In most US industries, banks help businesses finance their buildings. The lenders also provide working lines of capital for the operations to grow.

Cannabis is different. It is tricky for operators to find money due to federal roadblocks.

At the national level, cannabis is still illegal. However, 40 states have legalized the drug in some fashion. Uncle Sam mostly looks the other way and lets states regulate their own markets—except when it comes to banking and taxes.

Banks cannot lend to cannabis operators. So, good luck financing that building.

Also, there is a tax code relic of the 1980s war on drugs (“Just Say No!”) called IRC Section 280E. It blocks cannabis operators from deducting ordinary business expenses. Which means their profits are artificially low and access to credit is denied due to poor-looking books and federal laws.

But if you live in a state where cannabis has been legalized, you know there is plenty of money flowing. Obviously, there is no shortage of demand to fund the countless dispensaries that have popped up in recent years. Where do these weed businesses find the money?

The answer is Innovative Industrial Properties (IIPR), which acts as the first landlord and primary lender of choice for cannabis operators. IIPR is the capital lifeline for the industry. And it’s a dividend cash cow that yields 13.7%!

IIPR buys dispensary facilities from the operators who are often short on cash and remember, could not finance their buildings. In the transaction, IIPR hands them a chunk of cash they badly need. Then it leases the facility back to the operator for 15 to 20 years.

The operators receive money upfront. IIPR collects long-term rent checks. And shareholders snag a fat dividend.

Because traditional banks won’t touch the space, IIPR negotiates incredibly favorable leases. They have long durations, built-in rent escalators and guarantees from the large corporate multi-state operator-lessees.

IIPR is essentially a “Godfather landlord” in a restricted industry. Cannabis peddlers need cash and have nobody else to turn to. So, they take the deal.

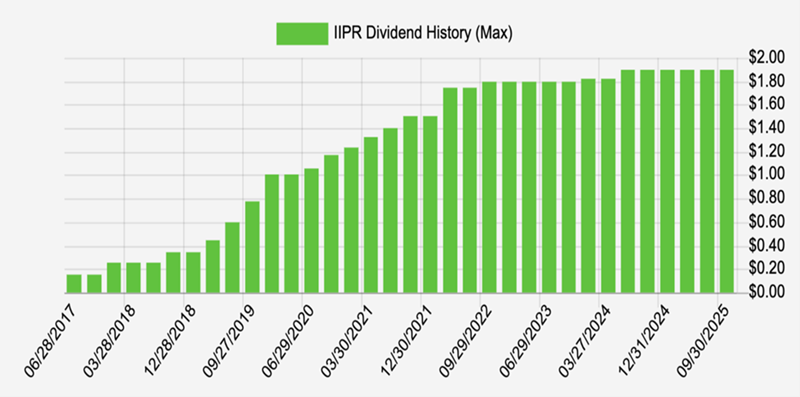

These rents fund a dividend that has grown steadily since the company’s IPO in 2016. The first quarterly payout was $0.15 per share. Cannabis stocks have been volatile but IIPR’s payout has been a steady staircase higher to $1.90 per share, a 12-fold increase:

IIPR’s Blazing Dividend History

IIPR’s balance sheet is clean and its leverage is low. It is a reputable publicly traded company with “mob-boss” economics. IIPR has “Prohibition pricing power!”

Why doesn’t this company command more per share (and pay less?). The stock is unloved today because it was too loved before. IIPR delivered dynamite 1,620% returns from 2016 to 2021, climaxing in a bubbly valuation. Investors paid sky-high multiples—30X to 40X funds from operations (FFO)—for a REIT yielding 2%.

Then the air came out. The stock deflated 75% from its peak. Analysts fled and downgraded. Today only one analyst rates IIPR a Buy. (By comparison, more than 400 of the S&P 500 have a Buy label. Those analysts are certainly a cheery lot!)

Which is perfect for us careful contrarians. We have a hated stock with plenty of cash flow.

Today, IIPR trades for just eight-times FFO. This is quite cheap for a solid REIT. Thanks to its 13.7% dividend, a $50,000 position in IIPR pays almost $7,000 per year in cash income.

Dividend coverage is fine. The $230 million FFO haul keeps the payout flowing. More importantly, the stock looks frisky again to the upside. IIPR carved a bottom in the spring and, two months ago, bulls rejected another selloff attempt. Momentum is shifting.

Plus, IRC Section 280E is likely to be softened or removed in the coming years. Cannabis legalization has momentum at the state level. The federal restriction is a relic that, when repealed, will unlock tax relief and improve operator coverage ratios right away.

IIPR longs may not have to wait that long. The stock may pop on the next upgrade, with seven analysts as current holdouts. The bar is low and the yield stays sky high while we wait.

Deals like IIPR exist because Wall Street suits and mainstream financial advisors are unimaginative. Their jobs depend on herdlike mediocrity. So, they will lazily tell you that IIPR is risky—without doing any research about its leases, tenants or current cash flows!

We contrarians don’t care what the vanilla beans say, except as a signal to fade their groupthink. And that’s how I uncover hated high-yield opportunities like IIPR—the kind that can fund your retirement while Wall Street holds its nose.