The bankruptcy of auto-parts supplier First Brands has hit a corner of the market known for high dividends. Does that make these assets bargains?

Maybe. But we need to be careful here, and avoid making the mistake of “reaching for yield”: that is, buying yields that are high for a reason: the stock price has plunged.

But I’m getting ahead of myself. The corner of the market I’m talking about is business development companies (BDCs), which loan money to small- and mid-sized firms.

Investors first got worried about BDCs a couple months ago, when the First Brands story broke. The news raised alarm about the private-credit market (where BDCs operate). JPMorgan & Co. (JPM) CEO Jamie Dimon added to those fears, saying there were likely more “cockroaches” here than just First Brands.

BDCs Look Like Bargains, But Beware the Traps

I know that quite a few readers of my CEF Insider service invest in BDCs, or at least follow them. It’s easy to see why, with the double-digit yields many BDCs offer.

But if you’re looking to buy this dip, there are two tickers I urge you to avoid. We’ll discuss those now, then follow up with another high-income play—a deep-discounted closed-end fund (CEF) yielding 8% that’s well-suited to this market. To be clear, neither of the BDCs we’re going to discuss now has any real exposure to First Brands.

High Fees Make This 11.9%-Paying BDC a Sell

First up is Blue Owl Capital (OBDC), which has fallen along with most of the BDC market. You can see that in the chart below, with its total return (in purple) and the return of the BDC benchmark VanEck BDC Income ETF (BIZD), in orange:

Private-Credit Fears Hit BDCs—and Blue Owl, Too

So does this dip make Blue Owl a bargain?

Nope. The first reason why? Fees. As of now, OBDC’s base management fee is 1.5% of assets, according to BDC Investor, plus it takes roughly 17.5% of all net investment income. So yes, high fees are an issue here.

But we do need to keep in mind that running a BDC is a complex job requiring a lot of legwork: OBDC manages over 200 assets, and almost all of those are loans made to smaller, unlisted companies. That means more monitoring and due diligence than if you’re lending to large, publicly traded firms. So those fees are understandable if the BDC delivers strong results.

But so far this year, OBDC is simply matching the BDC market (which is itself underwater), so it hasn’t shown outperformance. How about the long run? Since its IPO in 2019, the stock’s total return (in purple below) has trailed that of BIZD.

Blue Owl Lags Its Benchmark

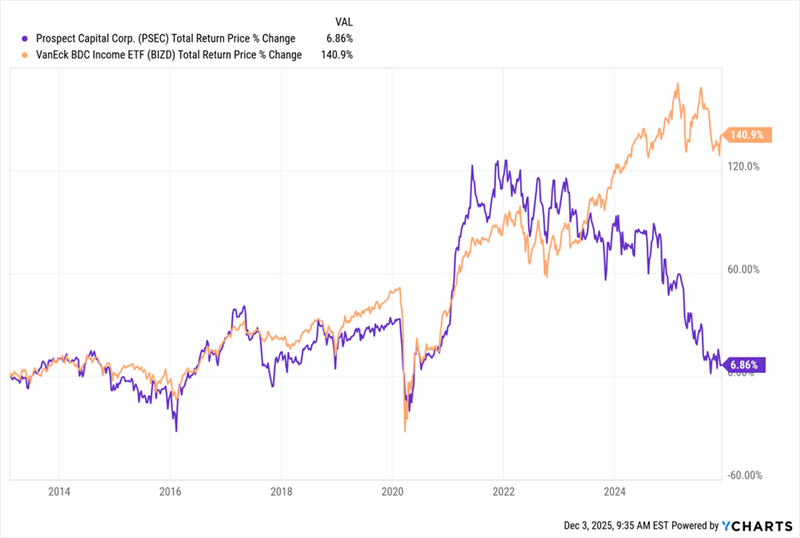

So let’s move on to our next BDC, which, according to BDC Investor, is the cheapest one on the market, at a 60% discount to NAV. That would be Prospect Capital Corp (PSEC). Here’s its long-term chart.

No Good Prospects With Prospect

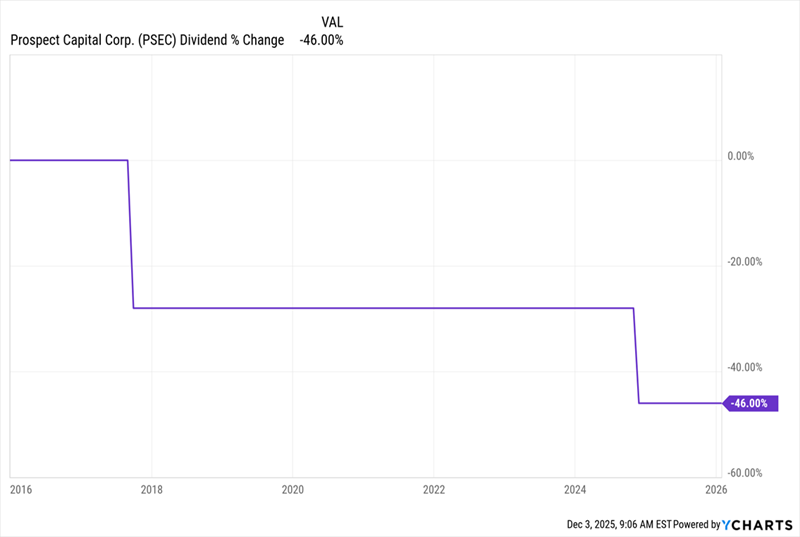

It’s fair to say that PSEC’s long-term return doesn’t inspire, at 7% over the last decade. Moreover, its 20.9% current yield is a danger sign. It’s no doubt attracted plenty of buyers over the years, but they’re paying in the form of missed gains and lower income. PSEC’s payout has dropped in half in the last decade.

PSEC’s Falling Payout

PSEC and OBDC are examples of common risks involved with BDCs. Which is why, at this moment, I recommend putting more weight on another high-yielding asset class: closed-end funds (CEFs).

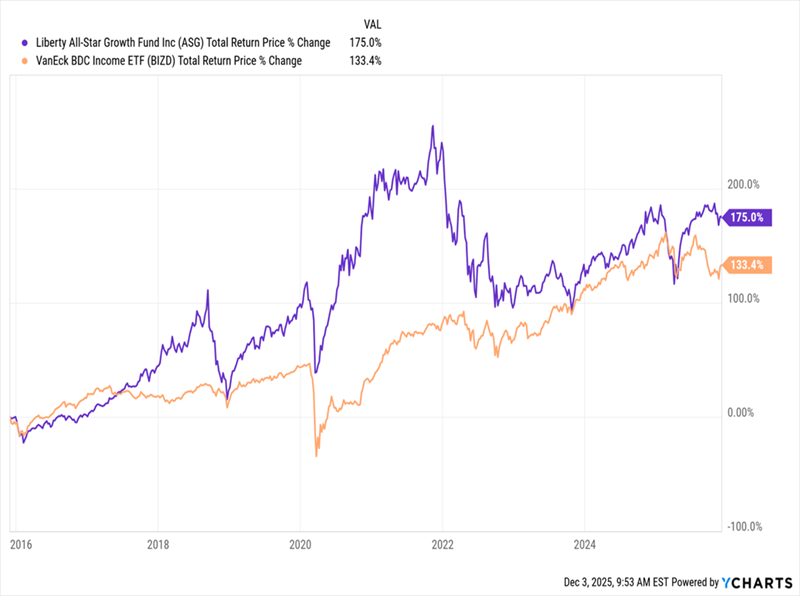

Top CEF Beats BDCs (and It’s Cheap)

In purple above, you see the performance of the 9%-paying Liberty All-Star Growth Fund (ASG) over the last decade. As you can see, it’s outrun BDCs, with a 175% total return. ASG doesn’t loan to companies, preferring instead to go the equity route.

Its portfolio holds S&P 500 mainstays like tech darlings NVIDIA (NVDA), Microsoft (MSFT) and Apple (AAPL), as well as cornerstones of other sectors, such as JPMorgan Chase & Co. (JPM), Visa (V) and Constellation Energy (CEG).

I should mention that the fund’s managers tie its payout to the performance of its underlying portfolio, so the dividend does float a bit. But management commits to paying about 8% of NAV as dividends yearly, so we do have some predictability here.

To be sure, ASG is very different from a BDC. But right now I’d argue it has more upside, thanks in part to its 11.2% discount to NAV, well below the 2.4% discount it’s averaged over the last five years.

With a discount like that, plus a 9% dividend, there’s simply no need to take the risk of “reaching for yield” with PSEC and OBDC. With ASG, you don’t need to reach at all.

Exclusive: My Top 9%+ Dividends for 2026

At CEF Insider, I’ve spent the last eight years recommending CEFs that deliver big yields and price upside—just like ASG.

And with the new year about to dawn, I’m making a rare move: I’m taking 4 top picks from our service’s portfolio and dropping them into a “mini-portfolio for 2026” all their own. These 4 funds are rock-solid dividend generators, kicking out an outsized 9.2% yield, on average.

And thanks to their way overdone discounts (due in part by exaggerated bubble worries), I have them pegged for 20%+ upside next year.

I want to give you access to them now.

I’ve broken down these 4 top picks (and my full CEF investing strategy) in an Investor Bulletin that gives you a free Special Report revealing these funds’ names and tickers. Don’t miss this chance to bulk up your income stream at a bargain. Click here to read more about these top 2026 dividend picks and grab your free Special Report now.