we love to pounce on!

Hershey’s Dividend Magnet is Due

With input costs easing, restructuring savings flowing, and a beaten-down share price that’s starting to rally, Hershey is primed for a rebound.

Megatrend stocks like these are the secret to retiring on as little as $500K. The “suits” that say we need $2 million or more are talking their own book. Their “safe” strategies are failing while we income investors secure our own dividend-powered retirements with megatrend stocks like these. Here’s how we turn $500K into a stable income stream that could last decades.