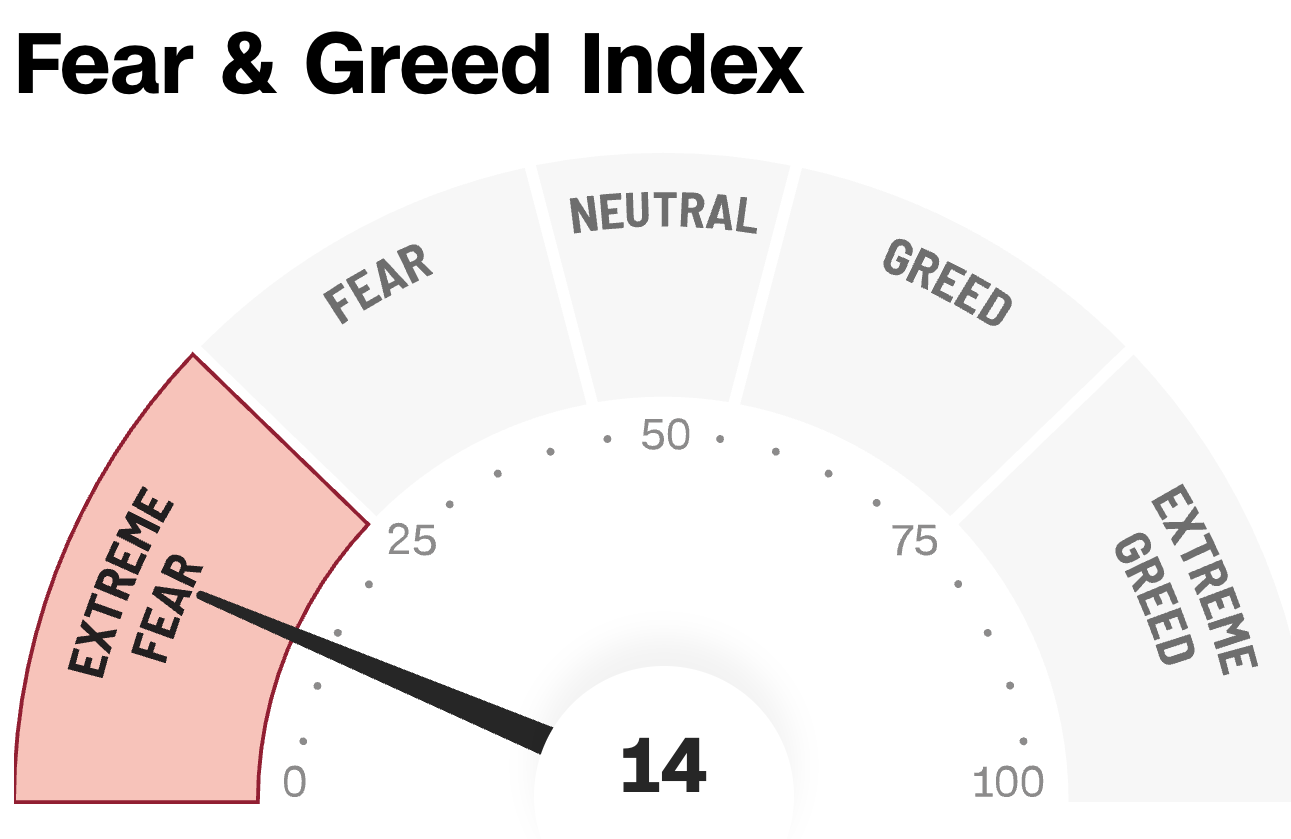

I know uncertainty is the word on everyone’s mind these days, but is this level of terror actually justified?

Source: CNN

Short answer: Nope.

In fact, we contrarians are more nervous when our CNN Panic-O-Meter hits “Extreme Greed!” Times like these are when we go shopping. And closed-end funds (CEFs) throwing off 8%+ dividends are a great way to do it, since many are in the bargain bin as we speak.

We’ll talk two tickers (paying dividends north of 10%) in a sec. First, here’s what the mainstream crowd is missing—and why it’s teeing up these 10% income opportunities.

First, the Iran War has thrown AI off the front pages—and once again, the crowd is overlooking just how much this tech stands to “amp up” productivity (and profits!).

It’s already happening.

Take the latest stats from FactSet, which released its earnings projections for the just-completed Q1 on March 27. In all, they’re calling for 13% growth. That would be the 11th straight quarter of growth and the sixth straight in double-digits.

And it pales in comparison to what they see for the full year: 17% profit growth. Seventeen percent!

Every day, we hear more and more cases of AI driving real profits (including at my own software business, where I’ve been able to cut costs by 70% while growing revenue).

In other words, the ’bots are a two-stage rocket for stocks, boosting growth on one hand, while capping spending (and by extension interest rates) on the other.

And the market is pricing stocks, and CEFs that hold them, as if none of this is happening.

Which brings me to those two 10%+ paying CEFs. The current panic has made both—one focused on stocks and the other on bonds—bargains. But their current discounts price in a far worse situation than we’re likely to face.

CEF #1: A 10.7% Payer With a Discount in Disguise

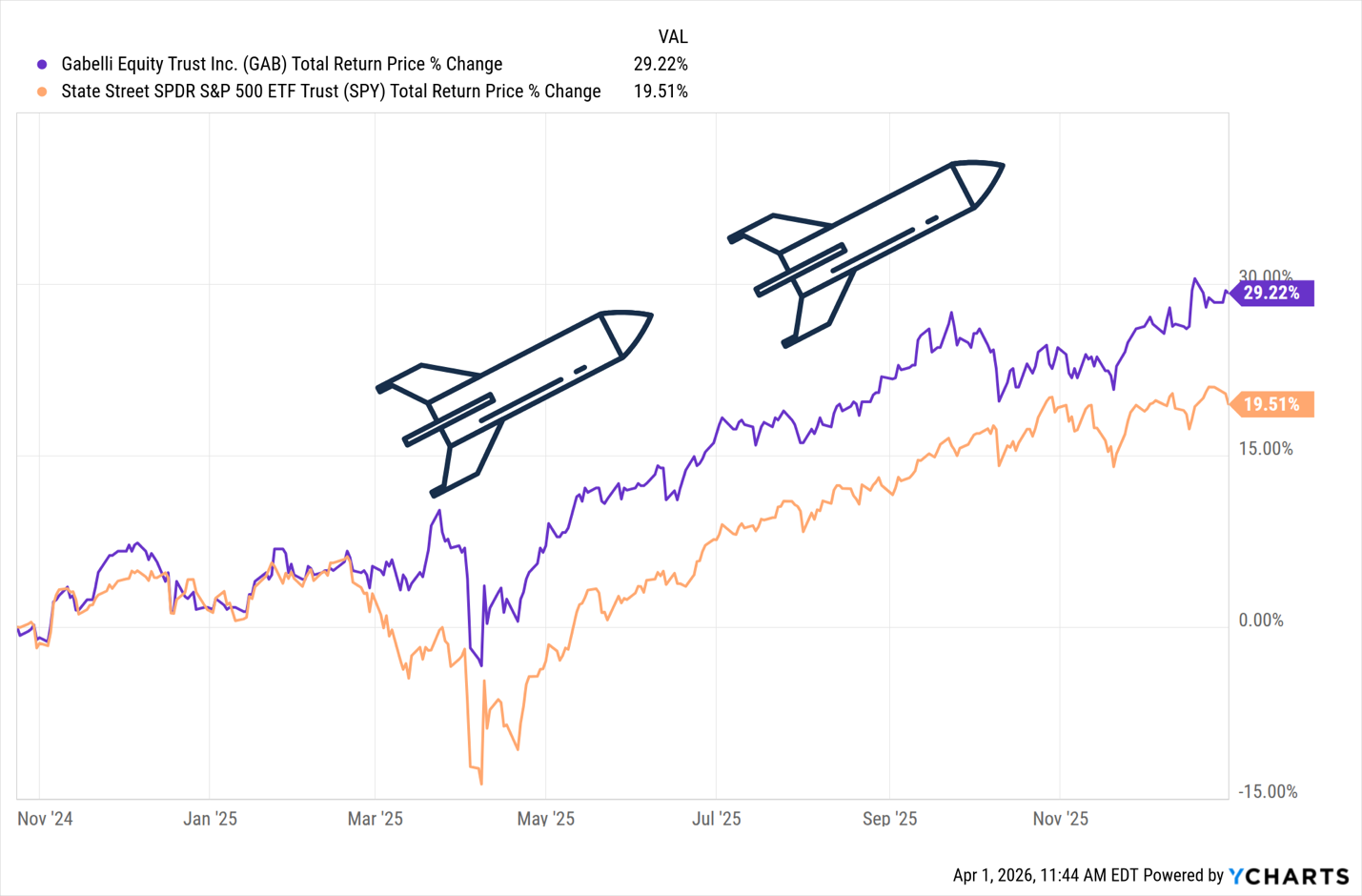

The Gabelli Equity Trust (GAB) doesn’t look cheap at first glance, trading at a 0.9% premium to net asset value (NAV). Here’s why that’s misleading: Over the last five years, GAB has averaged a 7.1% premium—far higher than today’s level.

The last time GAB’s premium got this low was in late October 2024. If you’d bought then and held till the premium peaked north of 11% on December 31, 2025, you’d have bagged a tidy 29% return, way ahead of the S&P 500:

GAB’s Premium Surges, Inflates Its Return

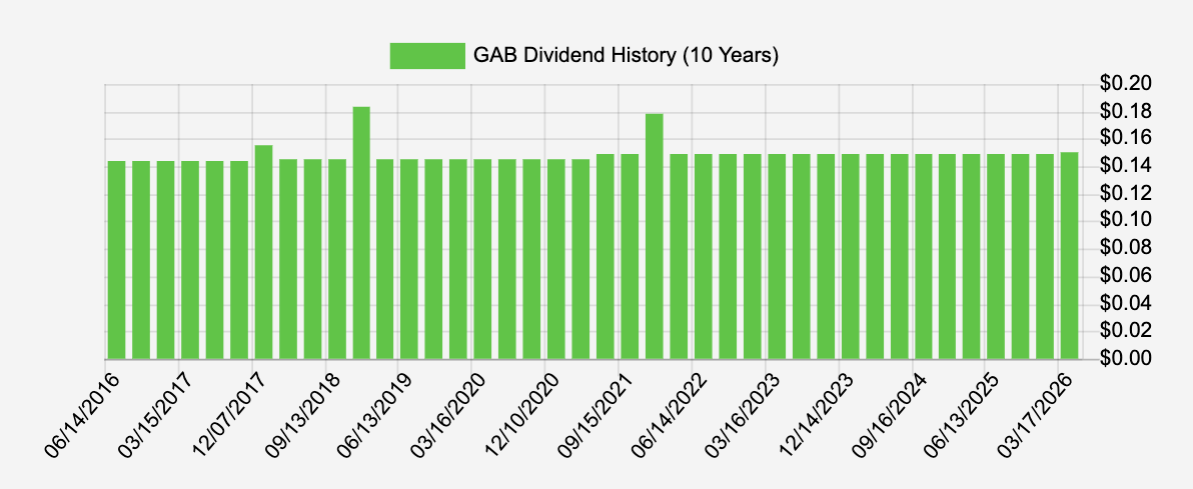

What’s more, the fund’s dividend (which yields 10.7%) has been growing, and GAB has dished out the odd larger-than-normal payout (the longer lines in the chart below):

GAB Taps Well-Known Stocks for a Growing 10.7% Payout

Source: Income Calendar

Beyond the “deal” on the fund itself, we’re getting a bargain on its holdings, which are proven cash flow generators caught up in this quarter’s chaos, including MasterCard (MA), American Express (AXP) and waste manager Republic Services (RSG).

One last thing: GAB is in the midst of a rights offering as part of its 4oth anniversary. Under the deal, existing shareholders get rights that let them buy more shares of the fund at $5 each—below the current price.

New shareholders can’t get on this, but the offering is no doubt weighing on GAB’s share price. Once it passes, that pressure is likely to reverse, as it has with other CEFs in the past.

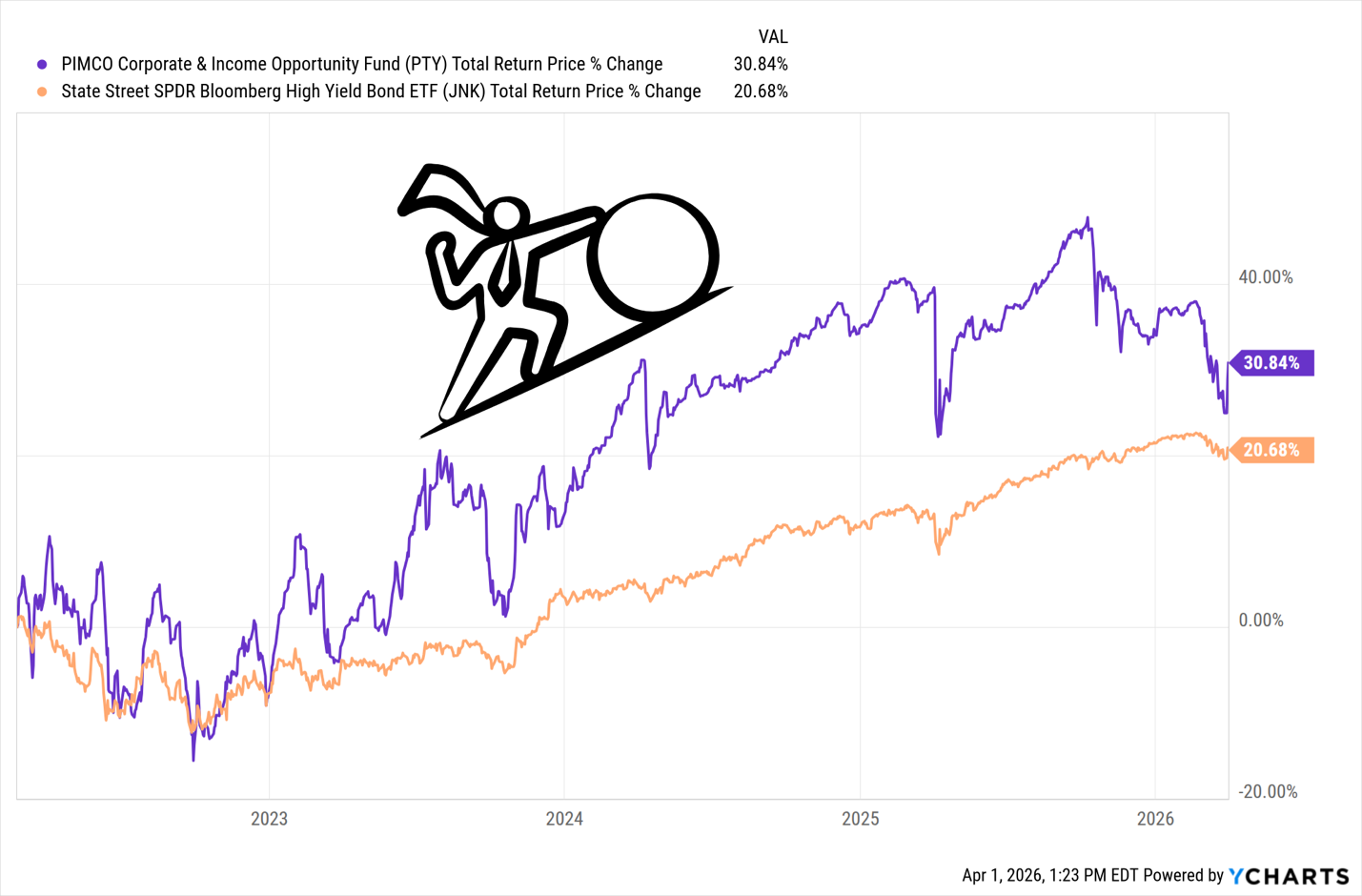

CEF No. 2: an 11.7% Payer That’s Cheaper Than It Was in 2022

We last discussed the PIMCO Corporate & Income Opportunity Fund (PTY) a couple weeks back: in a March 17 article. I bring it up now because the fund’s “hidden” discount (in the form of a 6.5% premium at the time) has slipped to 5.6%.

That’s cheaper than PTY was during the 2022 inflation panic—when CPI hit 9%! No forecast has us anywhere close to that this time around.

Like GAB, PTY usually trades at a premium, and a wide one: Over the last year, that premium has averaged around 14.8%, way above today’s level. (If you’re wondering why the premium exists at all, it’s because PIMCO, founded by legendary bond investor Bill Gross, has long had a grip on investors’ imaginations.)

One reason why the fund’s premium has shrunk is likely because of the long effective maturity on its credit assets: just under eight years. That’s important because longer-duration bonds fall when rates rise (something the current crisis is fueling fears about) and do better when rates fall.

But even if rates do rise, it’s more than priced in.

The crowd is also ignoring PTY’s effective leverage-adjusted duration of 3.8 years. That positions it for gains on lower rates without adding too much risk if rates rise.

And as with GAB, the power of buying at a low premium like this is clear. If you’d gone counter to the crowd and bought PTY at the depths of the 2022 panic, you’d be up a solid 31% today—a big move for a bond fund and well ahead of the benchmark State Street SPDR Bloomberg High Yield Bond ETF (JNK):

The Power of Buying a Discounted CEF

Reinvested dividends drove most of that return, thanks to PTY’s huge monthly payout.

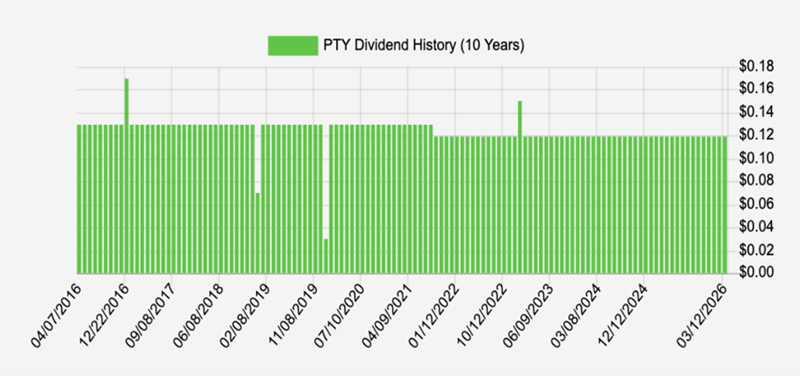

A Reliable Double-Digit Divvie

Source: Income Calendar

Despite a slight cut during COVID, PTY’s payout—11.7% as I write this—has held steady for years. And besides, its regular special dividends (the spikes and dips shown above) have gone a long way toward making up for that cut.

I expect that to continue as the wind shifts toward lower rates, inflating PTY’s premium back to its usual double-digit level. That could happen fast, especially with a steady 11.7% payout in play.

The One Income Plan Built to Pay $40K+ in Dividends (It’s on Sale Now)

If you’ve been reading my articles for a while, you know I’m a fan of a “dividends-only” retirement.

The goal? Simple: Build a dividend stream that covers your bills. Then you can sit back, collect your payouts and ignore market storms like this one.

Most people think this is impossible. They look at the sad yields on the typical S&P 500 stock and think they’ll never save enough to make it happen.

That’s a mistake. The two CEFs we just discussed prove otherwise. With 10.7% (and up) dividends, they show it doesn’t take millions to generate real income.

That’s the foundation of my $500K “Dividends-Only” retirement portfolio. It’s a simple mix of “battleship” stocks and funds built to kick out real income: $40,000, $50,000 or more in dividends every year.

The Iran panic has made this portfolio cheaper, but that won’t last: As AI ripples through the economy, capping wages and dragging down rates, big, steady dividends like these will only get more valuable. That’s why we need to move now.