Monthly dividends and panic readings? Now that’s a path to profits.

Two weeks ago, my Contrarian Income Report readers and I were staring at a recent decline in DoubleLine Yield Opportunities Fund (DLY). Buy more, hold or sell? DLY owners were understandably jumpy. Something must be wrong with the bond portfolio itself, right? Why else would it be down?

The bond fund had just registered its deepest panic reading—which I will share with you in a moment—since we’ve owned it. My contrarian gut said buy. Always buy the hysteria. But, I admit, my taste isn’t for everyone.

(“Dad, why are you buying sardines with tomato sauce?” My oldest winced in the grocery checkout line last Friday, an “early release” day from school. That’s your lunch, I deadpanned, receiving approval and two thumbs up from our smiling cashier. Contrarians feast when normies wince.)

What did the numbers say we should do with DLY? Let’s look at our playbook, which we run to target double-digit total returns from monthly dividend payers like DLY.

DLY or “Dilly,” as those inside the building call it, is run by the “Bond God” Jeffrey Gundlach. His fund invests across the global bond universe—mortgage-backed securities, corporate credit, emerging market debt—wherever Gundlach finds value. DLY has paid its monthly distribution without interruption since its 2020 inception. (That monthly $0.1167 per share adds up to $1.40 per year. A double-digit yield just two weeks ago!)

Careful readers pointed out that DLY’s distribution isn’t currently fully covered by net investment income (NII). About 16% of the payout is classified as return of capital—cash in DLY’s checking account. This is not a red flag. CEFs use leverage, borrowing money to invest for higher yields. With short-term rates still elevated, Gundlach’s borrowing cost is pinching net income.

When oil prices calm down and corporate AI rollouts further compress wage growth, I expect the Federal Reserve to cut rates again. (How’s that for a hot take?) Borrowing costs fall, NII coverage improves and DLY’s bond portfolio rises in value. A triple play.

Good manager, monthly dividend, 10% yield, all set to benefit from the next leg of Fed cuts.

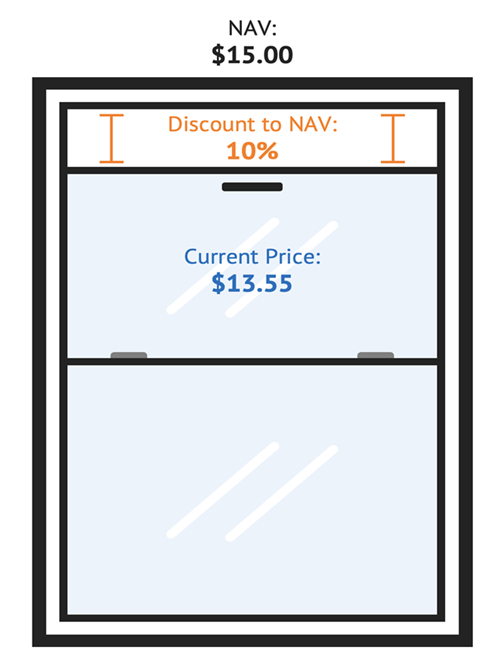

Oh, and the discount! Two weeks ago, DLY was trading at a generous 10% discount to its net asset value (NAV), meaning the bonds DoubleLine handpicked were selling for 90 cents on the dollar. Not a bad margin of safety! Plus, we had a nifty catalyst for price upside. DLY’s price would increase when the panic subsided and investors no longer demanded a discount.

DLY Sold at a Big Discount

And lo and behold, we know today that DLY was indeed about to rally!

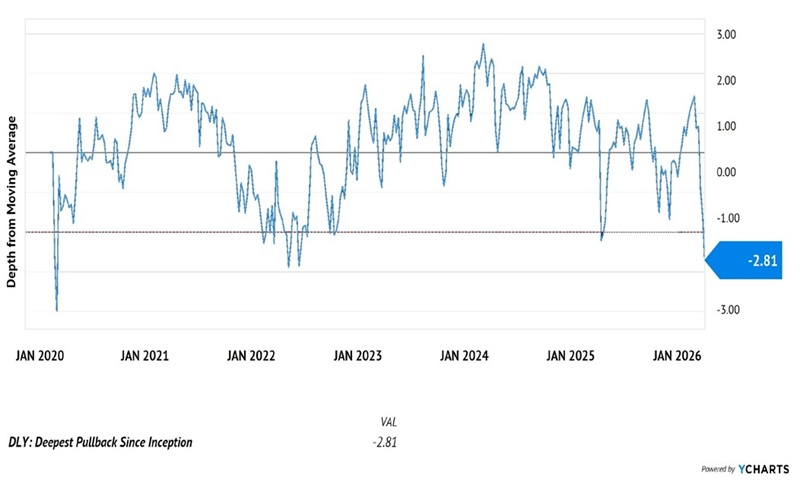

So, how to know we were in deep panic mode? I ran the numbers on every instance in which a major taxable bond CEF like DLY hit this level of pessimism. A great pessimism gauge is how far below its long-term moving average a fund trades.

Moving averages (MA) are, well, averages. They take the average of numbers over a moving period of time, such as the last month, months, year, or more. A common moving average is the 200 day, abbreviated as 200 DMA. This calculates the average price daily for the last 200 days.

The MA tells on average where we expect a stock or fund to be trading at a given moment, though prices are rarely average. But over time, the more a price is higher or lower than the average, it “reverts to the mean”—goes back to average. We can say that a moving average is like a “rubber band” that pulls the price back to reality periodically.

Bond CEFs are especially sensitive to distortions. Most of the time, they trade within one standard “depth” (one unit of normal volatility) of their moving average, reverting to the mean in between moves.

Sometimes, however, they are pummeled even lower by panics, stretching these rubber bands so much they have no choice but to snap back up! They are—wait for it!—way out of their depth.

So, two weeks ago, DLY had just registered its deepest “panic reading” since we’ve owned it. Here were the eight previous historical instances—every time a comparable bond CEF reached this depth of more than two units of normal volatility—and what happened over the following five months:

When Bond CEFs Hit This Level of Pessimism: All 8 Instances

A 75% batting average is excellent. The eight buys averaged +17.3% over five months—and that includes two small losses from the 2022 rate-hike cycle dragging the number down. That’s over 46% annualized. Not bad returns from “boring” bond funds!

And the two “losses”? Both came during the 2022 rate-hiking cycle, when the Fed was raising rates at the fastest pace in forty years, a very different environment from today’s stable to falling rates. But here’s the thing—even those two entries weren’t disasters. PDO, which showed -7.3% at five months, returned +19.8% over the following three years. GDO returned +8.3%. Both funds paid their dividends every single month along the way. Patient holders did just fine.

Notice that PDI entered at a depth of -2.84 in March 2020—almost identical to where DLY sat two weeks ago at -2.81. PDI returned +16.1%. And PDO entered at -2.80 in October 2023 and returned +29.1%. DLY was trading at the same level where these funds launched double-digit rallies.

We Bought the DLY Dip

So how’s DLY doing? More than fine. The fund is up 4.6% in two weeks. Plus Gundlach has already declared another $0.1167 monthly distribution, payable April 30. That’s a 4.6% total return from a bond fund in fourteen days.

And if the eight-instance history is any guide, we’re barely out of the gate. The average five-month return on this setup is +17.3%. We’ve captured one-quarter of this move in the first two weeks.

And remember, the whole time you’re watching the rubber band snap fully back, DLY is dropping $0.1167 per share into your account every single month.

This is how we retire in style on monthly dividends.

But if you’re reading this, you missed my DLY “buy alert.” Fortunately, there’s a quick fix. Subscribe to my Contrarian Income Report service (on a risk-free trial!) and never miss a Monthly Dividend Best Buy again!