Hands down, one of the biggest retirement risks I’ve come across is when investors try to play it safe.

That’s because, in hiding out from volatility, they stunt their returns and end up locked into the workforce for years longer than they need to be.

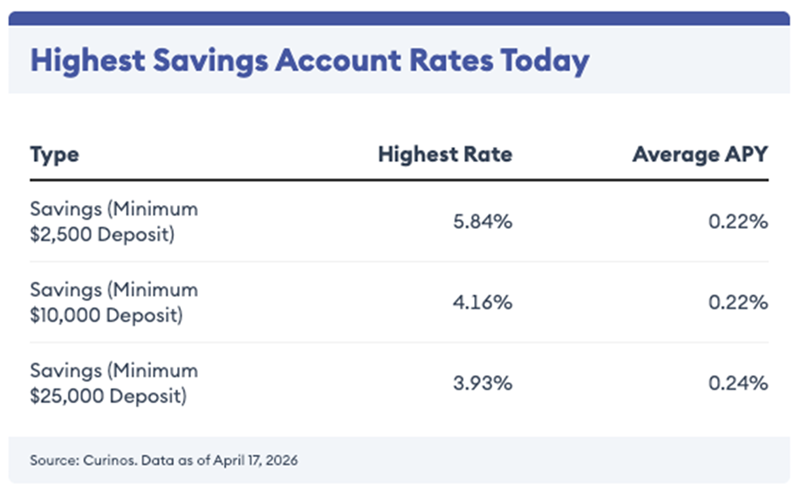

Worst thing is, many of these “safe” options sport high yields that never deliver in reality. Consider a savings account:

Source: Forbes Advisor

To be sure, the highest rates can look appealing, like the 5.8% here. But in reality, larger balances earn closer to 3.9%.

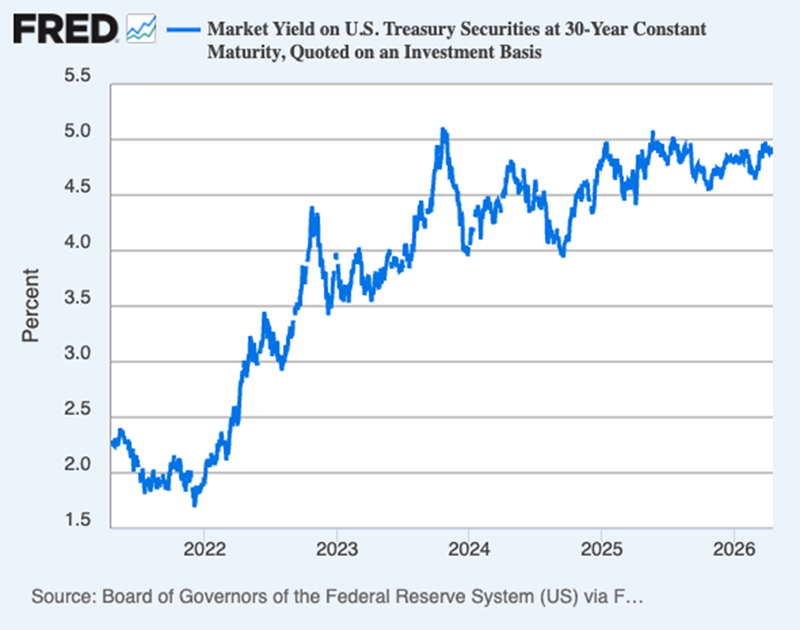

You can do a little better with a 30-year Treasury, which yields around 4.9% now. But here again, there are risks that can push financial independence out of reach.

Locking in Almost 5% for the Long Haul

First, you’ll need to keep your money tied up for 30 years to get that return. If you need to sell early, you could lose money, including giving back all you earned in interest, and more. The bond selloff of 2022 is a good example of a precarious time to have to sell a bond.

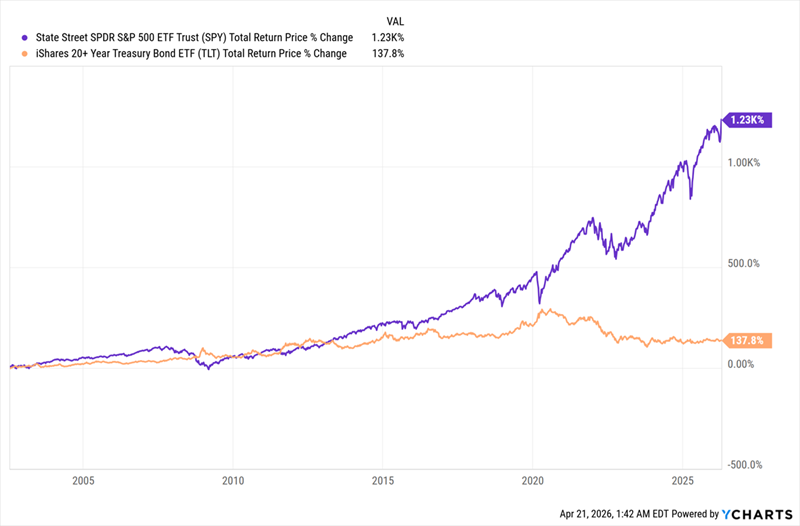

And that’s not even the biggest issue I see here. A 5% annualized return is actually pretty poor, relatively speaking. Check out this chart.

Stocks Crush Bonds

In orange above, we see that over the last 24 years (which is as long as the two funds shown above have been around), the iShares 20+ Year Treasury Bond ETF (TLT), composed of long-term Treasury bonds, has returned about 3.7% annualized.

Meanwhile, an S&P 500 index fund, the State Street SPDR S&P 500 ETF Trust (SPY), in purple, has returned 11.4% annualized. In other words, $10,000 put into Treasuries in 2002 is now worth about $23,780. The same $10,000 in stocks? $133,250.

This Matters More Than You Think

Obviously, having $133,000 is better than having $23,000. But this isn’t just a matter of getting richer. It’s also a matter of getting to retire at all.

Source: CEF Insider

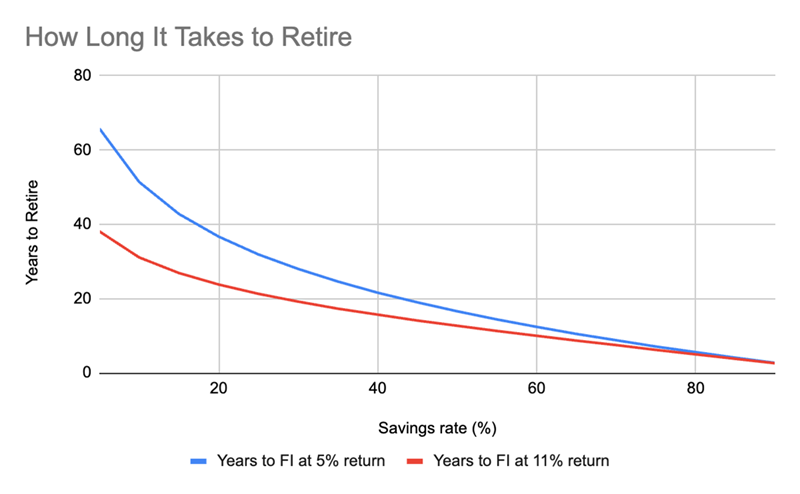

Above we can see how long it would take an investor to hit financial independence if they received a 5% yearly return (in blue) and an 11% annualized return (in red). With either asset class, someone who saves to an extreme (like 90% of after-tax income), there’s not much of a difference; our investor would retire in 2.6 years instead of 2.7.

But of course, no one saves that much. Let’s look at a more realistic savings rate of 20% of after-tax income. In that case, being too risk-averse adds a full decade to the time you’d need to achieve financial independence.

Most Americans save a lot less than that still, of course. In fact, the average savings rate is now 4%, and not all of that is going to retirement. But if it were, that would mean a difference of around 30 years between an investor getting 5% annualized and one generating an 11% yearly return. It also means anyone starting to save at, say, 20 won’t have enough money to retire until their late 80s.

That’s obviously unrealistic, and clearly shows that being too conservative is, in fact, a very real risk.

The Lower-Risk Higher-Return Option

The lowest-risk way to get a better than Treasuries return is, of course, the stock market. The S&P 500 has averaged over a 10% return for over a century, and buying stocks is a way to get a higher return and have enough for retirement.

But, as we saw earlier this year, stocks can crash in the short term, raising the risk of a retiree having to sell into a downturn to get the cash they need.

Fortunately, there’s an asset class out there that can get us around that risk: a closed-end fund (CEF) that invests in stocks and pays a high dividend yield.

A good example is the Liberty All-Star Equity Fund (USA), which yields 10.3% as I write this. In other words, USA pays out a large share of the market’s long-term annualized total return in cash. That’s a big plus in a volatile market like the one we’ve been living with lately.

Moreover, USA holds some of the strongest companies in America: NVIDIA (NVDA), Microsoft (MSFT), Alphabet (GOOGL), Visa (V) and Capital One Financial (COF) are all top positions.

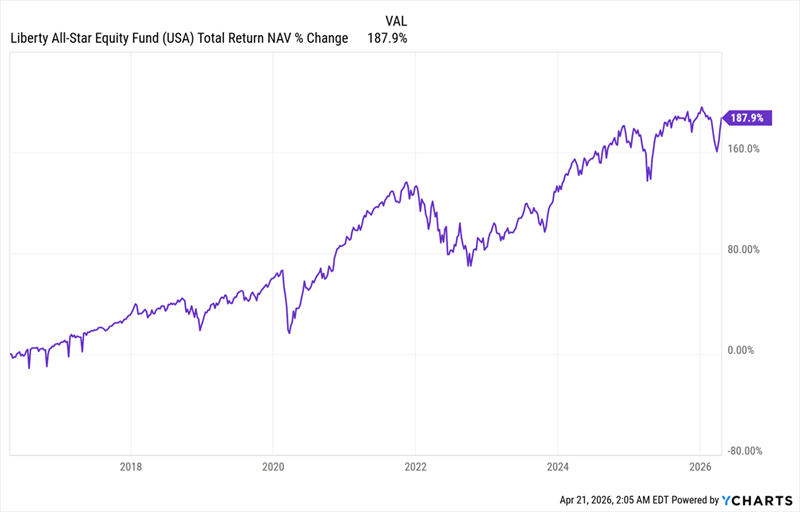

USA Delivers a “Retirement-Saving” Return

Here we can see that USA has posted a strong return over the last decade—11.2% on an annualized basis. Moreover USA’s high dividend (currently around nine times the payout on an S&P 500 index fund) means the bulk of that return was in dividend cash.

In other words, USA investors don’t have to worry about timing their sells to get the cash they need. And if they didn’t need the dividends, great. They could have reinvested them and bought more shares of USA—boosting their income as they did.

One thing to note is that USA’s payout isn’t fixed. Instead, it’s tied to the fund’s NAV, though management does commit to paying 10% of NAV as dividends, putting a floor under the dividend.

That strategy is actually a plus for shareholders, as it turns market gains into cash without forcing them to sell. Moreover, in down years, it gives management flexibility to pick up bargains.

Finally, this fund is cheap, trading at an 11% discount to NAV now, far below its five year average of a discount of less than 1%. That’s simply too big of a gap to last.

Do This to Unlock 60 Dividend Payouts a Year (at a 9.3% Yield)

We can actually go one better than USA here, with CEFs that pay dividends just as high, but pay us in fixed monthly amounts.

That’s right, monthly. Few people realize it, but the majority of CEFs pay every month, not every quarter like the typical stock does.

I think you’ll agree that a setup like that—a high yield with predictable monthly payouts—is ideal, whether you’re saving for retirement or have already clocked out.

To help you start your own high monthly income stream, I’ve published a free Special Report revealing my top 5 monthly payers to buy now. They pay 9.3% on average and, if you hold them all, you’ll grab 5 dividend checks from this “mini-portfolio” every month.

That’s 60 dividend payouts a year! And with a 9.3% yield, you’re getting most of the market’s historical return in dividend cash, as we just saw with USA.

Plus, these 5 funds trade at deep discounts now, which will help drive their prices higher as these markdowns revert to their normal levels.

Everything you need to get started is waiting for you now. Simply click here and I’ll introduce you to these 5 monthly payers and give you your own copy of that free Special Report, which reveals their names and tickers.