One of our favorite tech-focused closed-end funds (CEFs) is showing a pattern we love to see. What I’m going to show you below is one of my favorite setups for future gains for us, while we collect strong dividends, too.

The fund in question—the BlackRock Technology and Private Equity Term Trust (BTX)—yields 7.4% as I write this, so we’re getting paid handsomely while we wait for those gains to materialize.

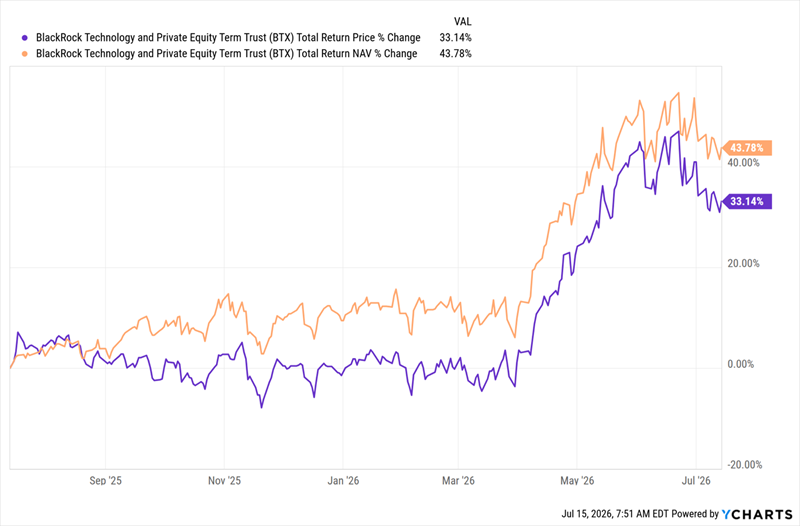

Plus, the performance of this CEF’s underlying portfolio, or its “total NAV return” in CEF-speak, has earned enough over the past 12 months—43.8%, to be exact—to pay that dividend many times over, so the payout looks safe (and is paid monthly, to boot).

This 7.4%-Paying Tech Fund Is Soaring, Inside and Out

There’s something else about this chart that I want to draw your attention to: the purple line, or the fund’s total return based on market price (which is more influenced by investor sentiment). It trails the fund’s NAV, and the gap has been widening.

This is possible with CEFs like BTX because their closed-share structure lets the market over- or underprice a fund relative to how its portfolio is doing.

That’s the start of our opportunity with BTX. To get at it in full, we first need to talk about why investors are suddenly nervous about one corner of tech in particular: semiconductors.

Fact is, we’re now in the midst of the third major drawdown in “semis” this year, and it’s left the benchmark for this sector, the VanEck Semiconductor ETF (SMH), a full 9% off its year-to-date high, as of this writing. That may not sound bad, but it comes at a time when the S&P 500, benchmarked by State Street SPDR S&P 500 ETF (SPY), is basically at its all-time high.

Before we drill into what ails semis, and the growth (and dividend) opportunity it’s setting up for us in BTX, let’s do something most media outlets rarely do when discussing these products: talk about what they do, and following from that, why investors are so downcast on them all of a sudden.

The place to start, as is the case with so many things these days, is AI.

Semiconductors, in a nutshell, are the chips that power modern electronics. As a result of the data-center buildout, the stocks that make up SMH—like NVIDIA (NVDA), Micron Technology (MU), ASML Holding (ASML), Texas Instruments (TXN), Intel (INTC), Advanced Micro Devices (AMD), Broadcom (AVGO) and Applied Materials (AMAT)—have soared.

However, such a fast rise in names like these in such a short time makes some investors nervous. That’s natural, especially when you consider that many of these stocks are far from flashy growth names. Texas Instruments, for example, has been around for generations, yet its stock has returned 78.2% in 2026 alone.

Beyond the nerves, however, there is simple profit-taking. SMH, after all, has more than doubled in the past year.

In other words, the recent decline in semis makes sense. But a prudent investor should ask: Is this selloff justified, or is it again time to buy in?

Semiconductor Demand Is Still Soaring

If we look at the facts, it seems quite clear that demand has not waned. Not even a little.

The world’s largest chipmaker (by a huge margin) is Taiwan Semiconductor Manufacturing, or TSMC. The company just reported a 67.9% year-over-year sales increase for June, announcing the news before their scheduled earnings release.

SemiAnalysis analyst Sravan Kundojjala also told CNBC that this shows strength for the entire market: “The demand-supply situation in AI is still quite tight, and TSMC is sold out on N3, which is targeted by all leading AI GPU and CPUs this year,” he said.

So the sales are still there, and demand is still red-hot. But what about these companies’ valuations?

On the one hand, stocks like Broadcom (trading at 67-times its last 12 months of earnings), ASML Holding (59.9) and Texas Instruments (53.3) are on the pricey side, while NVIDIA (32.3) and Micron (22.2) are still relatively cheap compared to the broader market. In fact, both of these AI darlings are in fact cheaper than the S&P 500, which currently has a 32.6 P/E ratio.

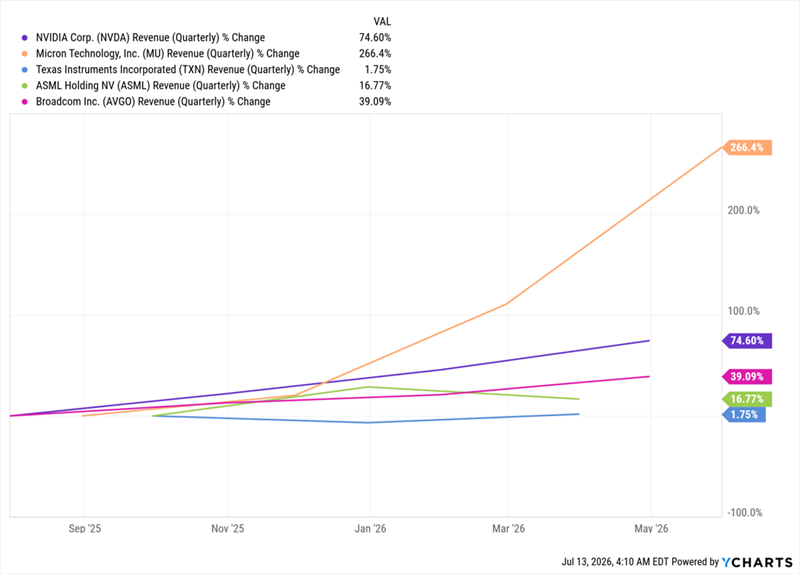

So some semiconductor stocks are bargains, based on their P/E ratios, while others aren’t. That’s not terribly odd on its own. But this is: The semi firms growing their sales the fastest are the cheapest. Check out the revenue growth from Micron (in orange) and NVIDIA (in purple) below.

NVIDIA, Micron Post Skyrocketing Sales

With sales far ahead of the higher-priced companies, NVIDIA and Micron are clearly high-value stocks. But why is the market pricing them so cheaply?

That’s a whole other article, but suffice it to say, both of these stocks are very much AI darlings and in the media spotlight, so they tend to gain (and fall) aggressively when the mood around AI shifts. And over the last few weeks, investors have soured on the AI narrative somewhat, despite the strong data around the AI buildout. That’s where our BTX opportunity comes in.

BTX Gives Us “Discount-Driven” Tech Growth (and Plenty of Dividend Cash)

In a market like this, we especially want to avoid ETFs like SMH, which, because of the indices they track, must hold both pricey and cheaper semiconductor stocks. A more actively managed tech fund, like BTX, avoids this problem, and it pays us that 7.4% dividend, too—compared to a sad 0.2% for SMH.

The fund also holds both of our undervalued semiconductor names—Micron and NVIDIA—as well as a mix of other high-flying tech companies, like privately held quantum-computing firm PsiQuantum; Lumentum Holdings (LITE), a maker of optical-networking gear used by AI systems; and even Space Exploration Technologies (SPCX). This gives us diversification beyond the partly overplayed semiconductor sector while still getting us into the cheaper chipmaker stocks.

And the best part is, BTX itself is a bargain right now.

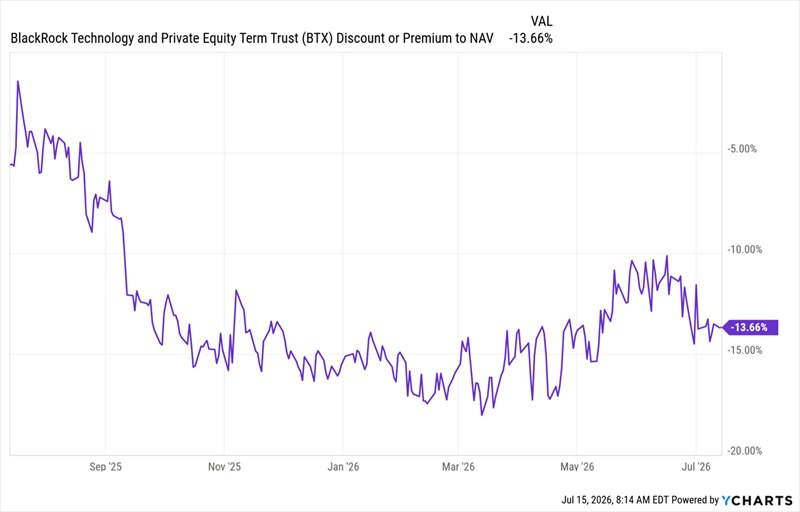

A Slowly Disappearing Discount

With the fund’s market price trailing its NAV, its discount to NAV (a key CEF value metric) has widened to attractive levels. Earlier this year, BTX saw its discount widen to close to 20%, but as tech has recovered, its discount has faded—until the recent volatility in tech caused that discount to widen a bit again.

That’s left us with that tidy setup I mentioned earlier: a still-wide discount that’s narrowing. Then there are the dividends.

With that 7.4% dividend yield, BTX is a generous payer, and since the fund’s NAV is up so much in the past year, it has the profits to keep paying that dividend without eating into said NAV to fund them. So we can collect a reliable income stream while we wait for the fund’s discount to close and the wider semiconductor market to recover.

That leaves us with a fund paying a well-covered 7.4% dividend, trading at a 13.7% discount that’s narrowing, and with convincing data that the semiconductor selloff is overblown. That’s a great setup for us to buy more of smartly run BTX.

Get Your “Bargain” Semiconductor Shares (and a 7.4% Payout) With BTX. Then Do This.

Buying bargain-priced semiconductor (and other tech) stocks through BTX is a great first step to strong AI profits. But we’re going deeper—buying into industries that AI is spreading into, and is just starting to transform.

Like we did with semiconductors through BTX, we’re “front-running” AI’s next growth leg through high-yield CEFs. I’ve handpicked 4 bargain-priced funds yielding 10% on average I’m urging all investors to buy now. I call these 4 CEFs “pivot point” funds because they represent a true economic shift in these industries.

These 4 funds hold pharma, finance and industrial stocks that all stand to gain as AI boosts their growth and cuts their costs. And while we wait for that to happen, we’ll enjoy their 10% average dividends!

Get started now by clicking right here. I’ll walk you through each of these 4 “pivot point” 10% payers and give you a free Special Report revealing the name, ticker and my complete research on each one.