Stop me if you’ve heard this before, but the Strait of Hormuz is closed once again.

Crude oil jumped 9% Monday on the news, and on cue we have vanilla investors piling into everything and anything with a rig or pipeline attached. It’s an understandable reaction, but we careful contrarians can play this smarter.

Still, the energy sector is cheap after months of investor avoidance, and today we’re going to talk about seven names that pay between 4.8% and 13.9%.

These energy payers dish their dividends with or without a geopolitical crisis.

Let’s look at these seven oil names averaging 8.8% yields right now.

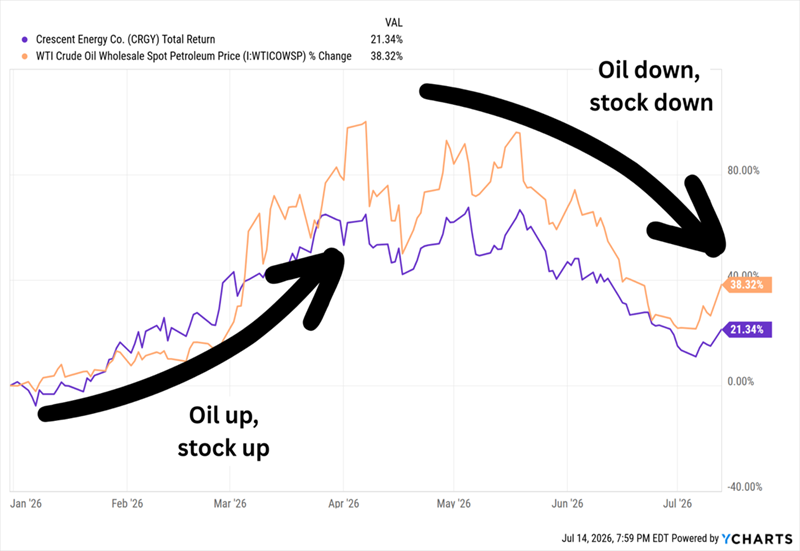

Producers like Crescent Energy (CRGY, 4.8% dividend yield) are the most direct plays on oil because barrel prices have a direct impact on their bottom line. Look at any chart of an American oil exploration-and-production firm against West Texas Intermediate crude, and it’ll usually go something like this:

It’s a Pretty Clear Connection

It’s rarely a perfect 1-for-1, of course. Many producers deal in more than one commodity. Efficiency varies from firm to firm. And they sometimes have additional lines of business past traditional E&P.

Take Crescent Energy, for instance. Crescent is a producer of oil, condensate (ultra-light oil) and natural gas. It has operations in the Eagle Ford Shale, as well as the Uinta and Permian basins, but it also owns mineral and royalty interests that are operated by other companies—thus, CRGY gets to enjoy the cash flows from those assets without having to put up capital to work them.

Growth comes not by developing new sites, but by acquiring existing operations (such as its blockbuster $3.1 billion deal to buy Vital Energy in a deal that closed late last year) and finding efficiency gains. It’s a slower-growth but more consistent model.

Declines since April have CRGY trading at just 4.4 times 2026 earnings estimates, which is just a third of where the energy sector is trading. The nearly 5% yield is decent, too, though its short payout history could be better. The company was created in the late 2021 combination of Independence Energy and Contango Oil & Gas. It quickly initiated a 12-cent quarterly dividend, raised it to 17 cents for about a year, then brought it back to 12 cents, where it has remained ever since.

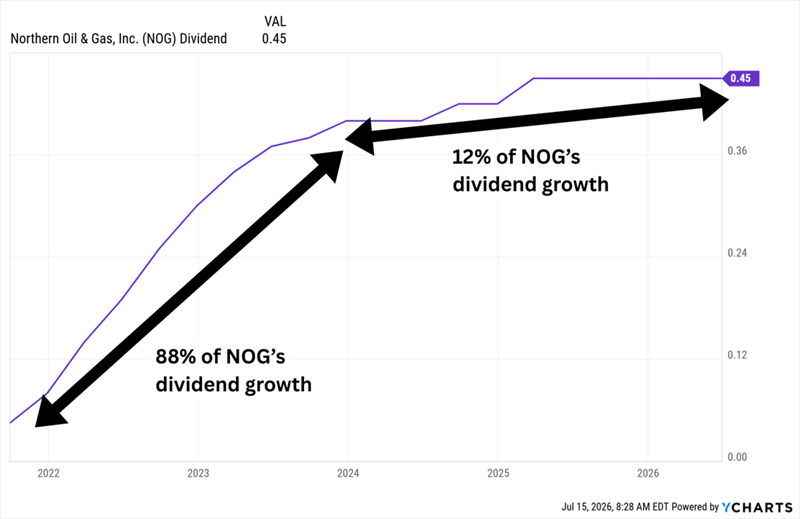

Northern Oil & Gas (NOG, 8.9% dividend yield) has been around for longer but has a similarly young dividend program. This firm was founded in 2006 and went public in 2007, and it deals in oil and natural gas across the Williston, Uinta, Permian, Appalachian and Duvernay formations.

While it’s technically an E&P firm, it’s not an operator—it holds interests in thousands of wells, then partners with other E&P operators to work them. It’s a cash-flow-friendly business, though Northern Oil & Gas didn’t share the wealth until relatively recently. The payout kicked off at 3 cents per share quarterly in 2021, then NOG ramped up that figure every three months.

For a Few Years, Anyways

It slowed to semiannually in 2024, and its last hike came at the start of 2025. Still, the 45-cent payout is light-years from where it used to be, and NOG yields a wild 9% as a result. The payout ratio, which sits at just half this year’s earnings and 45% of 2027’s, isn’t problematic, either. It’s not a cash crunch, either—the company recently cut back on capital spending, but it lifted its share buyback program by $150 million.

Shares trade at an extremely cheap forward P/E of 6, though that price also reflects a more conservative business model.

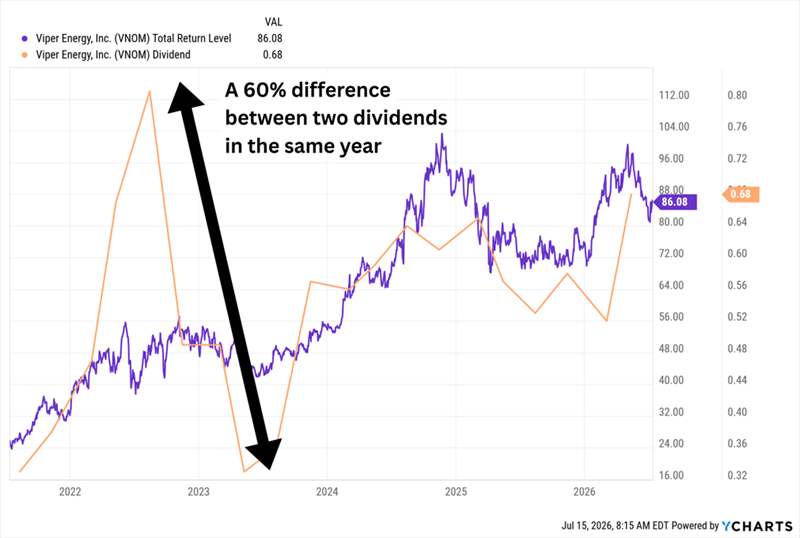

Viper Energy (VNOM, 5.4% dividend yield) is a similar company, formed by Diamondback Energy (FANG) to own and acquire mineral and royalty interests. Viper Energy leases these interests—which primarily involve oil, natural gas or natural gas liquids from the Permian Basin—to E&P companies. Again: light on capital, rich in cash.

Viper’s version of this business model has looked healthier than Northern’s of late, and investors have expressed that with their wallets: VNOM has nearly doubled on a total-return basis over the past three years and is still holding on to a decent chunk of its Q1 stock gains; NOG has lost a third of its value and is in the red year-to-date.

But Viper isn’t as much of a value, either, trading more cheaply than the market but more richly than the sector. And while the 5% yield is OK, it could change.

VNOM Has a Fairly Variable Dividend

Specifically, the company has a base-plus-variable dividend with a current floor of 38 cents, which it raised 15% this year. On the one hand, recent payouts that came to 85%-90% of cash available for distribution as dividends aren’t the norm; management indicated it would likely go back to its 75% minimum this year. But elevated prices could keep the dividend aloft, too.

Another place to look for high yields? Energy infrastructure firms—effectively “toll takers” that take a cut when oil, natural gas and other commodities flow through their pipelines, storage units and other assets.

Hess Midstream LP (HESM, 7.8% distribution yield), for instance, owns midstream energy assets such as pipelines, gas processing facilities, terminals and gathering pipelines.

Hess Midstream is a master limited partnership (MLP), which are harder to value using the traditional P/E metric. Enterprise value to earnings before interest, taxes, depreciation, amortization and exploration (EV/EBITDAX) tends to be a better lens; HESM’s roughly 7x multiple is plenty cheap compared to the 9x-10x valuations of many of its peers.

Just a couple of weeks ago, I highlighted Hess Midstream among stocks with pivotal dividend announcements coming up. I said then:

Historically, HESM has delivered a drumbeat of 1%-3% quarter-over-quarter raises that have amounted to roughly 10% year-over-year growth. But the company recently pared back its full-year capex guidance and raised its free cash flow outlook, which could result in modestly thicker raises in the quarters to come (though it muddies the potential for growth). Whatever it chooses to do, it’s likely to come in late July.

Hess Midstream’s Shares, Distributions Have Grown Hand-in-Hand

Shareholders will be looking for more than extra cash, though. They’ll also be watching for a clearer picture of what Chevron (CVX), which has a roughly 38% stake in HESM following its 2025 acquisition of Hess Corp., plans for HESM. It has been ambiguous so far. There could be upside if CVX plans to invest in the midstream name—less if it continues to simply siphon off cash.

HESM, like many MLPs, has another issue: The dreaded K-1. MLPs are required to issue us a K-1 package at the end of the tax year. These are generally headaches (for us, or for whoever does our taxes).

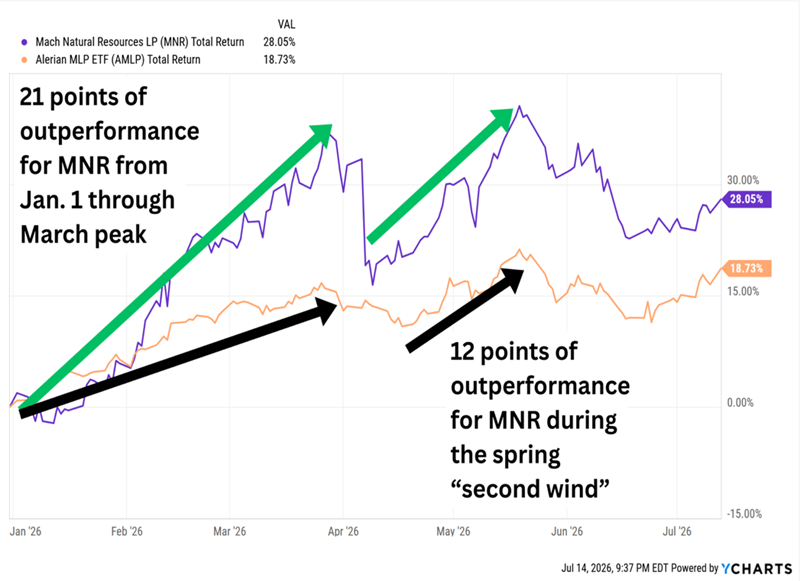

The headache might be worth it for a much bigger payout, though. Consider Mach Natural Resources LP (MNR, 13.9% distribution yield), which I highlighted right as the U.S. war with Iran was breaking out, and which generated much more upside through oil’s highs than the broader MLP industry.

MNR Has Delivered Better Swings, Held on to More of Its Returns

Mach Natural Resources is an oddball in that it’s an upstream energy MLP (read: E&P, not infrastructure). It operates in the Anadarko Basin, though it also has assets in the Green River, San Juan and Permian basins.

Mach is an efficient operator with a good track record of buying assets at low valuations. And it’s not just an oil play—in fact, natural gas represents just more than half its production.

Despite its relative strength so far in 2026, MNR still trades at a dirt-cheap 4.5 EV/EBITDAX, which isn’t much higher than where it traded in late February. The distribution is also sky-high, but it’s not fixed—it’s based on cash available after a 50% reinvestment rate and thus extremely variable.

What if we want big MLP yields but don’t want big MLP tax complexity? Closed-end funds (CEFs) let us have our cake and eat it too.

Kayne Anderson Energy Infrastructure Fund (KYN, 7.5% distribution rate) owns the top names in energy logistics. Buying this fund gets us exposure to corporations such as The Williams Companies (WMB) and Kinder Morgan (KMI), as well as MLPs like Enterprise Products Partners LP (EPD) and Energy Transfer LP (ET).

What we don’t get is a K-1. We receive a neat little Form 1099, just like a regular stock.

Unlike similar exchange-traded funds (ETFs), Kayne Anderson can use CEFs’ special sauce—debt leverage—to double down on some of its highest-conviction picks. Its fairly high effective leverage of 25% squeezes more yield out of its holdings (and it pays monthly to boot).

However, that leverage also means KYN will swing harder than a typical infrastructure ETF—for better or worse.

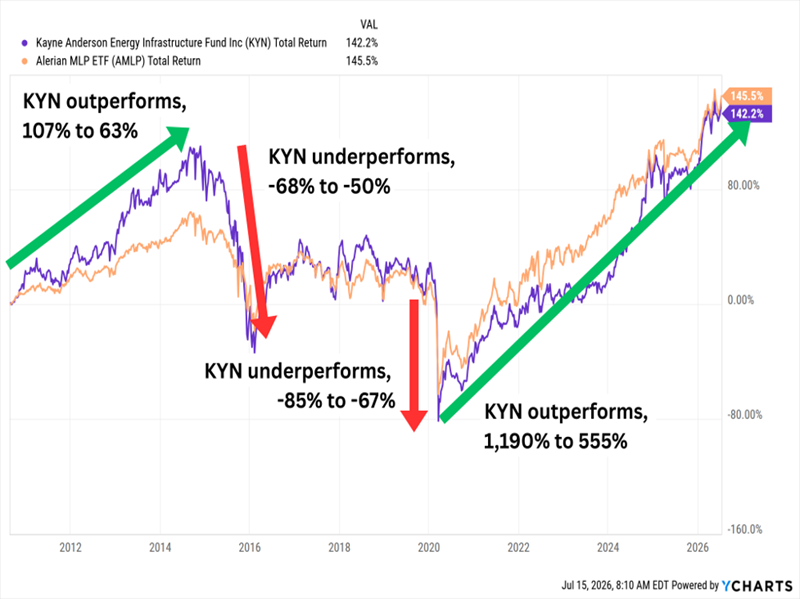

KYN Is Merely OK Over the Long Term, So When We Buy Matters

A reminder: CEFs can also trade at premiums or discounts to their net asset value (NAV), and Kayne Anderson Energy Infrastructure Fund currently trades at a 14% discount, meaning we’re buying its energy infrastructure holdings at 86 cents on the dollar. Not bad—but not as great as it sounds. That’s only a little wider than KYN’s historical 13% discount.

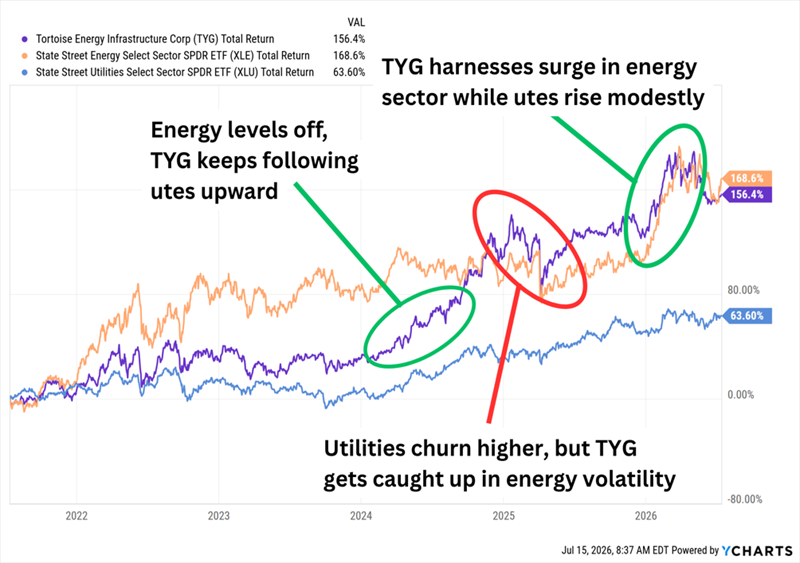

Tortoise Energy Infrastructure (TYG, 13.1% distribution rate) is a less pure play on the space, but one that comes with a massive step-up in yield. Tortoise’s CEF is a roughly 55/45 blend of energy infrastructure and utility companies. It too holds energy corporations and MLPs alike, such as Targa Resources (TRGP) and MPLX LP (MPLX), but also “utes” like Entergy (ETR) and Sempra Energy (SRE).

It’s another quirk of the CEF space. Energy ETFs are rarely structured this way; however, several energy infrastructure CEFs pair the two sectors.

We Get the Ups and Downs of Two Worlds, But the Strategy Has Merit

TYG pays monthly and we get to avoid the K-1.

Tortoise Energy Infrastructure has carried an average 14% discount over the past five years. During 2026’s energy peak, TYG traded at a small premium. It has burned off some of that fat, but at a 9% discount right now, it still hasn’t returned to bargain territory.

My Favorite Monthly Dividends Pay Up to 16.2% (And Don’t Rely on Global Chaos)

I love TYG’s yield and monthly cadence. But I don’t like betting my retirement on volatile commodities.

When you invest in my “11%+ Monthly Payer Portfolio,” you don’t need to deal with either.

This group of monthly dividends is constructed to be high on yields but low on drama. These are income checks so big, you don’t need to invest seven figures to generate the cash you need to pay your bills—and they’re written by companies that will actually let you sleep at night.

It’s a recipe for security: an income stream strong enough to let you retire on dividends alone.

Let me show you these dividend superstars, which pay up to 16.2%. Click here, and I’ll introduce you to your new 11% income stream (paid monthly) and give you a free Special Report revealing the names and tickers of every investment behind it.