There’s one critical takeaway for us as AI flits through the market, whacking sector after sector as it does:

Actively managed funds—closed-end funds (CEFs), in particular—are the best way to play it.

Funds with human managers are often viewed as dinosaurs by the AI crowd and those obsessed with low-fee ETFs, but they shouldn’t be. Because when it comes to investing in a sector as complex, and fast-changing, as tech, we need an insider in our corner, spotting, and moving ahead of, the next shift before it hits.

I’m talking about a real person who talks to other pros in the business and uses their own personal tech background to get at the insights others miss.

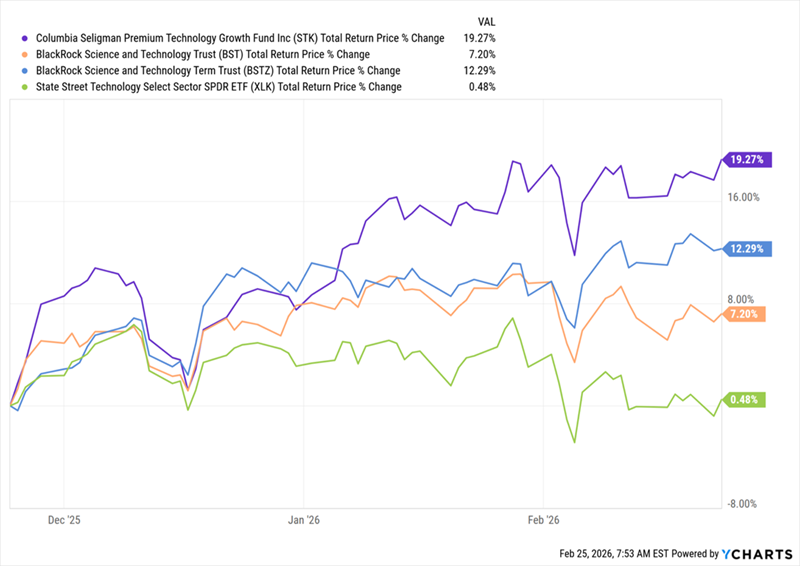

That was the first thing I thought of when I looked in on the three tech-focused CEFs in our CEF Insider portfolio a few days back: the BlackRock Science and Technology Term Trust (BSTZ), BlackRock Science and Technology Trust (BST) and Columbia Seligman Premium Technology Growth Fund (STK).

Over the last three months—a tough time for tech, especially on the software side—all three soundly beat the State Street Technology Select Sector SPDR ETF (XLK), a decent proxy for the sector as a whole.

It wasn’t particularly close, as you can see below, with STK leading the way (in purple) followed by BST (in orange) and BSTZ (in blue).

“Human-Run” CEFs Beat the Index—Handily

That’s a pretty clear snapshot of the power of these funds’ management teams doing their due diligence, taking soundings of the sector as a whole and applying those to get out ahead of the two rotations happening throughout tech now.

That’s right: The overdone panic in software-as-a-service (SaaS) stocks isn’t the only shift hitting the sector (though we will talk about that one in a bit).

The other is much more important: The shift in the discussion around AI as a whole, from whether the tech is in a bubble to a much more mature dialog around not if it will produce gains for the economy, but just how big those gains will be.

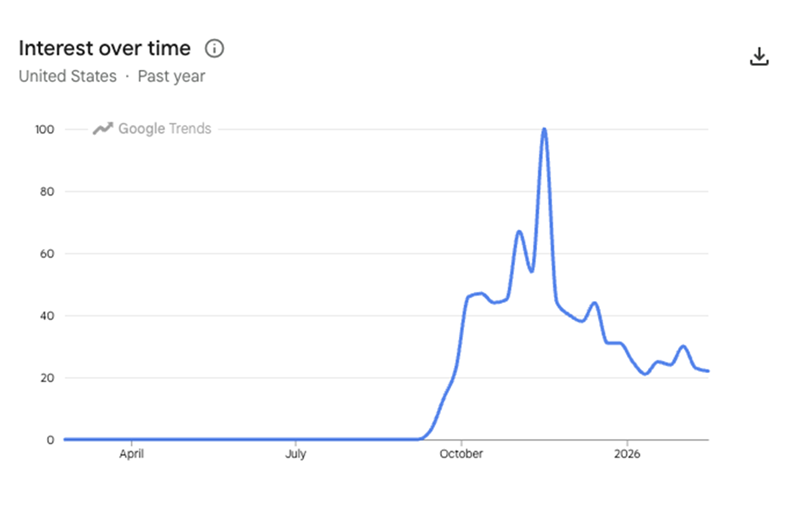

It’s a shift we welcome, and we can see it happening in real-time through one very public indicator:

The Bubble in AI Bubble Talk Bursts

This chart shows the popularity of the topic “AI bubble,” according to Google Trends, and you can see how there was a bubble in bubble talk until Thanksgiving, when it suddenly dropped off sharply.

That’s great news for us, as it shows the crowd is finally coming around to the more reasoned point of view we’ve held at CEF Insider since we started discussing AI way back in 2020.

The other shift is a move we’re taking a contrarian approach to now, however: Investors’ pivot away from software stocks and into areas like chipmakers, semiconductors and hardware suppliers.

That’s being driven by the release of new AI tools that have raised fears that any single person, with no coding experience, can create their own apps, potentially cutting the need for companies like Microsoft (MSFT) and Salesforce.com (CRM).

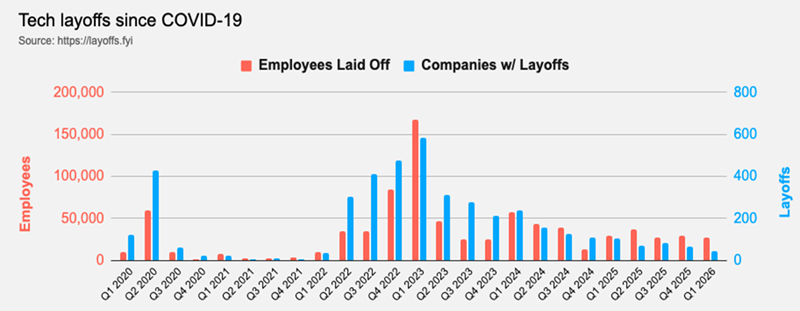

The flames are being fanned by the media, of course, which is piling on, reporting that job losses in the tech sector are the canary in the coalmine for this shift.

But is that really the case? I mean, if AI really were going to replace these companies, we’d be seeing it show up in the form of layoffs, right?

That’s not showing up in the data—yet, anyway.

Data from Layoffs.fyi tells us that the number of layoffs in the tech sector is actually falling from what we saw in 2022 and 2023, and the trend seems to indicate that there is not a significant decline in demand for labor from the sector.

In other words, the data says the opposite of the fear mongering that’s rattling the markets today.

Back to the ’90s

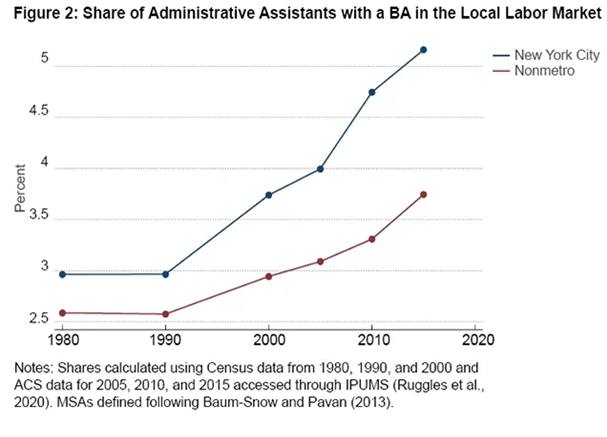

There’s one reason why jobs are not disappearing even as AI gets better: Technology has a long history of creating jobs. And that’s what I expect to see as the tech sector grows—and incorporates AI—in the months and years ahead.

When the computer became a major part of businesses in the 1990s, you may recall that, back then, fears circulated that computers were going to kill entry-level jobs. The chart above shows us what actually happened: Computers caused an explosion in administrative-assistant jobs.

My take, based on all this, is that AI is likely to create more jobs than it kills. That’s only one sign that IT workers, and more importantly for us, the SaaS companies that employ them, are likely to be winners, not losers, here.

(That’s in addition to the proprietary infrastructure, information and expertise these companies provide—one “vibecoder” making their own apps simply can’t replace those.)

How to Play Overdone Fears of a SaaS Meltdown

Our three tech-focused CEFs remain great ways to play the SaaS meltdown.

STK, for example, yields around 4.6% now. That is a bit lower than the average CEF, which pays around 8%, but the fund makes up for that with its strong total return, as we saw off the top.

We also like STK for its top-flight management team. CIO Paul Wick has a 12-person squad to manage all of Columbia Seligman’s tech funds. The team leverages Paul’s tenure (he’s been managing tech funds for 30 years) and its analysts’ expertise to make its picks.

Unlike the teams at many other funds I’ve interacted with, what impressed me most about the STK team is that they focus on the long term and the bigger picture, while tuning out short-term noise.

For instance, they like to talk about exactly how AI will change the modern media landscape, rather than get sidetracked into AI-bubble talk.

This team knows where growth is and, most importantly, knows whom to ignore in their focus on capturing it. Right now, the top holdings focus more on hardware firms like NVIDIA (NVDA), Broadcom (AVGO) and Marvell Technology (MRVL). But it does have some software exposure in the form of Alphabet (GOOGL) and Microsoft.

That’s a good place to be for the fund, as it leaves it more room to pick up bargain-priced software stocks.

The fund’s discount to NAV has narrowed some, to around 3.6% as I write this. That’s a good deal on this fund, which has averaged a 2.9% premium over the last five years. And when you consider its savvy management team and the bargain on SaaS stocks right now, that deal looks even better.

My 4-Fund AI Portfolio Is a Prime Buy Now (and Set to Bounce)

We love that STK is weighted toward hardware because, as I just pointed out, that gives it lots of room to pivot to software stocks now that bargains abound in that space.

But as we also touched on, its discount could be deeper. So we’re going to patiently wait for the next dip before picking this one up.

However, that doesn’t mean we have to be entirely on the sidelines. Because CEF-land being what it is, there’s always a bargain somewhere. And in this case, it’s in the 4-fund portfolio I’ve specifically built to tap the AI boom.

This collection of funds yields much more than STK now—a rich 9.3% as I write this—and thanks to this overdone SaaS selloff, their discounts are wider than they were just a few weeks ago.

That’s our time to strike—and pick up this 4-buy portfolio of the top AI developers and companies increasingly using the tech in their businesses—while we can still do so at a bargain.