The stock market is roaring, and according to the media, it’s all because of AI.

But is that really true?

Because if it is, there must be other corners of the market, beyond tech, that are being overlooked. And that’s where we contrarians want to go hunting for high, steady (and cheap!) dividends.

Let’s break this question down, starting from a 50,000-foot view, then zeroing in on an ignored 8.1%-yielding fund with strong upside as investors come to realize its true value.

Source: State Street Investment Management

This table is a great starting point—a kind of roadmap to where the cheapest stocks in the S&P 500 might be hiding out.

It’s simply a table of ETFs for every S&P 500 sector, and it shows us that, yes, tech is a big factor behind this year’s 10% gain (as of this writing) in the overall index.

Since the start of the year, tech has gained an eye-watering 29.4% as of this writing, pretty well all on AI strength.

But that’s not the only reason for the market’s gain. Energy, for example, edges it out, up 28.6% on the oil shortfall caused by the Iran conflict. Materials, industrials and even real estate have also beaten the market’s return. (We talked about the opportunity taking shape in real estate investment trusts in last Thursday’s article.)

What I really want to draw your attention to in the chart above is the flat performance of consumer-discretionary stocks.

On its face, you can understand why this is the case: Inflation is high. Hiring is sluggish. Wage growth is waning (to the point it slipped behind the CPI in April). Consumer sentiment? In the tank.

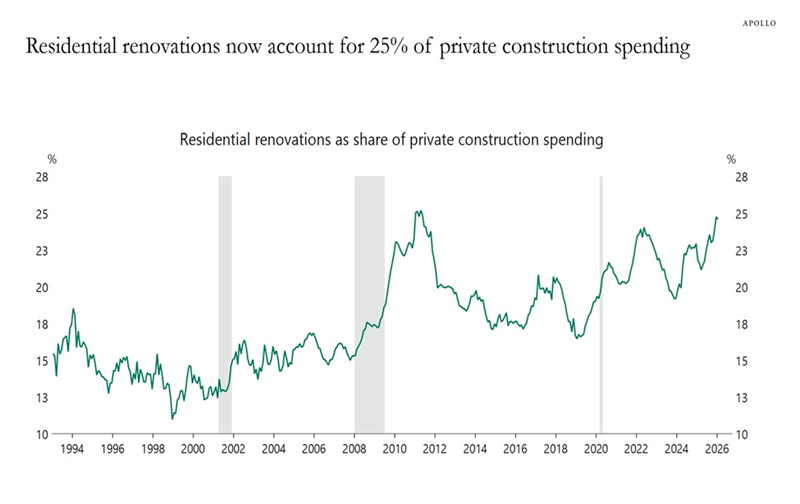

And yet, there’s plenty of evidence that consumers, while grumpy, are still spending. Consider home renos, which, according to the chart below from Apollo Global Management, have surged to account for a quarter of all private-construction spending.

Source: Apollo Global Management

Today’s level even tops the pandemic reno boom, when we were all building home offices and redecorating, thinking we may never go outside again!

It also clearly shows the strength of the American consumer. Compare it to the surge in 2010, for example. Back then, interest rates on home-refinance loans were low. Today, they’re high. Inflation was 2% then. It’s 3% now—after only gradually moving down from its sickening 9% peak in 2022.

But none of that has put off consumers from spending on one of the biggest-ticket items there is for most people. This, in other words, is a textbook contrarian opportunity: a powerful force (consumer spending, in this case) mainstream investors are downplaying.

Here’s how we’re going to go after it.

Forget ETFs—This 8.1%-Paying CEF Is the Best Play on Resilient Consumers

The first place most people would look in a case like this is an ETF like the State Street Consumer Discretionary Select Sector SPDR ETF (XLY). But we’re dividend investors, and XLY’s sad 0.75% yield just won’t cut it for us.

Instead, we’re looking to this 8.1%-yielding closed-end fund (CEF) called the Eaton Vance Tax-Managed Buy-Write Opportunities Fund (ETV). As we’ll see, it’s nicely positioned to profit from the strong US consumer, including one holding that’s tied directly into the home-reno boom.

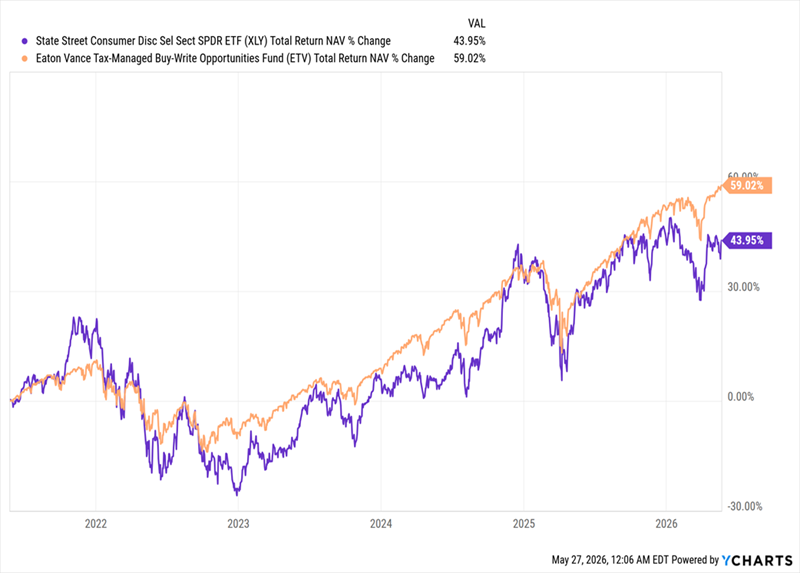

Let’s start with the fund’s performance:

ETV Crushes Consumer Stocks

As you can see in purple above, ETV has beaten XLY—the consumer-discretionary ETF, in orange—on a total NAV return basis over the last five years.

(By “total NAV return” I mean the performance of the fund’s portfolio, including dividends collected, as opposed to its market price. The difference between the two creates the big discount ETV currently sports, which we’ll talk about shortly.)

And while the fund’s 150 holdings are weighted toward tech, at 39% of the portfolio, that’s a bit deceiving because its top tech holdings are mainly consumer-focused, including Apple (AAPL), Amazon.com (AMZN) and Tesla (TSLA).

And there are plenty of other consumer favorites further down ETV’s holdings list, including Chipotle Mexican Grill (CMG), Best Buy (BBY), Carvana (CVNA), Hershey (HSY), Nike (NKE), Darden Restaurants (DRI), Yum! Brands (YUM), Marriott International (MAR) and Home Depot (HD).

All of these companies are benefiting from Americans’ continued strong spending, with Home Depot directly profiting from surging home renos. That, in turn, is supporting ETV’s 8.1% dividend, which rolls out monthly.

That income also comes from the fund’s covered-call strategy, which provides some downside protection while bringing in cash, since it collects fees on all the options it sells, regardless of how the underlying trades turn out.

One would think a dividend as high as this one, backed by an undervalued basket of blue chips and a proven covered-call strategy, would be high on investors’ buy lists.

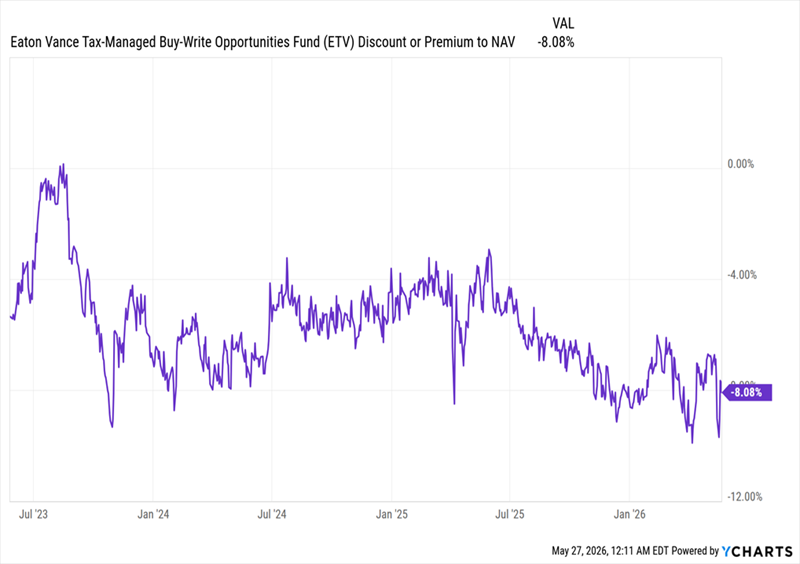

Instead, ETV’s 8% discount to NAV is at one of the widest levels I’ve seen in years. That markdown has also bottomed out recently, suggesting investors are finally starting to take notice of this smartly run CEF.

ETV’s Discount Hits Bottom—Then Bounces

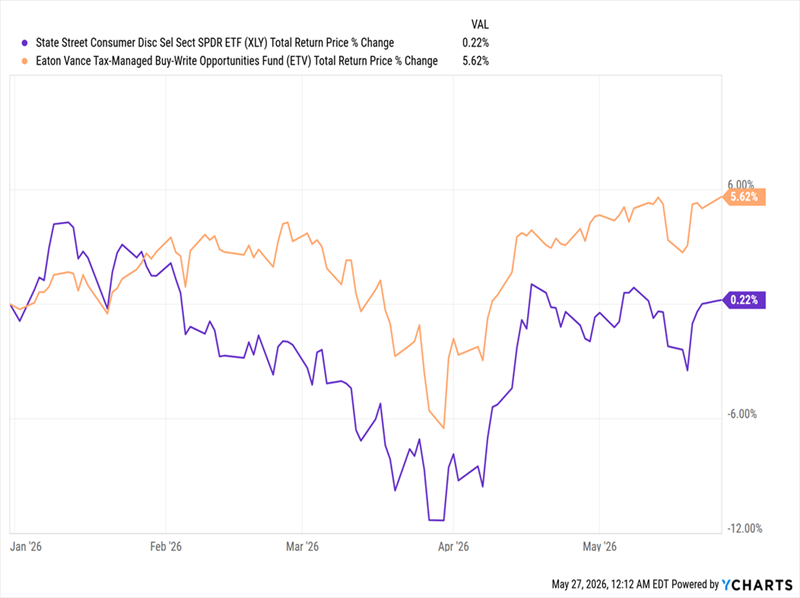

With this momentum, ETV will likely get more bids, boosting its market price and shrinking the discount further. In fact, that’s already starting to happen, as ETV’s total return (based on market price this time) has outrun XLY this year.

ETV’s Narrowing Discount Pushes It Past the Benchmark

Before we wrap, let’s shift back to the dividend: To most investors, ETV’s 8.1% payout seems high, but it’s actually lower than the 8.8% average for all CEFs tracked by my CEF Insider service. So there’s nothing particularly unusual here.

ETV had a stable dividend for years until the 2022 crash, which forced management to reduce it. But another cut is unlikely given the economy’s strength. But even if that were to happen, it would likely only reduce ETV’s 8% yield to something like 7.2%. That’s still a monster payout.

With its high income and still-wide discount, ETV is clearly a better way to profit from America’s underappreciated consumer spending than XLY. And it’s just one of many CEFs that crushes index funds—whether you measure by dividend yield, past performance or both.

No, You Haven’t Missed the AI Boom. Here’s How to Get In (With 8.7% Dividends)

Just because we’re looking beyond the AI boom doesn’t mean we’re ignoring it. Far from it!

Truth is, there are still CEFs that hold top AI stocks—and let us buy them at BIG discounts.

That’s the beauty of CEFs. Not only do they give us big dividends, but because of their wide discounts to NAV, they let us buy those same holdings at a bargain.

In the case of the major AI players, that means we’re essentially buying well below their current market prices. And we get a big dividend as a nice “bonus.”

To get you in as easily as possible, I’ve handpicked my top 4 AI-focused CEFs to buy now. These funds yield 8.7% on average and hold all the familiar names associated with AI—the Microsofts, NVIDIAs and Metas of the world.

Plus—and this is key—they also hold the companies best positioned to profit from AI. Here I’m talking about the banks, insurers, manufacturers and, yes, consumer stocks that are only just beginning to reap the productivity gains AI is unleashing across the economy.

This 4-fund “mini-portfolio” is a complete AI investing package, and it comes your way at a deep discount and a rich 8.7% dividend!

The time to buy is now, before these funds’ discounts slam shut and their prices race away from us. Click here and I’ll lay out the details on all 4 of them and give you a Special Report revealing their names and tickers.