Imagine a fund yielding 16.2% that’s likely to keep that high payout steady for years and years. I know it sounds unthinkable, yet we have just such a fund sitting in front of us today—ripe for buying at a discount, no less.

That would be the PIMCO Dynamic Income Fund (PDI), a bond fund throwing off that 16.2% payout, as of this writing. PDI uses a variety of credit investments to produce that outsized income stream. Thanks to high interest rates that look set to stay high for some time, and thanks to a sudden drop in the fund’s valuation, that income stream is sustainable.

With a payout like that, we’re talking about just under $5,000 a month in income on $370,000 invested! You could bring in a six-figure annual income with $620,000 invested. A little over a million in this fund returns $13,500 a month in dividend income.

Now, this isn’t the only reason to like PDI, but obviously it’s a very big reason! It’s also a reason why I’ve been following this fund for a long time. Back in 2017, I wrote that PDI “is a quality fund that has been beating the market while paying one of the biggest, most sustainable dividend yields out there.” PDI hasn’t cut distributions since:

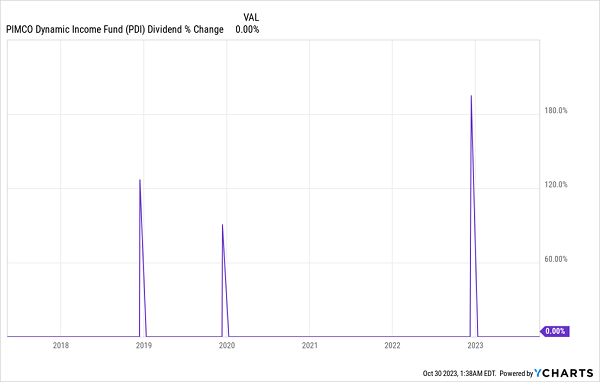

A Stable Dividend—With Big Special Payouts, Too

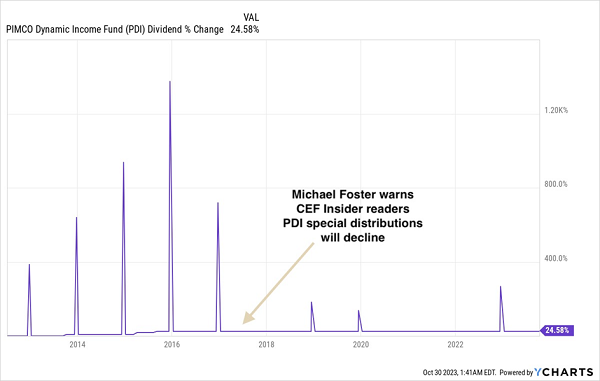

That, however, doesn’t mean PDI was an amazing fund to buy at the time. I also warned in the same article that PDI’s special distributions (shown in those three spikes in the chart below) would get smaller. And that is, indeed, what came to pass.

PDI’s Bonus Bonanza Quiets Down

The main culprit was low interest rates, of course.

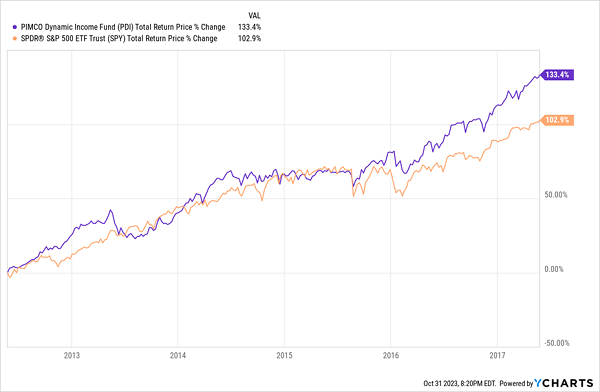

PDI had been collecting excess income through a strong portfolio that benefited from lower rates at a time when those same lower rates scared investors out of the bond market. This helped PDI provide an income stream 800% larger than the S&P 500 in its first years, while beating the S&P 500 on a total-return basis.

Smartly Run Bond Fund Beats Stocks

As the subprime-mortgage crisis became a more distant history, this bond trade got more crowded and PDI’s first sub-5% discount to NAV, in 2013, slowly turned into a 24.5% premium by late 2019.

I started to write about PDI less, aware the payouts were pricey. Now, fortunately, things are different.

PDI Is Cheap—and Its Payout Is Sustainable

Fast-forward to today and PDI’s income stream is still stable because it uses a variety of credit investments to buy undervalued bonds that yield more than average, while mitigating risk through credit instruments that change the fund’s exposure to various risks (duration, default, interest rates), according to the market.

This means PDI should be able to get a higher income stream than the bond market by a few hundred basis points, which compensates for the fund’s riskier portfolio relative to risk-free assets, such as Treasuries. So, for instance, when the federal funds rate is targeting 0.25%, and PIMCO’s strategy means PDI can earn the funds-rate target plus a spread (let’s say 800 basis points, although this number historically has been much higher), PDI has a sustainable 8.25% income stream right off the bat.

The Fed’s rate target is now 5.5%, meaning PDI’s income stream should now continue to be 13.5%. This is actually lower than PDI’s year-to-date net investment income, which is at 13.994%, but let’s stay conservative when analyzing how sustainable its dividend is.

This conservative scenario suggests that, even if its 16.2% yield doesn’t turn out to be sustainable in the long run, PDI is likely to give investors a minimum of $11,250 in monthly income per million invested, which is still a lot of cash.

And we know PIMCO is great at maintaining payouts in higher-rate environments; doing so is what made company founder Bill Gross a legend at the start of his career in the 1980s, when rates were far higher than they are today. PDI’s older sibling, the PIMCO High Income Fund (PHK), also beat the bond market and maintained payouts during the very aggressive rising rates of the early to mid-2000s.

This leads us to our biggest takeaway: this 16.2%-yielding fund, which would yield 13.5% in our conservative worst-case scenario, is not only perfectly set up to outperform like PIMCO has in similar environments in the past—it is also oversold.

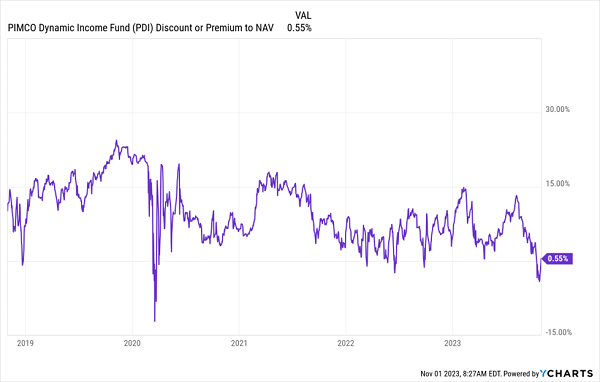

PDI’s Valuation Hits Historic Lows

As I write this, PDI’s market price roughly matches its net asset value (NAV), a level it’s only hit a few times in the last five years and well below its five-year average premium of 9.96%.

This means PDI is setting up for capital gains; it also means that the fund is set up to give us at least $11,250 in monthly income over the long run on a million-dollar investment in a worst-case scenario. Not a bad deal either way!

5 Ways to Build a Sturdy Monthly Payer Portfolio (With a Huge 9.2% Yield)

Another benefit of PDI is that its income stream rolls our way monthly—another bonus of investing through CEFs! Few people know it, but most CEFs kick out dividends every 30 (or 31) days, instead of every quarter, like pretty well all stocks.

That makes CEFs a terrific way to build a regular income stream. To help you do just that, I’ve assembled a 5-CEF portfolio yielding a sky-high 9.2%. It gives us everything we want in a collection of monthly payers: diversification, big discounts and, of course, a high yield!