I was happily sipping my morning coffee on the couch. Quietly…’til now.

Here marched my eight-year-old, straight at me with a bone to pick.

“Dad, MarkRober said the cars can’t really drive themselves. They drive into walls! So if you get a car that drives itself, it’s going to drive you right into a wall.”

She paused and glared at me while she reached for her conclusion.

“Is that what you want, Dad?”

MarkRober’s real name is Mark Rober. He’s a YouTube guy who preaches science to kids. (Note: Preach isn’t quite teach.) My daughter pronounces his name as one when she recites his gospel.

My wife and I like the science aspect. We don’t love the personality but we roll with it. Usually.

At this moment, however, I had been completely steamrolled by a MarkRober video that I had never seen.

“Oh, really?” I said, amused but slightly defensive. “What’s his take on self-driving?”

“They don’t work!” she yelled. And continued. “He took a Tesla and it drove right into a wall because the cameras couldn’t see it in the rain. Do you want to get a new car that drives you into walls?”

I had been making noise about buying an EV specifically for the self-driving capabilities. A sequel to Driving Miss Daisy—a robot car tasked with Driving Your Dividend Guy!

My daughter didn’t know that I had lunch with a friend earlier that week. After we dined, we took his brand-new Tesla Model Y for a spin. The car drove us to four places and after that ride, I was sold. I ordered mine days later.

The receipt was already in my inbox. She was going to have to learn to love this thing, MarkRober wall or not.

Had I made a mistake, though? Perhaps. But this was not the time to admit it!

“Don’t worry. Daddy’s going to take the wheel in a storm.” Then I paused for effect. “I grew up in Buffalo, you know.” Yes, she nodded. She’d heard it one thousand times.

But your editor raced to do some research—I’m not buying a car that drives straight into a wall!—and learned the “wall” was Styrofoam, painted to look like the road. Wile E. Coyote style. So unless there are walls painted to look like roads out there, I’m pretty sure I’ll be fine with Full Self-Driving (FSD).

Plus! MarkRober’s test ran on Autopilot, not Full Self-Driving. When someone re-ran it on FSD, the car did better. But of course, my steady hand is always there to take the wheel as needed.

The bigger trend here is the demand for EV batteries. There are more and more on the road and they require one key ingredient for every EV that gets ordered, Tesla or no!

That need for lithium benefits top producer Albemarle (ALB). ALB extracts and processes the lightweight metal that goes inside every EV battery, smartphone, laptop and power tool on the planet. If it’s rechargeable, Albemarle’s lithium is likely inside it.

Its customers are the battery makers who supply Tesla, GM, Ford and BMW—basically every automaker going electric. All told, ALB controls roughly 15% to 17% of global lithium supply, so it’s the dominant producer in a fragmented market.

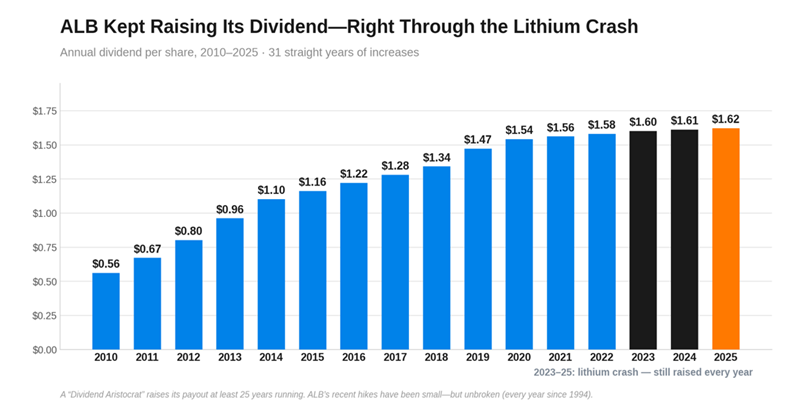

Here’s the setup. Lithium prices crashed over 80% from their late-2022 highs to early-2024 lows. Vanilla investors panicked and fled, and the “lithium is dead” headlines ran for months. It was the kind of capitulation we contrarians live for. Meanwhile, Albemarle kept raising its dividend right through the crash. And now that lithium prices are recovering, ALB is ready to run.

I ran the numbers on every lithium recovery cycle over the past decade and the results tell us one thing: buy ALB! Since 2016 we’ve seen three lithium recovery cycles. All three times ALB has soared, rewarding investors with a double (+97% on average) in just 12 months. (The fourth recovery, by the way, is unfolding now…)

Previous Lithium Recoveries (and ALB Action)

So this fourth bounce still has room to run. And it could go longer than the previous three because the demand for lithium is evolving into a megatrend. Global EV sales have risen 10-fold in the last seven years (from 2 million in 2018 to 20 million last year) and they’re projected to double from there by 2030.

Each EV battery needs 8 kilograms of lithium. Then there’s the grid, which has to store energy—it needs 30% more of the commodity, too. The Wall Street suits are catching on. Goldman Sachs sees lithium prices rising through 2028 as demand outpaces supply, and JPMorgan recently upgraded its own outlook.

Plus, in March, Albemarle sold its non-core chemicals Ketjen business and used the $670 million to pay down debt. Its balance sheet is as clean as it’s been in years. But the financial pundits are fixated on the company’s recently quarterly loss, missing the fact that it was a one-time Ketjen write-down and a tax adjustment

In reality, the business threw off $692 million in free cash in 2025 (a down cycle year). ALB stayed cash flow positive, even with its main product down 80% in price! And it kept hiking its payout through the down cycle, making thirty-one straight years of hikes. Yet payout ratio sits at a comfortable 46% of free cash flow and, remember, these are depressed earnings (closer to the cycle low than high!)

ALB’s Consistent Divvie Growth

Be prepared: Albemarle’s stock can fly all over the place. But here’s the thing: when lithium rallies, Albemarle soars. The EV cycle is turning for the better and this “pick and shovel” supplier has plenty of room to run.

And ALB isn’t the only dividend grower I like here! I have my eye on five more overlooked payers that are set to climb 15% per year from here, no matter what the broader market does. Please click here for the company names, stock tickers, and buy-up-to prices.