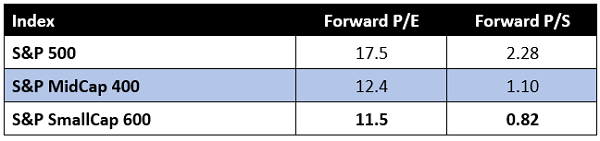

Small dividend stocks are dirt cheap right now. I’m talking about stocks trading for less than one year’s worth of sales. Yields up to 14.7%. And single-digit P/E ratios.

Why such deals? Well, because they’ve been pummeled into bargain territory of late. A number of high-yield bargains are staring us right in the face.

Small firms, straight up, are the cheapest stocks on the planet right now:

Value is great but show us the money! We’ll do so with five small-caps averaging a stellar 12% in yield among them. Are these deals or are these equities cheap for a reason? Let’s discuss.

Innovative Industrial Properties (IIPR)

Dividend Yield: 10.2%

When you think of industrial real estate investment trusts, you think of properties like warehouses and logistics centers.

But Innovative Industrial Properties (IIPR) isn’t your typical industrial REIT.

IIPR deals in weed.

Innovative Industrial Properties is a rare real estate play that provides capital for the regulated cannabis industry. With its sale-leaseback program, IIPR buys freestanding industrial and retail properties (primarily marijuana growth facilities) then leases them right back, providing cannabis operators with much-needed influxes of cash that they can use to expand their operations.

Marijuana might still be a relatively nascent industry, but IIPR looks like an old, established mainstay, building a portfolio of 108 properties (covering nearly 8.9 million rentable square feet!) across 19 states.

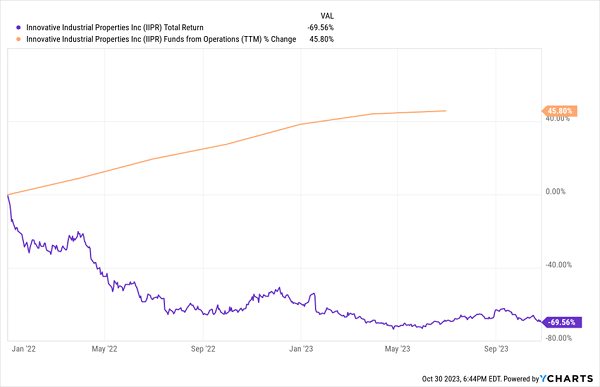

Of course, marijuana has also been a troubled industry, suffering a massive multiyear pullback from its 2019 highs. IIPR has hardly been immune, losing 70% (including its generous dividend!) since its own peak in late 2021—despite continued solid operational improvement.

Why Have Investors Ignored IIPR’s Strong Numbers?

I examined IIPR roughly a year ago, and my biggest hang-up at the time was valuation—shares at the time traded at a little more than 13 times adjusted funds from operations (AFFO) forecasts.

Shares have lost another quarter of their value since then.

But the bottom might finally be in for this small-cap REIT. While AFFO (and dividend) growth is slowing, shares trade at less than 9 times estimates, putting IIPR stock squarely into value territory. The payout, in the meantime, has ballooned into double digits.

Kimbell Royalty Partners (KRP)

Dividend Yield: 9.7%

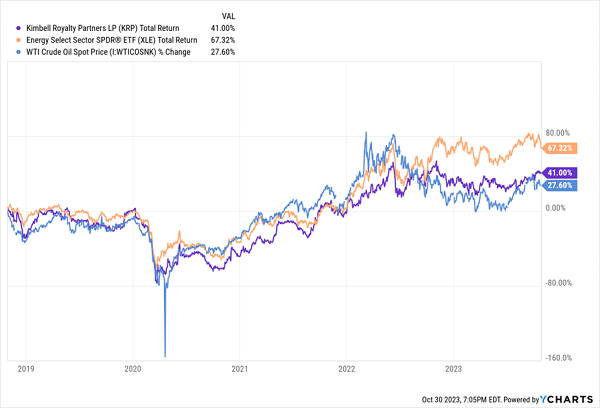

Kimbell Royalty Partners (KRP) is a name you almost certainly haven’t come across before. This roughly $1 billion energy name doesn’t pump oil, or send gas through pipelines, or sell you gasoline—it simply buys and owns royalty interests in oil and natural gas.

That’s it.

So, how does Kimbell make money? Well, it owns tracts of land that it then leases to energy producers, who in turn pay both an upfront “lease bonus” as well as a continuing royalty interest, typically 20% to 25% of revenue or production.

Currently, KRP owns more than 17 million gross acres in 28 states “and in every major onshore basin in the continental United States.” That includes formations like the Permian, Eagle Ford and Bakken.

The one thing Kimbell does share in common with traditional energy plays is that it’s strongly tethered to energy prices. Lower oil and gas prices are problematic—they decrease the royalties Kimbell collects, plus they can prompt producers to pare back operations, reducing output and further cutting into KRP’s profits. On the flip side, higher commodity prices tend to pad royalties sent to Kimbell.

So, despite its very different approach to making money, KRP very much trades like your average energy stock.

As Oil and Gas Go, So Goes Kimbell

Where Kimbell really differs, though, is its distribution.

For one, because varying energy prices can whip its earnings around, Kimbell has a variable dividend that keeps it from breaking the bank when oil and gas levels retreat. That’s not too uncommon—a growing number of energy firms have adopted this model.

But more importantly, much of Kimbell’s distribution is typically not cash, but instead non-taxable reductions to the tax basis of each unitholder’s ownership interest in Kimbell. Nearly 90% of the distribution it paid in August was structured this way.

(Also, a word to the wise: A lot of financial data providers list “LP” with Kimbell’s name, implying it is a master limited partnership. That information is outdated. Kimbell is neither an MLP or a royalty trust—it converted to a C-Corp back in 2018.)

It’s difficult to assess the value on such an oddball business, but at 9 times cash available for distribution (CAD), Kimbell at least appears cheaply priced.

Goldman Sachs BDC (GSBD)

Dividend Yield: 13.1%

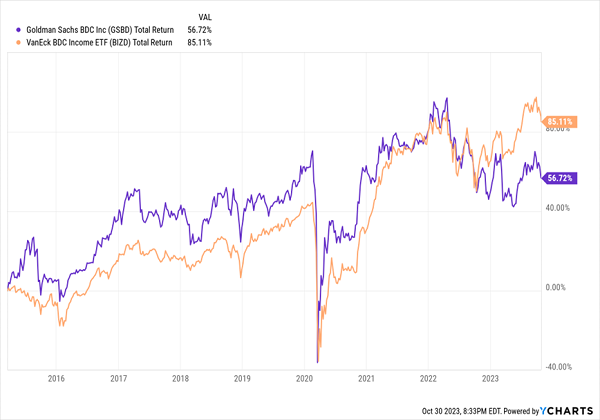

Analysts see the world through rose-colored glasses, which makes their drab opinion of Goldman Sachs BDC (GSBD) all the more noteworthy.

Goldman Sachs BDC is a business development company that can “draw upon the vast resources of Goldman Sachs to assist in the evaluation of potential investment opportunities.” It typically invests between $25 million and $75 million in companies with EBITDA of between $5 million and $75 million annually. At the moment, Goldman sees fit to hold 135 portfolio companies across 36 industries.

Also at the moment, GSBD trades at a decent 6% discount to its net asset value (NAV).

The problem is, right now, you’re pretty much just buying the Goldman name—but not its historical standard of quality. Yes, GSBD has provided periods of outperformance over time, but it has largely traded in line with the BDC industry, and it has turned into quite the laggard of late.

Goldman? More Like Pyrite Guy.

Among other issues, GSBD has had problems with its debt-to-equity ratio (currently 1.2), which has remained doggedly higher than company targets all year. And in Q2, it placed another two portfolio companies on non-accrual, raising non-accruals as a percentage of amortized cost to 1.8% from 1.6% in Q1.

For what it’s worth, it’s not all frowns for this BDC. Net investment income came in ahead of estimates, NAV ticked higher, and the net funded portfolio was ahead by $17 million.

Yes, GSBD offers a safe and sizable dividend. But without a growth catalyst, that fat payout will continue going toward offsetting the stock’s deep declines.

Chimera Investment Corp. (CIM)

Dividend Yield: 14.7%

Chimera Investment Corp. (CIM) is a member of one of the highest-yielding industries you can find: mortgage REITs (mREITs). Rather than owning physical properties like a traditional REIT, mREITs deal in paper—that is, mortgages, mortgage-backed securities (MBSs) and other instruments.

Chimera calls itself a “hybrid” mortgage REIT, as it owns residential mortgage loans, as well as agency and non-agency MBSs. But to be clear: Its business is heavily lopsided in mortgage loans (91%), with most of the rest in non-agency residential MBSs (8%).

mREITs are a tough business—especially whenever the Federal Reserve clamps down on easy-money policy. See, mREITs make money by borrowing “short” (assuming short-term rates are lower) and lending “long” (if long-term rates are higher, which they usually are). However, Treasury yields have been inverted (long-term rates are lower than short-term rates) for roughly a year now.

mREITs are best off when long-term rates are on the decline, because existing mortgages become more valuable. But when rates are rising—which they have been for a couple years now—mREITs feel the pain.

That’s very much the case for Chimera, which is difficult to consider a bargain despite shares trading for just 64% of book right now.

CIM has had to throttle back its dividend twice in the past two years, from 33 cents per share quarterly to 23 cents in 2022, then to 18 cents this year—a 45% haircut that has investors reeling.

Chimera: Part Lion, Part Goat, Part Snake? Wrong. It’s a Dog.

And Chimera’s struggles appear far from over. The mREIT recently reported a second-quarter earnings miss and acknowledged that it would either need interest rates to fall, or achieve greater scale, to get its return on equity up into double digits.

Buckle (BKE)

Dividend Yield: 12.2%

The retail industry isn’t the first or fifteenth place most people would go looking for high dividends, but it has its fair share of generous yields. Macy’s (M) yields 5.5%. Best Buy (BBY) yields 5.7%.

But no one holds a candle to the Buckle’s (BKE) 12%-plus payout.

Buckle is a fashion retailer offering mid- to higher-end clothes, accessories and footware. And unlike many retailers that have been battered by e-commerce, Buckle has come into its own, enjoying an explosion in profits over the past three years that has seen BKE shares zig and zag their way to several all-time highs in that time.

Buckle: A Rare Brick-and-Mortar Retail Renaissance

Buckle is a curious play. On the one hand, Buckle is indeed cheap for a reason—red-hot growth is cooling into an operational pullback. Revenues for the past six months were off 5.9% year-over-year, while profits were down 16%. That tracks with full-year estimates for a 4% pullback in sales and an 18% decline in earnings.

On the other, BKE’s top and bottom lines are expected to rebound mildly next year—and Buckle shares trade at less than 8 times profit estimates. Also, this is a fundamentally sound business with much higher margins (mid to high 40s) than many of its industry mates, not to mention a little more cash on hand than debt outstanding.

Where the rubber meets the road is the dividend—and that’s largely up to your income needs. See, Buckle is a habitual special dividend payer. Its regular payout only accounts for 4.2% of its yield—the remaining 8% is chalked up to a $2.65-per-share special distribution made in early 2023.

Earn 8% in Retirement + Get Paid EVERY MONTH

If you’re on the younger side and like the appeal of occasional bursts of cash, BKE is more capable of delivering that than most. However, given that these special dividends vary quite a bit, Buckle doesn’t quite cross the yield threshold I’d want for a regular retirement holding.

But if you’re a long-term investor looking for high yields you can count on year in, year out—and in fact, month in, month out—you can’t do better than the beautifully boring, high-yielding blue chips I hold in my “8% Monthly Payer Portfolio.”

Don’t let the name deceive you. The “8% Monthly Payer Portfolio” isn’t just about earning high levels of yield—it’s about earning high levels of yields by leveraging steady-Eddie holdings that won’t have you reaching for the Pepto every time the S&P gets the jitters.

You also won’t need to stress about the size of your nest egg. Unlike many retirement plans that require you to bleed out your savings as you age, the income this portfolio can generate is so rich, it can sustain a retirement on dividends alone.

Here’s the math: A mere $500,000 nest egg—less than half of what most financial gurus insist you need to retire—put to work in this powerful portfolio could generate a $40,000 annual income stream.

That’s more than $3,300 every month in regular income checks!

Even better? The current bear market has provided us with a rare gift, pulling many of these monthly dividend stocks back into our “buy zone,” where we can grab them at bargain prices. Click here to learn everything you need about these generous monthly dividend payers right now!