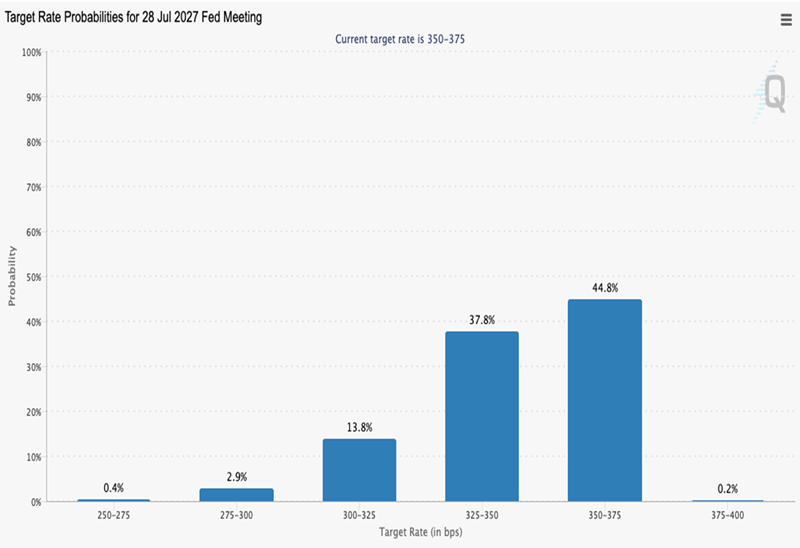

I just took a glance at the Fed futures market and, frankly, couldn’t believe what I saw.

These traders don’t see a rate cut from the Fed until July of 2027. And even then, only a bare majority do:

Source: CME Group

C’mon man! That’s 15 months from now.

I know predictions are tough, but from where I sit, this one seems awfully hard to justify.

For one, Trump administration pick Kevin Warsh is likely to be installed as Fed chair long before then, with Jay Powell’s term officially up next month. Sure, Warsh has been hawkish in the past, but over the last few months, he’s been in line with the administration’s wish for lower borrowing costs.

Let’s be honest. If (when?) push comes to shove, Warsh will choose self-preservation.

But the Fed drama is the least of my reasons for expecting lower rates. A far bigger one is AI, which is cutting headcount, slowing wage growth and, as it does, grinding on inflation.

Goldman Sachs (GS), for example, recently said that AI is wiping out roughly 16,000 jobs a month on a net-net basis, with the bulk of those on the entry-level side of things. That’s after the US added just 181,000 net jobs last year, or an average of just over 15,000 a month.

In other words, the economy added fewer jobs per month than Goldman says AI is wiping out! Wage growth, too, has trended steadily lower since the big raises doled out in the go-go days of 2020 and 2021.

These are all deflationary. And with AI just starting to flow out to the broader economy, I expect wage growth and hiring to stay on the mat, dragging down price growth more. That means it’s time for us to pounce, while the crowd wrings its hands over inflation.

Our play? Bonds! Specifically, good old-fashioned municipal bonds. We’re into these plays now because:

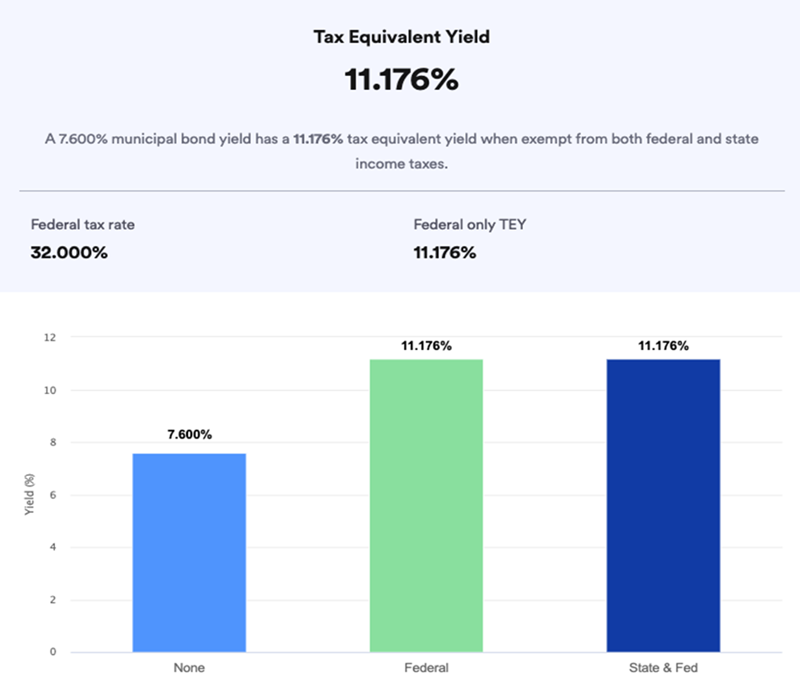

- They pay high (and tax-free) dividends. The fund we’ll discuss next yields 7.6%, and that payout could be worth 11.2% on a taxable-equivalent basis for those in the highest tax bracket.

- They’re relatively safe, with bonds backed mainly by revenue-generating assets. Think vital infrastructure, like toll roads and airports.

- Municipal bonds tend to be long duration. That’s key now, as these bonds’ value has fallen as rates have risen (since newer debt is being issued at higher rates). But their value stands to gain as rates fall (and newer, competing bonds are issued at lower rates).

When we’re looking to add “munis” to the portfolio of my Contrarian Income Report service, we look to closed-end funds (CEFs), specifically CEF manager Nuveen.

The company has been around since 1898 and manages around $1.4 trillion in assets today. It specializes in bonds, infrastructure and real estate, and its performance is proven. The Nuveen Municipal Income Fund (NZF) has been a staple of our portfolio since April 2023, and it’s returned about 30% in gains and reinvested dividends for us since. That’s a big move for a “boring” fund like this.

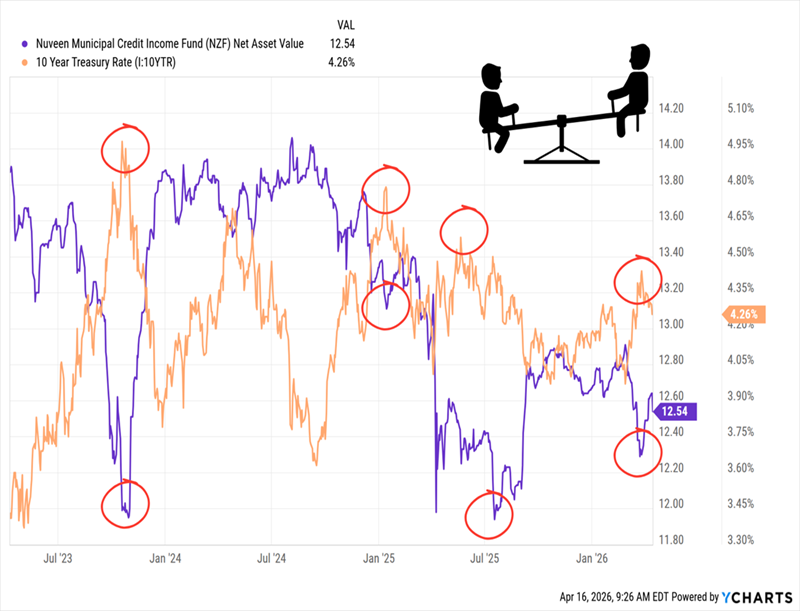

Funny thing is, this return came as the fund’s net asset value (NAV, or the value of its underlying portfolio—in purple below) declined, weighed down by the rising 10-year Treasury rate (in orange)—pacesetter for the real interest rates we all pay on our loans:

NZF’s NAV/Interest-Rate “Teeter-Totter”

Another thing to note here is the inverse relationship between NZF’s NAV and interest rates: When rates jump, NZF’s NAV falls (and vice versa). That overall trend toward higher rates cut the fund’s discount to NAV from roughly 14% when we bought to around par today.

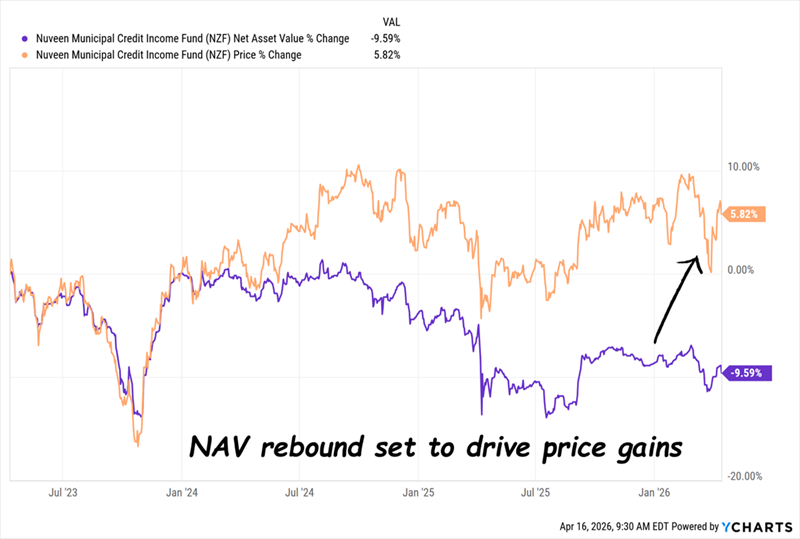

That might make it seem like we’re too late here, but we’re not. A look deeper shows that the fund’s narrowing discount is not the result of investors suddenly catching on to our argument that AI will erode inflation and piling in. The fund’s price (shown in orange below) is only up around 6% in that three-year period.

Instead, it’s that falling NAV (again in purple below) that’s wiped out the discount:

NAV Drops, Price Holds Steady

Now that NAV drop looks set to reverse, setting up a nice entry point.

As AI slows wage growth and pulls down inflation, the Fed will cut, putting downward pressure on Treasury rates. As that happens, NZF’s NAV will rise (rates down, NAV up, remember), priming the fund for a premium—and the price growth that goes with it.

Another reason to be bullish? That long duration I mentioned a second ago. As I write, NZF’s portfolio of 671 bonds carries an average leverage-adjusted duration of 14 years. That’s the key to further upside as rates move down.

By the way, that leverage I just touched on amounts to about 35% of the portfolio. That sounds high, but it’s actually a normal ratio for a fund holding government-backed bonds like these. And it’s another benefit as rates decline, since lower rates will cut NZF’s borrowing costs.

But I’ve really left the best for last here: the dividend, and how much it could really mean for you, depending on your tax bracket.

An 11.2% Payout “Disguised” as 7.6%

As you might’ve guessed, NZF’s dividend has provided most of our 30% gain on the fund, since its price has only risen around 6% since we bought. That’s in part because management has hiked the dividend a healthy 85% in the last three years.

Given that the fund’s price tends to move slowly, these hikes went a long way toward boosting NZF’s 4.3% current yield at the time of our buy to 7.6% today.

And that’s before we talk tax benefits, which boost our payout even more—potentially a lot more. In the top tax bracket? NZF’s 7.6% yield flips to a gaudy 11.2% for you, with your federal tax savings, according to Bankrate’s taxable-equivalent yield calculator:

Source: Bankrate.com

In addition, we’ve got a shot at further dividend growth here as rates fall, driven by NZF’s NAV gains and its lower borrowing costs.

At the end of the day, our approach here is pretty simple: Come for the upside as AI swings NZF’s NAV/rate “teeter-totter” back our way. Stay for the 7.6% dividend (shielded from Uncle Sam), which we’ll happily pick up while we wait.

Urgent Note From the Publisher

Kevin Wallen here. I’m the publisher of Contrarian Income Report.

Brett’s take on AI and municipal bonds clearly shows that there are few corners of the economy this tech will leave untouched.

Municipal bonds are one place we can still pick up bargain dividends before AI integrates itself into the economy. And our CEF specialist, Michael Foster, has been hard at work uncovering more.

He’s come up with 4 other AI-driven breakthroughs that aren’t getting nearly the attention they deserve. And he’s uncovered 4 other CEFs—yielding 10% on average—dialed straight into each of these 4 megatrends, which he calls “pivot points.”

This is, hands-down, one of the biggest opportunities for upside (and 10% dividends!) I’ve seen in my 11 years as publisher at Contrarian Outlook. I’m urging all income investors to take a close look at it today.