A major AI upgrade just crushed software stocks. We’re going to cash in with two “volatility-loving” dividends paying 7.5%+.

Just days ago, new AI tools were rolled out that let bots make entire apps by themselves. It’s not a big leap from there to the question a lot of people are asking now:

“Why would anyone buy software from a Microsoft (MSFT) or a Salesforce (CRM) if AI can just build for free?”

It’s legit, and it sent these stocks tumbling. It’s frankly hard to know which breakthrough will come next, though financials and office REITs have been pressured in the last couple days.

The takeaway from all of this is that AI is changing by the hour—and it’s rattling a different sector with every iteration.

A Classic “Short-Term Pain, Long-Term Gain” Setup

Before I go further, I should be clear about one thing: This is a massive productivity unlock that looks poised to drive stocks higher.

Fewer humans will be needed, yes. But efficiency gains are only half of the story here. Growth is the other half. Penn Wharton numbers from September forecast a 1.5% boost to GDP between now and 2035, jumping to 3% by 2055 and 3.7% by 2075.

These are permanent boosts to growth. And those numbers are from September—a lifetime ago in AI terms.

Plus we’ve got other reasons to be bullish, too, beyond AI.

For one, as we discussed last week, Treasury Secretary Scott Bessent is making moves that effectively cap long-term interest rates. And 2026 is an election year, so we can expect more cash to flow into the economy.

This setup—a likely rise in volatility in the short term with solid growth in the long run—is perfect for the “matched set” of 7.5%+ dividends below.

Enter the Ultimate Market “Shock Absorber”

Both of these high-yielders are closed-end funds (CEFs) that sell covered-call options on their portfolios. It’s a savvy move that results in far higher dividends for us than we’d be able to get from, say, the typical S&P 500 stock.

Under this strategy, these funds sell, or “write,” options that give the buyer the right to purchase their stock holdings at a fixed future price and date.

If the stock hits that target, it’s likely to be sold. If not, nothing happens. Either way, the fund keeps the fee—called a “premium” in option-land—it charges for the option.

And that boosts these funds’ (and by extension, our) payouts. This strategy, as you can probably tell, does best in volatile markets.

What’s more, between them, these two funds hold the stocks in the S&P 500 and the NASDAQ, so we don’t even have to give up our current holdings to get these 7.5%+ payouts. That diversification also gives us some insulation, as we’ll be spread across a range of stocks and sectors.

Let’s walk through them.

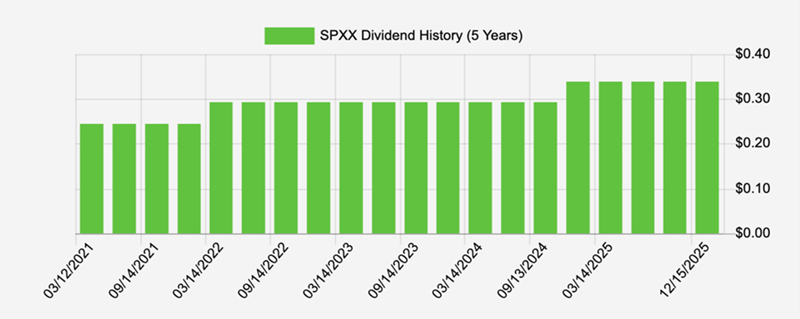

A 7.5% Payer Selling for 8% Off

The Nuveen S&P 500 Dynamic Overwrite Fund (SPXX) sells options on 35% to 75% of its portfolio, and the premiums it collects drop straight to its 7.5% payout, which has risen 25% in the last five years.

A Growing 7.5% Payout

Source: Income Calendar

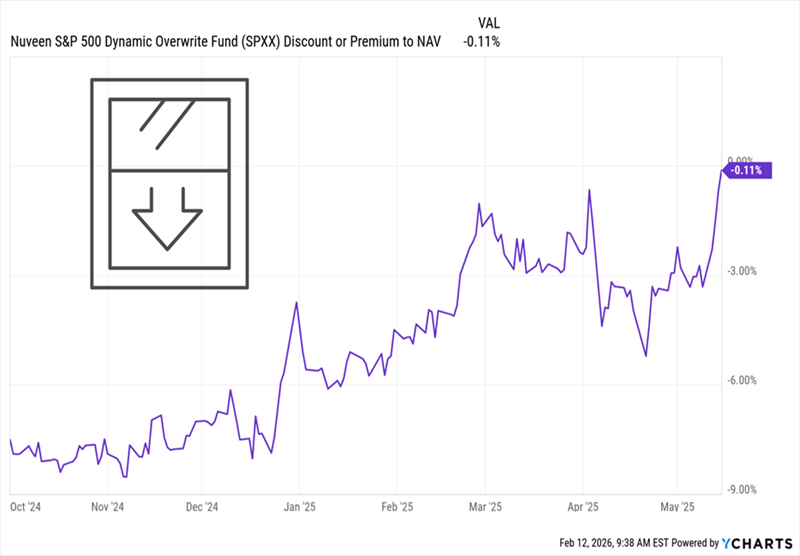

Now let’s talk about the discount to net asset value (NAV, or the value of the fund’s underlying portfolio), because it’s key to our buy case here.

As I write this, SPXX’s discount sits at 8%, near a low not seen since October 2024. How did a buy back then play out? In the seven months following that time, SPXX’s discount shot from around 8% to just 0.1%—near par, in other words:

SPXX’s “Discount Window” Slams Shut …

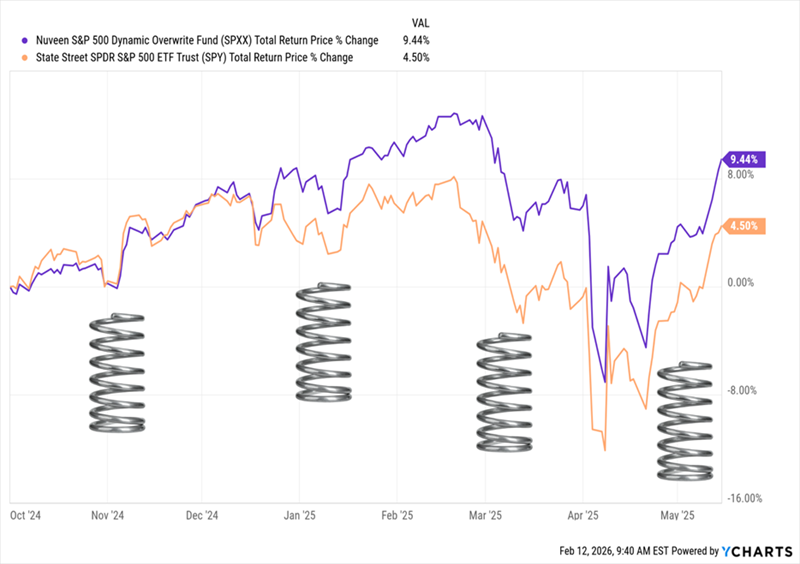

In just seven months, that closing discount pushed the fund’s total return to 9.4%, doubling up the S&P 500 (in orange below):

… Spiking Its Return, and Cushioning the “Tariff Tantrum”

That’s a big move for a covered-call fund. Note also that SPXX didn’t fall as far as the S&P 500 during the April “tariff tantrum,” and recovered far more quickly, too.

This is exactly what this fund is designed to do, and it’s why it stands out in uncertain times. Same with its “sister” CEF—an 8% yielder that’s even cheaper now.

“Software Shakeout” Gives Us a Special Deal on This 8% Payer

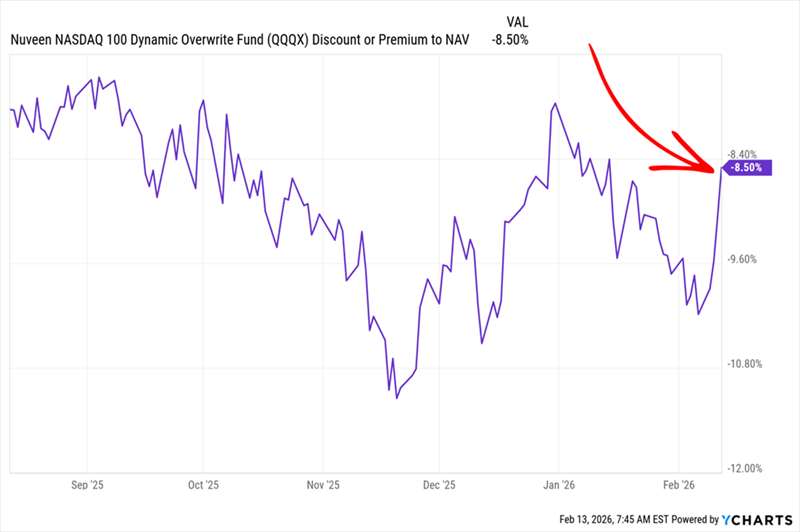

The companion to SPXX, the NASDAQ-holding Nuveen NASDAQ 100 Dynamic Overwrite Fund (QQQX), pays that 8% dividend and trades at an 8.5% discount.

That, again, is almost triple the fund’s five-year average discount of 3.1%.

In other words, just a reversion to that level amounts to a 3% gain in the share price, to go along with that healthy 8% payout—a potential total return of 11% in a year.

And that’s before additional upside from the fund’s tech-focused portfolio. That’s likely, as AI unlocks productivity both within tech (due to fewer human developers needed to build apps) and in sectors of the economy beyond Silicon Valley.

This, by the way, neatly sums up why we love CEFs in general—namely that they have three ways to pay us:

- Through their high dividends.

- Through their closing discounts, and …

- Through portfolio gains.

But I digress. Back to QQQX, whose discount is giving us a particularly timely buy window now:

QQQX’s “Discount Momentum”

If you look at the right side of the chart above, you see that QQQX’s discount is still wide but is arcing back toward par. That makes sense, as investors look to the fund to tame their portfolio’s volatility while still looking for exposure to AI’s efficiency gains.

This “discount-with-momentum” setup is also a smart time to make a move into QQQX. And if we do get more short-term volatility (again, likely), I expect QQQX to move back to (and beyond) its five-year average of 3.1% even faster. That means this 8.5%-off deal is likely on borrowed time.

This 11% Dividend Crushes SPXX and QQQX—and Loves 2026 Chaos

Funds like QQQX and SPXX do help smooth volatility, thanks to their savvy option strategies. But I’ve got another fund for you that’s even better.

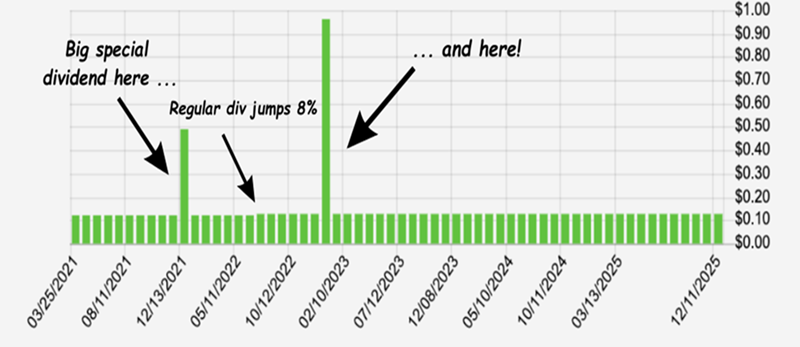

It’s overlooked. It holds a smartly built bond portfolio set to gain as rates fall. And it yields a stout 11% (with dividends paid monthly).

Take a look at this soothing payout chart:

That’s exactly the kind of payout we want in times like these: high, reliable, monthly paid and sporting potential for growth, too.

Moreover, this 11% payer is run by one of the best bond managers in the business. That’s another way it’s purpose-built for times like these, when we want a deft-handed pro with deep connections running our bond holdings.

Discounts on funds like these tend to vanish as volatility ticks higher and investors rotate out of growth stocks and into reliable sources of income like this. I don’t want you to miss your chance. Click here and I’ll introduce you to this “ironclad” 11% payer and give you a free Special Report revealing its name and ticker.