All-time highs are usually the wrong place to shop for stocks. Prices climb, yields drop, and the only deals left are in junk that nobody wants for good reason.

Right now, though, we have seven cheap, high-yielding dividend stocks available in an otherwise rich market. And these blue-light specials pay. I’m talking about seven dividends yielding 5.2% to 10.3% as I write.

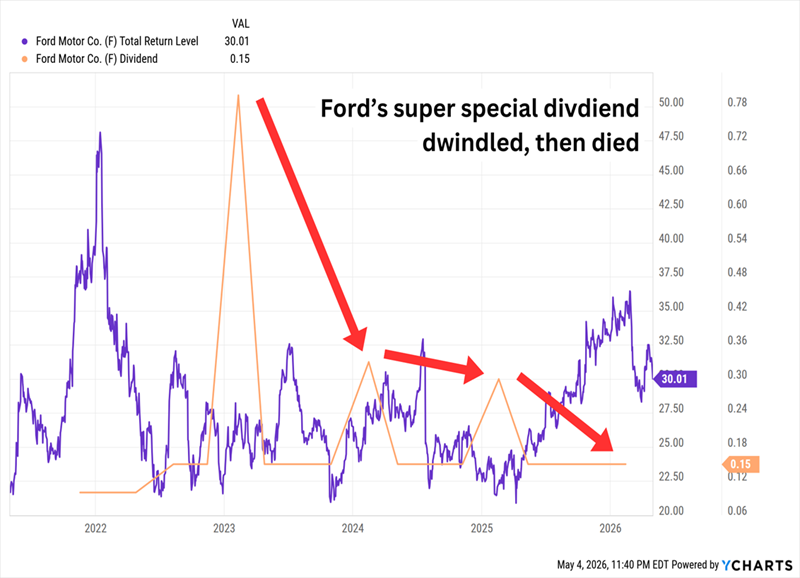

Let’s start with automaker Ford (F, 5.2% yield), an American automotive pioneer and its F-Series has been the country’s best-selling truck for more than four decades. It’s also a perpetually cheap stock, almost always trading at a fraction of the consumer discretionary sector’s average P/E.

Ford has delivered five straight years of top-line growth, but the bottom line is more interesting right now. Wall Street thinks the automaker will deliver a 45% year-over-year jump in earnings this year, and shares trade at just more than 7 times those estimates. F shares also boast a bargain-basement 5x forward cash-flow multiple.

Part of that bottom-line boost, however, is coming from a $1.3 billion government refund for previously collected IEEPA tariffs, which have since been struck down. The company’s “core” guidance is looking a little light thanks in part to higher commodity costs.

Ford has lost a little of its income shine; a short run of annual special dividends ended this year.

Goodbye to Those Extra Points of Yield

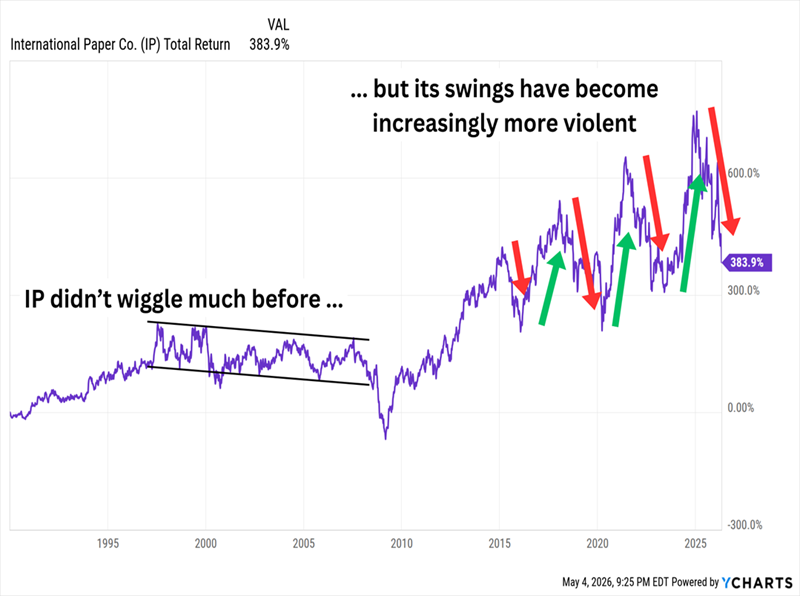

International Paper (IP, 5.9% dividend yield) produces and sells linerboard, whitetop, and saturating kraft paper, among other packaging products. It’s also a major player in pulp, which is used in a variety of personal-care products, construction materials, paints and more.

This area of the market has enjoyed a decades-long boost from growth in e-commerce, but the economic ebbs and flows of the past few years have made IP an increasingly volatile stock to own.

On the Upside? Dip-Buying Opportunities Come Around More Frequently

IP has been cheap for a while. The discount continues thanks to a year-plus slide amid higher input costs, softer demand and tariffs—shares are down roughly 45% (even with its sizable dividend included) since early 2025.

The upside? For one, that has driven the company’s yield to nearly 6% as of this writing. It now trades at less than 8 times cash-flow projections, as well as 12 times 2027 earnings estimates, which are expected to jump by more than 90% amid a restructuring and the 2025 acquisition of DS Smith.

But new money is effectively buying two companies. Earlier this year, IP announced it would split into a pair of public companies—the existing firm will represent North American assets, while the new entity will contain all of its Europe, Middle East & Africa (EMEA) assets.

While a few “traditional” stocks are on sale, many more deals can be found in the real estate investment trust (REIT) sector.

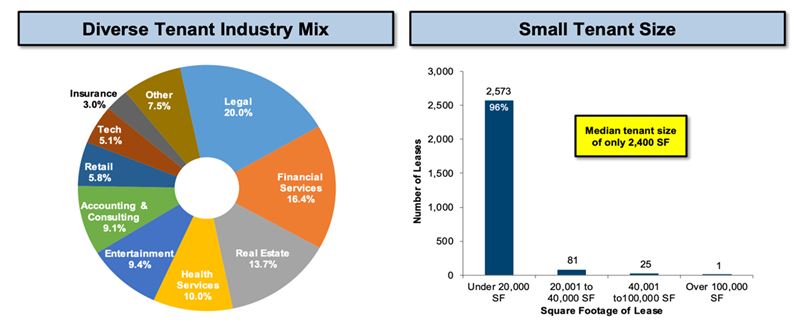

Let’s start with Douglas Emmett (DEI, 6.3% dividend yield), a niche office-and-apartment operator that trades at just around 12 times estimates for future adjusted funds from operations (AFFO, an important REIT profitability metric).

Douglas Emmett operates exclusively in Los Angeles and Honolulu. Offices are the lion’s share of the business at nearly 80% of annual rent. DEI is the largest office landlord in both cities, with around 2,700 leases at a median size of about 2,400 square feet. Virtually all of its leases include annual rent escalators of 3% to 5%, and its annual lease expirations are spread pretty evenly, at about 11% to 15% annually. It also has a pretty diverse tenant base:

Source: Douglas Emmett Investor Overview

Its multifamily portfolio, which accounts for the remaining ~20% of annual rent, includes 15 properties with 4,410 units in service and another 1,035 units in development.

Like with many office REITs, Douglas Emmett was forced to cut its dividend in the wake of COVID—DEI hacked off 32% of its distribution in late 2022. The remaining dividend is much more sustainable at about 75% of AFFO estimates.

It’s a major player in an attractive market (L.A.), but the return-to-office snap-back hasn’t been as sharp as DEI might have wanted. That has left the REIT with little in the way of pricing leverage, which helps explain a lethargic valuation.

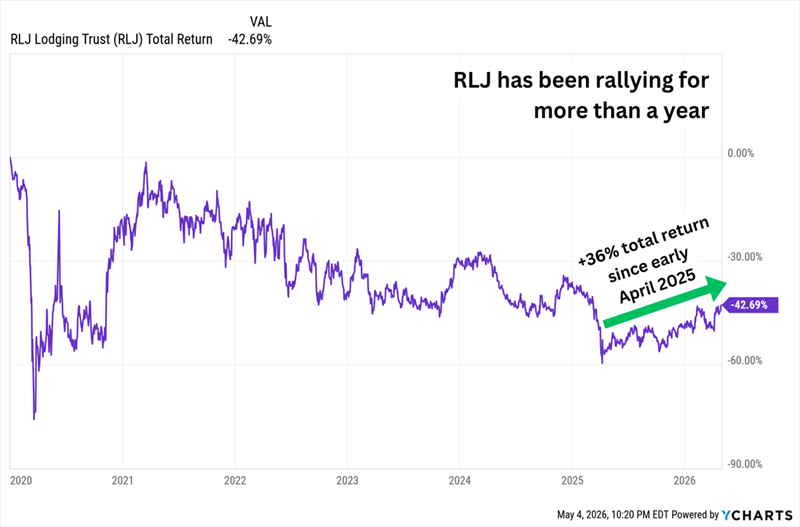

RLJ Lodging Trust (RLJ, 7.2% dividend yield) is a hotel REIT whose properties host “premium-branded, rooms-oriented, high-margin, focused-service and compact full-service hotels located within the heart of demand locations.”

That’s hotel-ese for “larger hotels that offer specific, limited amenities and essentials, and smaller hotels that offer a wide variety of services like bars, restaurants and spas.” Its brands run the gamut, including Embassy Suites, Courtyard by Marriott, Hyatt Place, Wyndham, Residence Inn by Marriott, Hilton, and more.

RLJ started its current decline more than a year before COVID, but shares have lost more than 40% (with dividends included) since the start of 2020.

But RLJ Is in the Midst of Its Most Prolonged Recovery Since Then

The REIT potentially could get a lift from sporting events like the 2026 World Cup and 2028 Summer Olympics, as well as America’s semiquincentennial celebrations. But it could face headwinds in D.C. thanks to lower government demand, as well as in Austin, where the convention center is temporarily closed for renovations.

In July 2025, I highlighted RLJ among several companies that were positioned to raise their dividends soon, and it simply didn’t. The dividend has now remained stagnant since mid-2024, stalling at less than half of its pre-COVID level. It’s not for lack of room—RLJ’s AFFO payout ratio is only 45%, which normally indicates a lot more room to expand the dividend.

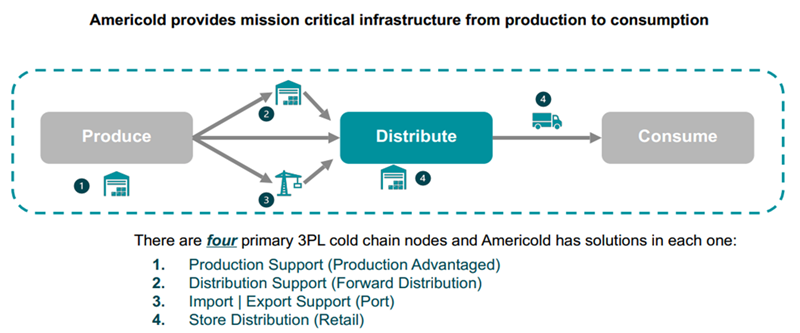

Americold Realty Trust (COLD, 6.4% dividend yield) is one of the most specialized REITs around. It has a portfolio of 224 temperature-controlled warehouses, making it essential across the food chain, from producers like Unilever (UL) and General Mills (GIS) to retailers like Walmart (WMT) and Grocery Outlet Holding (GO).

Source: Americold Investor Presentation Winter 2025

However, a huge buildout in cold-storage assets turned into a major oversupply problem, and the macro environment has weighed on demand. Lower beef supply has further cut into any need for Americold’s offerings. That has resulted in a roughly 70% plunge in COLD shares over the past five years.

That said, the company just rallied hard following its first-quarter earnings report. The results themselves weren’t much to get excited over–most notably, AFFO guidance stayed pat. But Americold also reported it was joining a cold storage joint venture with Swedish private equity company EQT’s Active Core Infrastructure Fund. COLD will contribute 12 cold-storage facilities with a value of more than $1.3 billion and retain a 30% equity interest. It expects to receive $1.1 billion in net cash proceeds, which it says it expects to use to repay debt.

The news drove a double-digit spike in shares, but even then, the stock still trades at less than 12 times AFFO.

COLD shares could be staring at another catalyst, too. Investment firm Sieve Capital has launched a public campaign against the re-election of Chairman Mark Patterson and Director Andy Power at the company’s May 18 annual meeting, and to prompt a review of all strategic alternatives, including a full sale of the company.

Highwoods Properties (HIW, 8.2% dividend yield) is “in the work-placemaking business … creating environments that spark experiences where the best and brightest can achieve together what they cannot apart.”

Or as the rest of us here on Planet Earth might say, it’s an office REIT.

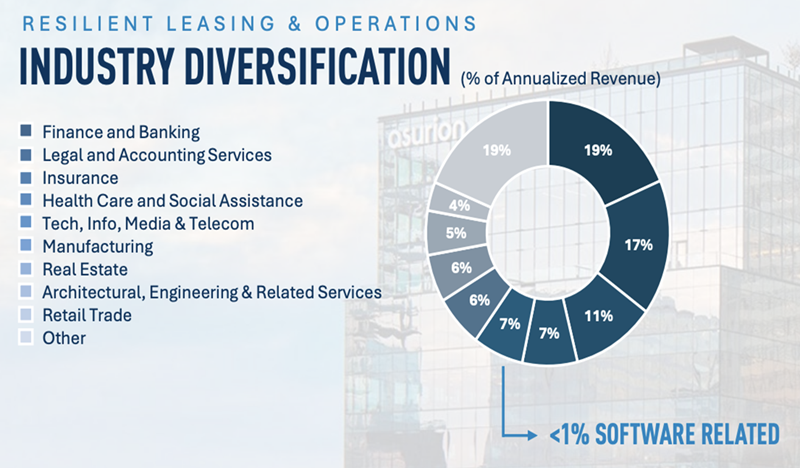

Highwoods owns or has an interest in 27.4 million rentable square feet of developed properties in the “best business districts” of primarily Sun Belt cities including Atlanta, Charlotte, Dallas, Nashville, Orlando, Raleigh and Tampa. These cities generally feature higher-than-national-average population growth, rent growth and office employment growth.

Better still, its office portfolio is fairly diversified, with only fractional exposure to the disrupted software industry.

Source: Highwoods Q4 Investor Presentation

Unfortunately, this appealing-on-paper business has delivered appalling returns; shareholders are sitting on a 25% total loss since the start of 2020. But rents are heading higher, and the company just provided year-end occupancy guidance of 86.5% to 88.5%, which would amount to roughly 1 to 3 percentage points’ worth of improvement over last year.

At current prices, HIW trades at just 7 times FFO estimates. Meanwhile, it has only offered a yield north of 8% a handful of times in its history—briefly in 2023 and the Great Recession, as well as for a prolonged period during the dot-com bubble burst and recovery.

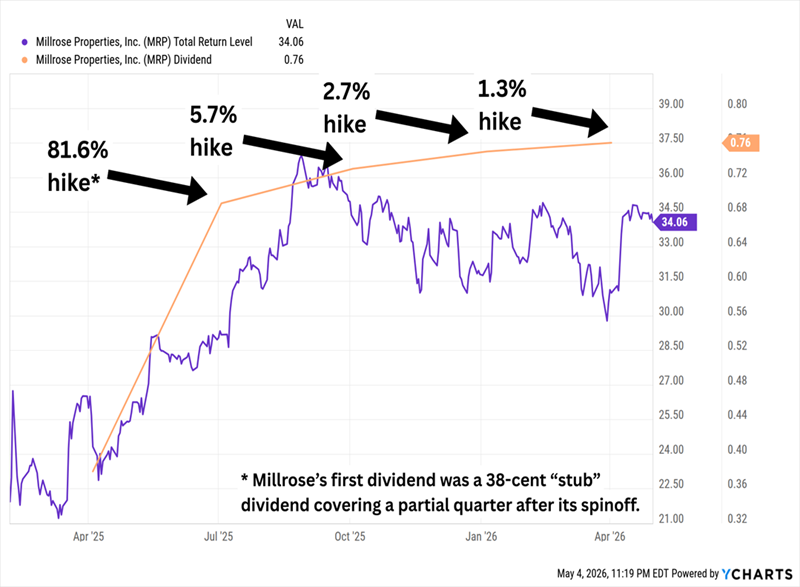

Millrose Properties (MRP, 10.5% dividend yield) is an oddball REIT that has fared well since Lennar (LEN) spun it off in 2025, smoking the sector by 45 percentage points and delivering dividend increases in every quarter since hitting the market.

Millrose’s Hikes Are Slowing, But Still Going

The company exists to buy and develop residential land, then sell finished homesites back to Lennar and other homebuilders through option contracts with predetermined costs.

I mentioned in March that Millrose has delivered higher AFFO across every quarter of 2025, and the analyst community thinks MRP will maintain or modestly grow AFFO every quarter across the next couple years.

Despite all of this, the market is still trying to figure out what Millrose is worth, and at around 9 times AFFO, Wall Street still might be shortchanging the REIT. The question becomes where the company will find additional growth. The answer is likely debt—the company won’t issue equity below book value, and it still has about $1 billion of debt capacity before it gets to its stated maximum debt-to-capital target of 33%.

My Favorite 11% Dividend Is a Cure for 2026’s Chaos

Millrose is churning out better results than most of the other value-priced REITs on this list, but it’s a young issue in a market with no comparisons—it’s extremely difficult to handicap.

If I’m going to take a swing on a double-digit yield, I’d prefer to wave my bat at a ticker with a more established track record.

Right now, one of my favorite home-run dividends is a heavily diversified, brilliantly built bond portfolio that yields 11% but is also set up for stock-like gains.

This fund checks off just about every income box I can think of:

- It pays a whopping 11% in annual income!

- It has increased its dividend over time

- It has paid out multiple special dividends

- And it pays its dividends each and every month!

On top of that, Morningstar previously named this fund’s manager a Fixed Income Manager of the Year. He’s been inducted into the Fixed Income Analysts Society Hall of Fame, too.

That’s about as good a resume as we’ll find, and his fund will pay us $1,100 for every $10K we invest.

But you’ll need to act soon. Premiums on funds like these tend to rise as volatility ticks higher and as investors rotate out of growth stocks and into reliable sources of income like this. I don’t want you to miss your chance. Click here and I’ll introduce you to this incredible 11% payer and give you a free Special Report revealing its name and ticker.